Harbin Bank Bundle

Can Harbin Bank Thrive in China's Dynamic Banking Sector?

From its humble beginnings in 1997 as a city commercial bank, Harbin Bank has charted a remarkable course. Today, it stands as a significant Harbin Bank SWOT Analysis player in China's competitive banking sector, but what does the future hold? This exploration delves into the Growth Strategy and Future Prospects of Harbin Bank, examining its path to success.

This analysis will dissect Harbin Bank's strategic initiatives, from its expansion plans across China to its embrace of digital transformation. We'll examine the financial outlook for Harbin Bank, considering both the opportunities and the challenges it faces in a rapidly evolving Financial Institution landscape. Understanding the China market and Banking Sector dynamics is key to unlocking Harbin Bank's long-term growth potential.

How Is Harbin Bank Expanding Its Reach?

Harbin Bank's expansion strategy focuses on accessing new customer segments and diversifying its revenue streams. Initially, the Marketing Strategy of Harbin Bank involved expanding beyond Harbin City to establish branches in other cities such as Dalian, Tianjin, Shuangyashan, and Jixi. A key element of this growth has been its focus on microcredit, serving small businesses, micro-enterprises, and rural farmers.

The bank's commitment to supporting the real economy, particularly small and micro enterprises, technological innovation, and green development, aligns with national strategies. This presents avenues for growth through targeted lending and financial services. Furthermore, Harbin Bank has been recognized for its efforts in rural revitalization, indicating a continued focus on expanding its presence and services in these areas.

While specific new market entries or large-scale mergers and acquisitions for 2024-2025 are not explicitly detailed, the bank's continued emphasis on serving the real economy and specialized businesses suggests ongoing organic expansion within existing and potentially new regions in China. This strategic approach aims to capitalize on emerging opportunities and strengthen its position within the banking sector.

Financial Backing and Strategic Focus

To support its expansion initiatives, Harbin Bank has secured significant financial backing. In August and October 2024, and March 2025, the bank issued three series of tier-2 capital bonds, totaling RMB 140 billion. These funds are intended to replenish its tier-2 capital, providing the financial resources needed to fuel its growth strategy.

- The first series of tier-2 capital bonds issued in August 2024 amounted to RMB 50 billion.

- The second series, issued in October 2024, totaled RMB 40 billion.

- The third series, issued in March 2025, also amounted to RMB 50 billion.

- The bank's focus remains on serving the real economy, supporting small and micro enterprises, and contributing to rural revitalization.

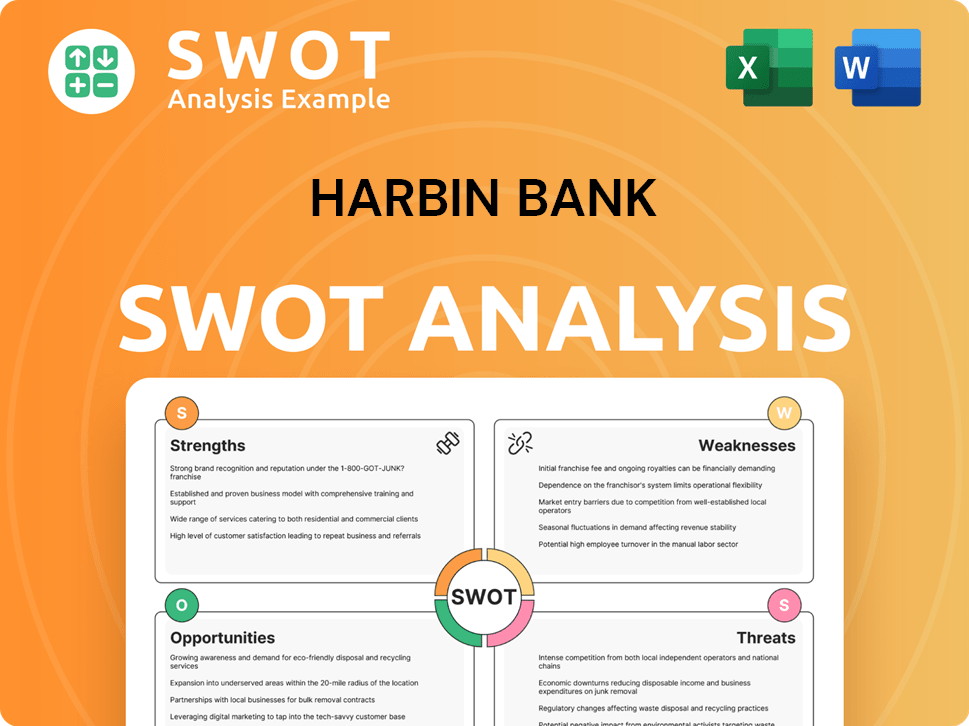

Harbin Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Harbin Bank Invest in Innovation?

In the dynamic landscape of the Banking Sector, Harbin Bank is actively embracing innovation and technology to fuel its Growth Strategy. This approach is crucial for enhancing operational efficiency, managing risks effectively, and providing sophisticated financial products and services. The bank's commitment to digital transformation positions it to meet evolving customer needs and maintain a competitive edge within the Financial Institution sector in China.

The bank's strategic focus on technological advancements is evident in its efforts to build an intelligent risk control platform. This platform is designed to proactively identify and address potential risks, thereby improving internal control mechanisms. By leveraging technology, Harbin Bank aims to streamline its operations and enhance its overall performance, contributing to its long-term Future Prospects.

Harbin Bank is also prioritizing data utilization to improve decision-making processes and customer service. The bank has strengthened the application of ICBC e Prevention and developed a zero-code data application platform and a digital operation view centered on customers. This initiative aims to realize a new paradigm of data analysis through natural language interaction, lowering the threshold of data application for users and improving user-friendliness.

Intelligent Risk Control Platform

The intelligent risk control platform is designed to dynamically reveal and prompt potential risks. It intelligently intercepts high-risk businesses, ensuring robust risk management. This platform is a key component of Harbin Bank's strategy to maintain financial stability and operational efficiency.

Data Application and Analysis

Harbin Bank has enhanced its data analysis capabilities through the application of ICBC e Prevention. It has also developed a zero-code data application platform and a digital operation view centered on customers. These tools enable the bank to gain deeper insights into customer behavior and market trends.

Customer-Centric Digital Operation

The digital operation view centered on customers aims to provide a more personalized and user-friendly experience. This approach involves leveraging natural language interaction to simplify data analysis. This initiative helps lower the threshold of data application for users, improving overall user-friendliness.

Awards and Recognition

In October 2024, Harbin Bank received the 'Outstanding Regional Private Banking Service Award' and 'Bank with Outstanding Wealth Management Service' by the Golden Reputation Award of Puyi Standards. The 'Cross-border Digital Finance Platform' also won the '15th Financial Product and Service Innovation Award'. These awards highlight the bank's commitment to innovation.

Impact on Growth

Technological advancements contribute to Growth Strategy by improving operational efficiency and enhancing risk management. They also enable the offering of more sophisticated financial products and services. These improvements are vital for achieving the bank's strategic goals.

Strategic Goals

Harbin Bank's strategic goals include improving operational efficiency, enhancing risk management, and offering more sophisticated financial products and services. These goals are supported by the bank's digital transformation strategy. The bank's focus on innovation is a key driver of its long-term Growth Strategy.

Strategic Initiatives and Future Outlook

Harbin Bank's focus on innovation and technology is central to its Growth Strategy, enhancing operational efficiency, risk management, and customer service. These initiatives are crucial for maintaining a competitive edge and achieving long-term success. Further insights into the bank's target market can be found in the Target Market of Harbin Bank article.

- Digital Transformation: Continuous investment in digital infrastructure and platforms to improve efficiency and customer experience.

- Risk Management: Implementation of advanced risk management tools and platforms to mitigate financial risks.

- Data Analytics: Leveraging data analytics to gain insights into customer behavior and market trends.

- Customer-Centric Approach: Focus on providing personalized financial products and services tailored to customer needs.

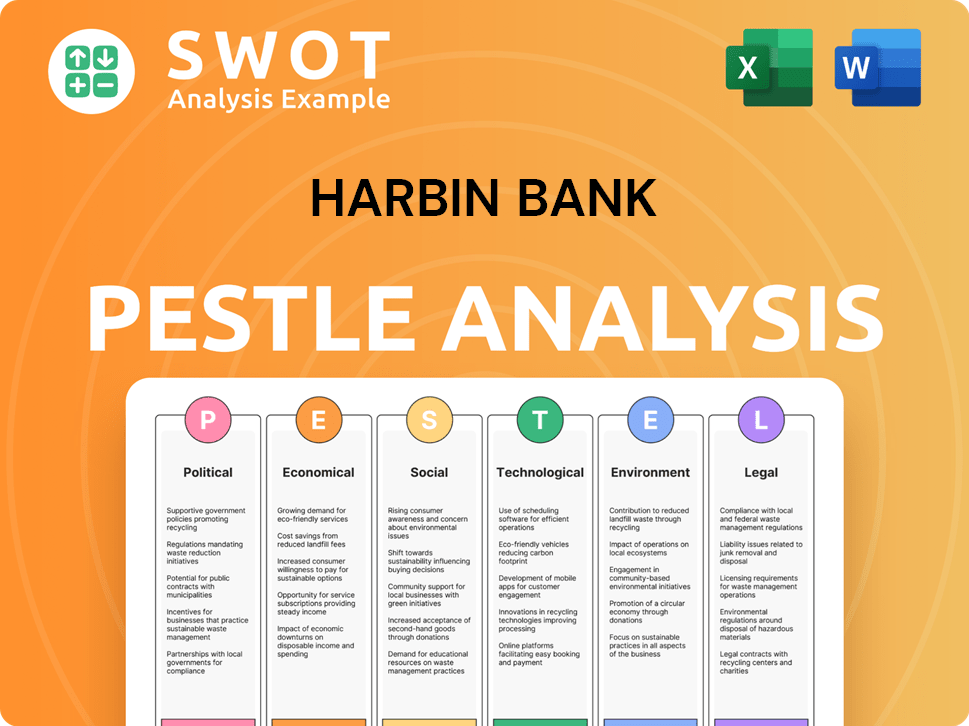

Harbin Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Harbin Bank’s Growth Forecast?

The financial outlook for Harbin Bank appears positive, reflecting improved performance in 2024 and a strong start to 2025. This positive trajectory is supported by increased net income and net interest income, indicating effective financial management and strategic growth initiatives. The bank's ability to increase revenue and net income, along with improvements in key financial metrics, underscores its potential for sustained growth within the Owners & Shareholders of Harbin Bank.

For the full year ended December 31, 2024, Harbin Bank reported a net income of CNY 919.67 million, a notable increase from CNY 739.99 million the previous year. The bank's revenue for 2024 was RMB 14.2432 billion, representing a year-on-year increase of 7.56%, and net income attributable to the parent company increased by 24.28% to RMB 0.9197 billion. These figures highlight the bank's robust financial health and its capacity to generate profits.

As of March 31, 2025, Harbin Bank's net income reached CNY 973.76 million, significantly up from CNY 343.11 million in the same period last year. This strong performance in the first quarter of 2025 suggests that the bank is on track to maintain its growth momentum. The increase in net interest income further supports this positive outlook, demonstrating the bank's ability to effectively manage its interest-earning assets and interest-bearing liabilities.

In 2024, Harbin Bank achieved a net income of CNY 919.67 million, a significant increase from the previous year. Net interest income also rose, reaching CNY 9,836.94 million. These figures indicate a strong financial performance.

The first quarter of 2025 saw a substantial increase in net income to CNY 973.76 million. Net interest income for Q1 2025 was CNY 2,023.46 million, exceeding the previous year's figures. This demonstrates continued financial growth.

Total assets as of December 31, 2024, were CN¥916.2 billion, with total equity at CN¥65.6 billion. Total deposits stood at CN¥716.8 billion, and total loans at CN¥379.9 billion, with a Net Interest Margin of 1.3%. These figures highlight the bank's financial stability.

The positive financial trajectory underpins the bank's strategic growth plans. The bank's ability to increase revenue and net income, along with improvements in key financial metrics, underscores its potential for sustained growth within the banking sector in China.

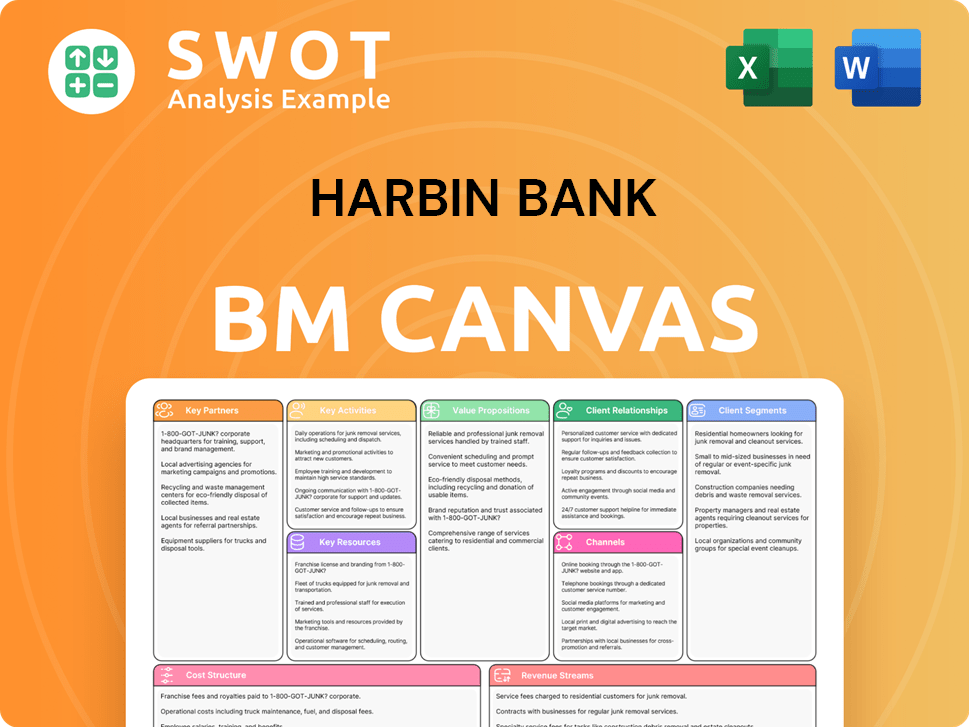

Harbin Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Harbin Bank’s Growth?

Several risks and obstacles could affect the future growth of Harbin Bank, as it navigates the competitive banking sector in China. The financial institution faces challenges from market competition and regulatory changes, which require strategic adaptation to maintain a competitive edge. Also, asset quality risks and economic conditions present additional hurdles that the bank must manage to ensure its long-term success.

Market competition is a significant ongoing challenge. The Chinese banking industry, as a whole, is experiencing a squeeze on profitability in traditional areas such as deposits and loans. This, along with narrowing net interest margins, necessitates that Harbin Bank and its peers adapt their business strategies and accelerate transformation to remain competitive.

Regulatory changes also pose a risk. The introduction of the National Financial Regulatory Administration (NFRA) 'Five Priorities' guidance in May 2024, which focuses on technology finance, green finance, inclusive finance, pension finance, and digital finance, requires banks to adapt their operations. Furthermore, the implementation of Total Loss-Absorbing Capacity (TLAC) in 2025 could introduce pressure on capital adequacy, particularly for smaller lenders like Harbin Bank.

Market Competition

The Chinese banking sector faces contracting profitability in traditional deposit and loan businesses. The industry is urged to adapt business strategies and accelerate transformation to maintain a competitive edge. This requires continuous innovation and strategic adjustments to stay ahead in the market.

Regulatory Changes

The NFRA's 'Five Priorities' guidance, introduced in May 2024, mandates banks to focus on technology, green, inclusive, pension, and digital finance. The rollout of TLAC in 2025 could introduce pressure on capital adequacy, especially for smaller lenders. These regulations require strategic adaptation and investment.

Asset Quality Risks

At-risk loans at major Chinese banks reached a four-year peak in the second half of 2024. Deteriorating retail credit quality and trade tensions are likely to increase these loans in 2025. Harbin Bank actively strengthens risk control and compliance management to mitigate these risks.

Capital Adequacy

The implementation of TLAC in 2025 could introduce pressure on capital adequacy. Smaller lenders like Harbin Bank need to ensure they have sufficient capital to meet regulatory requirements. This requires careful financial planning and management.

Bad Loan Levels

The level of bad loans at Harbin Bank is high, at 2.8% of total loans. The bank is actively strengthening risk control and compliance management to reduce this percentage. This involves intensifying oversight of high-risk customers and narrowing exposure in key areas.

Risk Management

Harbin Bank is strengthening risk control and compliance management, including intensifying oversight on customers with large risk exposures. The bank is also narrowing risk exposures in key areas such as real estate and local government debt. Effective risk management is crucial for sustainable growth.

Asset quality risks are a significant concern, with at-risk loans at major Chinese banks reaching a four-year peak in the second half of 2024. These are expected to grow further in 2025 due to issues in retail credit and trade. Harbin Bank is actively working to strengthen risk control and compliance, including more oversight of high-risk clients and reducing exposure in sensitive areas like real estate and local government debt. The bank's bad loan level is at 2.8% of total loans.

To address these challenges, Harbin Bank is implementing several strategies. The bank is actively strengthening risk control and compliance management, including intensifying oversight on customers with large risk exposures. Management continuously assesses and prepares for these risks through ongoing reform and transformation, enhancing fund utilization, and implementing multiple strategies to improve profitability. For more context, you can read about the Brief History of Harbin Bank.

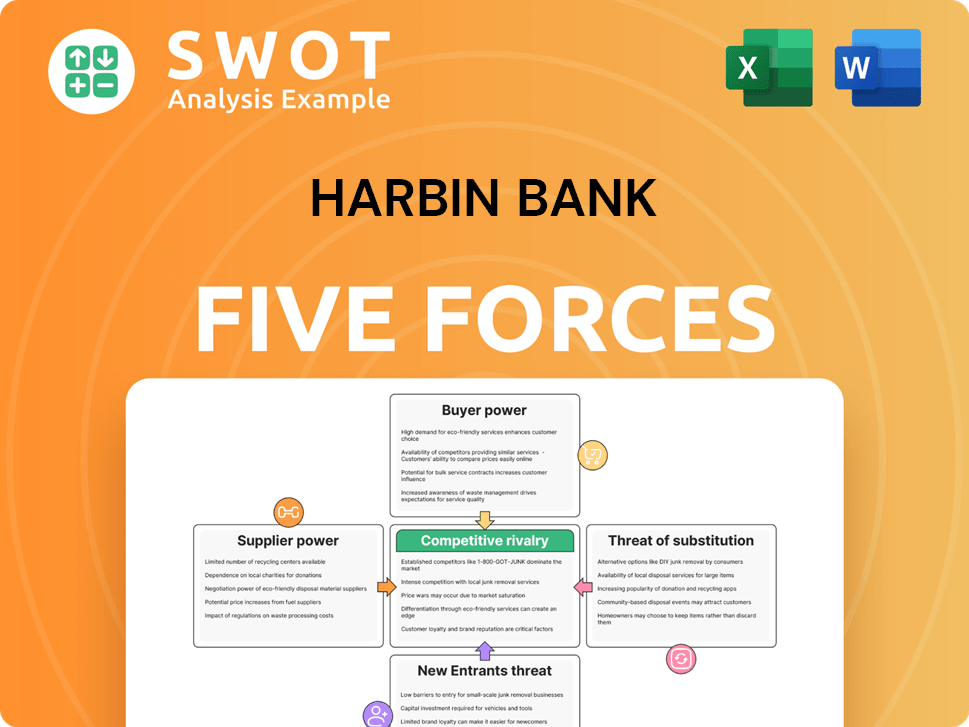

Harbin Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Harbin Bank Company?

- What is Competitive Landscape of Harbin Bank Company?

- How Does Harbin Bank Company Work?

- What is Sales and Marketing Strategy of Harbin Bank Company?

- What is Brief History of Harbin Bank Company?

- Who Owns Harbin Bank Company?

- What is Customer Demographics and Target Market of Harbin Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.