Dollarama Bundle

Can Dollarama Continue Its Dominance?

Dollarama, the Canadian dollar store giant, has captivated consumers with its value-driven approach since 1992. From its humble beginnings as a single store, the company has transformed the retail landscape, offering an array of products at irresistible prices. This Dollarama SWOT Analysis will explore the company's journey and future potential.

This in-depth Dollarama company analysis delves into its proven Dollarama growth strategy, examining its impressive financial performance and ambitious expansion plans. We'll explore Dollarama's business model and its ability to thrive even during economic downturns, alongside a look at its future revenue projections and competitive advantages. Understanding Dollarama's market share analysis and long-term financial goals is key to grasping its impact on the retail industry.

How Is Dollarama Expanding Its Reach?

The company is actively pursuing several expansion initiatives to drive future growth, both domestically and internationally. This strategy is a key component of its overall Dollarama growth strategy, aiming to increase its market share and revenue streams. These initiatives are designed to capitalize on the growing demand for value-focused retail, both in Canada and in international markets.

In Canada, the company is focused on expanding its store network and optimizing its logistics infrastructure. The company's growth strategy also includes strategic investments in its supply chain to support its expanding store network. These investments are essential for maintaining its competitive edge and meeting the increasing demand for its products.

Internationally, the company is expanding its footprint through its majority-owned Latin American subsidiary, Dollarcity, and through strategic acquisitions. These expansion efforts are a crucial part of the company's Dollarama future prospects, as it seeks to establish a strong presence in new and emerging markets.

The company has revised its long-term store target, aiming to operate approximately 2,200 stores by 2034. For fiscal 2026, the company expects to open 70-80 net new stores in Canada. The company had a total of 1,616 stores as of February 2, 2025.

In December 2024, the company acquired land in the Calgary, Alberta region for $46.7 million. It plans to build a 1.6 million square-foot logistics hub to service stores in Western Canada. This facility is expected to be operational by the end of 2027.

Dollarcity opened 100 net new stores in calendar 2024, bringing its total to 632 locations. The long-term target has been revised to 1,050 stores by 2031. The first stores in Mexico are expected to open in the summer of 2025.

The proposed acquisition of TRS, Australia's largest discount retailer, for approximately C$379 million (C$233 million equity value and C$146 million net debt). The acquisition is expected to close in the second half of 2025. The plan is to expand TRS's network from over 390 stores to approximately 700 locations by 2034.

Strategic Growth Initiatives

These expansion plans demonstrate the company's commitment to long-term growth and its confidence in its Dollarama business model. The company's strategic approach to expansion includes both organic growth through new store openings and inorganic growth through acquisitions.

- Aggressive store expansion in Canada.

- Strategic investments in logistics to support growth.

- International expansion through Dollarcity and acquisitions.

- Focus on value-focused retail to attract customers.

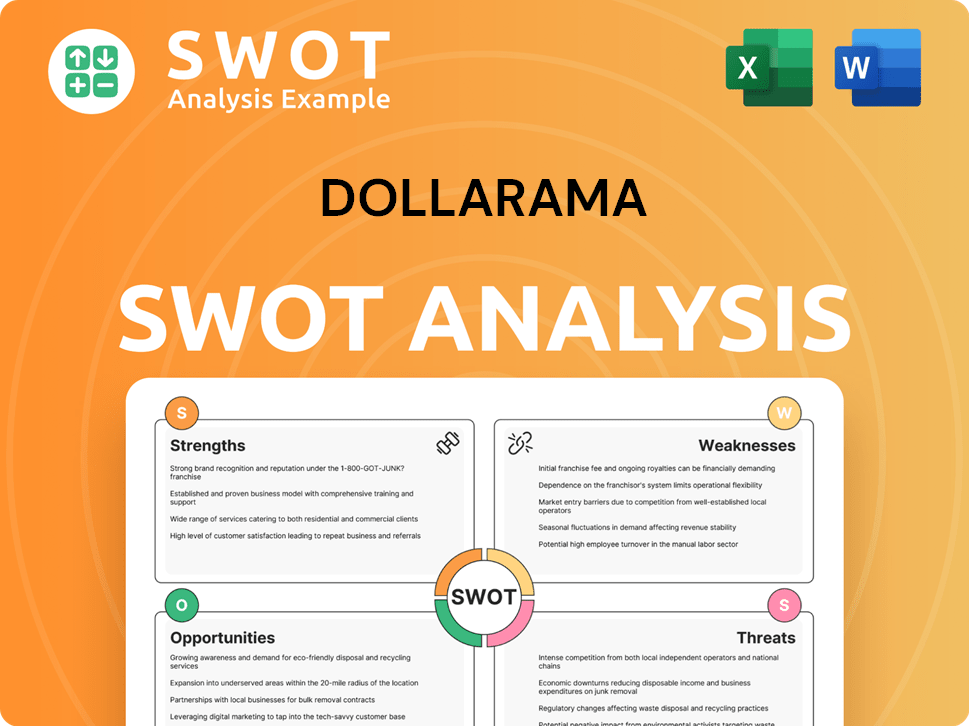

Dollarama SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Dollarama Invest in Innovation?

The Dollarama company analysis reveals a strategic focus on leveraging innovation and technology to enhance both its operational efficiency and the overall customer experience. While specific details regarding research and development (R&D) investments or patent filings are not extensively publicized, the company's commitment to adapting to evolving retail trends is evident through its digital transformation initiatives.

A key element of Dollarama's approach is its investment in optimizing its logistics and supply chain. This includes the development of a new distribution center, which is a significant step in supporting its ambitious expansion plans. This strategic focus on operational technology is crucial for maintaining its competitive edge.

The company's digital footprint, including its e-commerce site launched in 2019, is designed to constantly evolve the service and customer interaction model. This helps stimulate sales and keeps the company abreast of consumer and industry trends, contributing to its overall Dollarama growth strategy.

E-commerce Platform

Dollarama launched its e-commerce site in 2019, marking a significant step in its digital transformation. This platform serves as a key component in the company's strategy to adapt to changing retail trends and enhance customer engagement. The online platform is designed to evolve constantly to stimulate sales.

Logistics Hub in Calgary

Dollarama is developing a new logistics hub in Calgary, Alberta, spanning 1.6 million square feet, expected to be operational by the end of 2027. This facility is designed to enhance efficiency, reduce costs, and ensure a smooth flow of goods across Canada, especially in Western Canada. The new hub is part of a two-node logistics system.

Supply Chain Optimization

The company focuses on efficient sourcing and distribution to maintain cost advantages. This includes ongoing optimization efforts within its supply chain, potentially involving technological improvements. These efforts contribute to maintaining a strong gross margin.

Operational Technology

Dollarama's investment in infrastructure, such as the new logistics hub, demonstrates a commitment to leveraging operational technology. This supports the company's ambitious expansion plans. This strategic focus is crucial for maintaining its competitive edge.

Capital Allocation

A disciplined capital allocation strategy indirectly supports technological advancements. This contributes to cost advantages. This strategic focus is crucial for maintaining its competitive edge.

Customer Experience

Dollarama's approach to digital transformation is evident in its launch of an e-commerce site in 2019, serving as an additional growth platform to adapt to evolving retail trends. The digital footprint aims to constantly evolve the service and customer interaction model to stimulate sales and stay abreast of consumer and industry trends.

Key Technological and Innovation Strategies

Dollarama's Dollarama future prospects are closely tied to its ability to integrate technology and innovation effectively. While specific details on cutting-edge technologies are limited, the company's strategic investments in logistics and supply chain optimization are crucial. These initiatives support its expansion plans and contribute to its financial performance.

- E-commerce Platform: Launched in 2019, the platform is key to adapting to evolving retail trends.

- Logistics Hub: The new hub in Calgary, operational by the end of 2027, will improve efficiency and reduce costs.

- Supply Chain Optimization: Efficient sourcing and distribution contribute to maintaining a strong gross margin.

- Operational Technology: Investments in infrastructure support expansion plans.

- Capital Allocation: A disciplined strategy indirectly supports technological advancements.

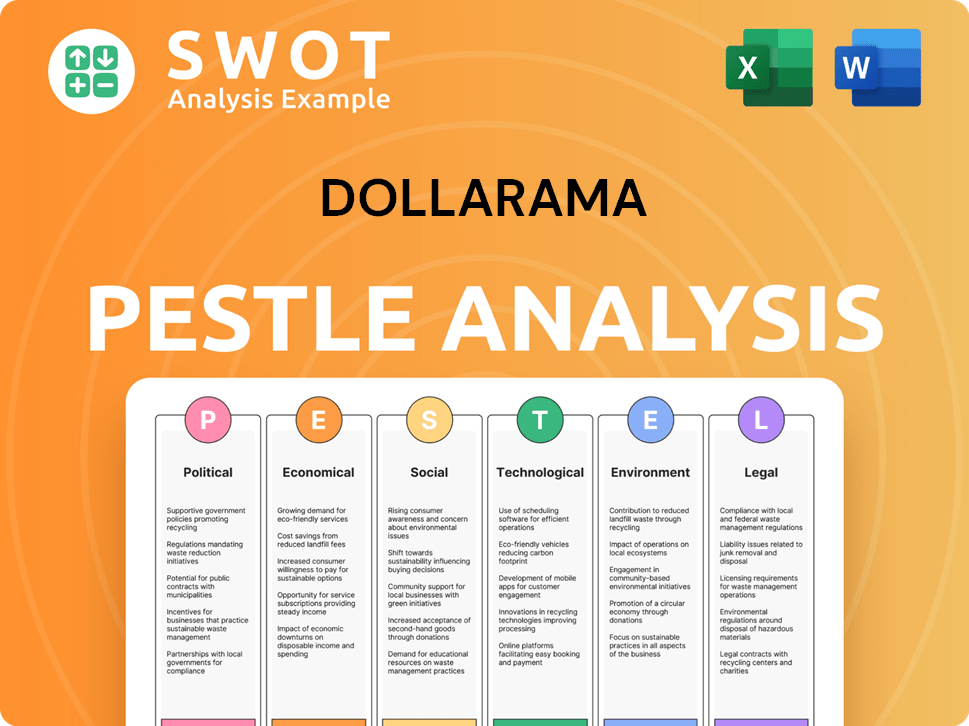

Dollarama PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Dollarama’s Growth Forecast?

The financial outlook for Dollarama is positive, with the company demonstrating strong performance and projecting continued growth. This positive trajectory is supported by solid revenue growth, increased earnings, and strategic financial management. An in-depth Revenue Streams & Business Model of Dollarama analysis provides further insights into the company's operations.

For fiscal year 2025, Dollarama reported a 9.3% increase in annual sales, reaching $6,413.1 million. This growth reflects the success of its business model and expansion strategies. The company's ability to maintain and increase its sales figures highlights its resilience and adaptability in the retail market.

Diluted net earnings per common share for fiscal 2025 increased by 16.9% to $4.16, up from $3.56 in fiscal 2024. This significant increase in earnings per share demonstrates the company's profitability and its ability to generate value for its shareholders. The company's comparable store sales grew by 4.6% in fiscal 2025, following a 12.8% growth in the previous year. For the fourth quarter of fiscal 2025, sales increased by 14.8% to $1,881.3 million, with comparable store sales increasing by 4.9%.

Dollarama's financial performance has been robust, with consistent growth in sales and earnings. This performance is a key indicator of the company's success in the retail sector. The company's ability to maintain and increase its sales figures highlights its resilience and adaptability in the retail market.

In fiscal 2025, Dollarama achieved a 9.3% increase in annual sales, reaching $6,413.1 million. Diluted net earnings per common share increased by 16.9% to $4.16. These results reflect the company's strong operational performance and strategic initiatives.

Comparable store sales grew by 4.6% in fiscal 2025, following a 12.8% growth in the previous year. This indicates continued strong performance in existing stores. For the fourth quarter of fiscal 2025, sales increased by 14.8% to $1,881.3 million, with comparable store sales increasing by 4.9%.

Looking ahead to fiscal 2026, Dollarama projects comparable store sales growth of 3.0% to 4.0%. Analysts anticipate revenue to rise from $6.4 billion in fiscal 2025 to $9.77 billion in fiscal 2030. Adjusted earnings per share are expected to expand from $4.16 to $7.4 over the same period.

Key Financial Strategies

Dollarama focuses on maintaining a strong gross margin and managing operating costs effectively. The company's capital allocation strategy includes organic growth investments and returning capital to shareholders.

- Gross Margin: Targeting 44%-45% of sales for fiscal 2025.

- SG&A: Projected at 14.5% to 15% of sales for fiscal 2025.

- Dividends: Increased quarterly cash dividend by 15.0% to $0.1058 per common share for fiscal 2025.

- Share Repurchases: Repurchased 8,119,971 common shares for $1,068.2 million during fiscal 2025.

- Capital Expenditures: Expected to rise to $185–210 million in fiscal 2026, excluding land acquisition.

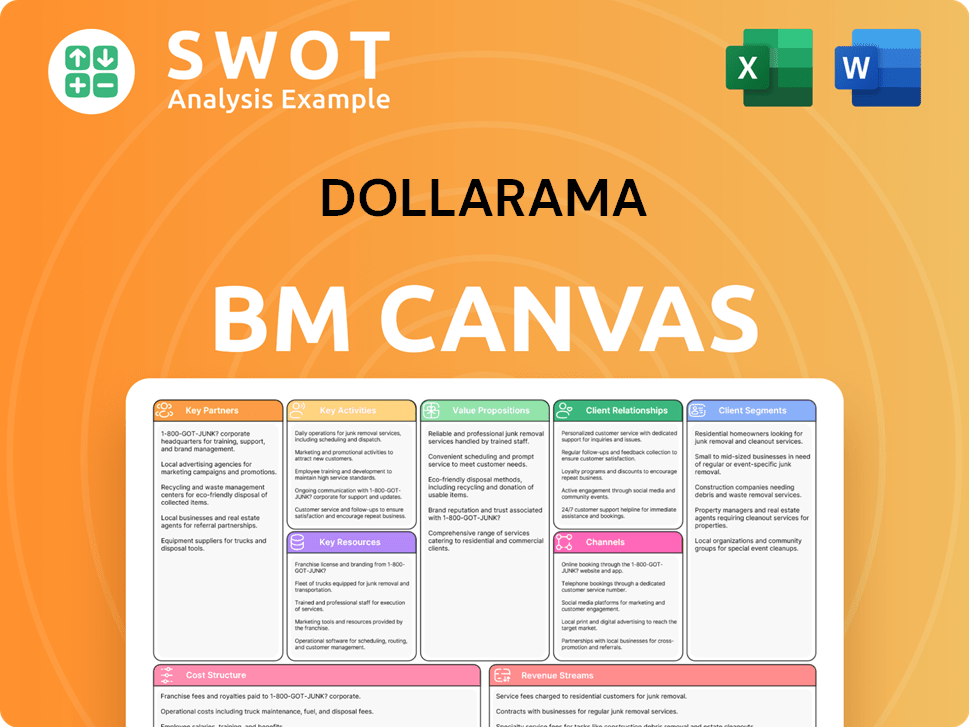

Dollarama Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Dollarama’s Growth?

The Dollarama growth strategy is not without its challenges. Several risks and obstacles could potentially impede the company's continued success. Understanding these potential pitfalls is essential for a comprehensive Dollarama company analysis and for assessing its future prospects.

One significant concern is the intense competition within the retail sector. Maintaining a compelling value proposition in the face of rivals like Walmart and Target is crucial. Furthermore, regulatory changes, particularly those impacting labor costs, pose a considerable risk to Dollarama's financial performance.

Supply chain vulnerabilities and geopolitical risks also present challenges. The company must navigate potential disruptions and manage the effects of currency fluctuations. Internal resource constraints, especially in logistics, add another layer of complexity to its expansion plans.

Competitive Pressures

The retail sector is highly competitive, with established players like Walmart and Target. These competitors also focus on value-driven pricing, which directly challenges Dollarama's market position. Maintaining a unique value proposition is critical for Dollarama's future revenue projections.

Regulatory and Labor Cost Risks

Regulatory changes, particularly those affecting labor costs, pose a risk. The company anticipates continued pressure on SG&A as a percentage of sales due to higher store labor and operating costs. Rising labor costs could impact profit margins, a crucial aspect of Dollarama's financial performance.

Supply Chain and Geopolitical Issues

Supply chain vulnerabilities and geopolitical risks are significant concerns. Increased shipping and transportation costs, along with a weaker Canadian dollar, can pressure gross margins. For instance, higher inventory shrinkage partially offset the benefits of lower inbound shipping costs in fiscal 2025.

Logistics and Infrastructure Challenges

Internal resource constraints, particularly in logistics infrastructure, have historically been managed through a centralized approach. Ambitious expansion plans require proactive measures, such as developing a new logistics hub in Western Canada. This is crucial for Dollarama's store expansion plans.

Stock Valuation and Growth Deceleration

The company's stock's high valuation and decelerating growth rates could be a risk for investors. Management assesses and prepares for these risks through strategic diversification, such as international expansion into Latin America with Dollarcity. This affects the Dollarama stock forecast.

Integration Challenges

The acquisition of The Reject Shop in Australia introduces potential risks related to foreign exchange currency fluctuations and integration challenges. This impacts the company's overall Dollarama business model and expansion plans.

In recent financial reports, Dollarama has noted that they anticipate continued pressure on SG&A as a percentage of sales due to higher store labor and operating costs. For instance, wage inflation has been higher than historical averages, impacting the cost structure. This is a key factor in Dollarama's long-term financial goals.

Supply chain disruptions and increased shipping costs can pressure gross margins. While lower inbound shipping costs positively impacted gross margin in fiscal 2025, higher inventory shrinkage partially offset this. This highlights the importance of effective supply chain management for Dollarama's market share analysis.

Geopolitical factors, such as counter-tariffs, can affect operations. While the impact of counter-tariffs imposed by Canada in response to U.S. tariffs was manageable, such events can introduce uncertainty. The company's response to these risks is a part of its sustainability initiatives.

The acquisition of The Reject Shop in Australia introduces potential risks related to foreign exchange currency fluctuations and integration challenges. This expansion strategy is a part of its overall growth opportunities in specific markets. The company's customer loyalty programs are also important.

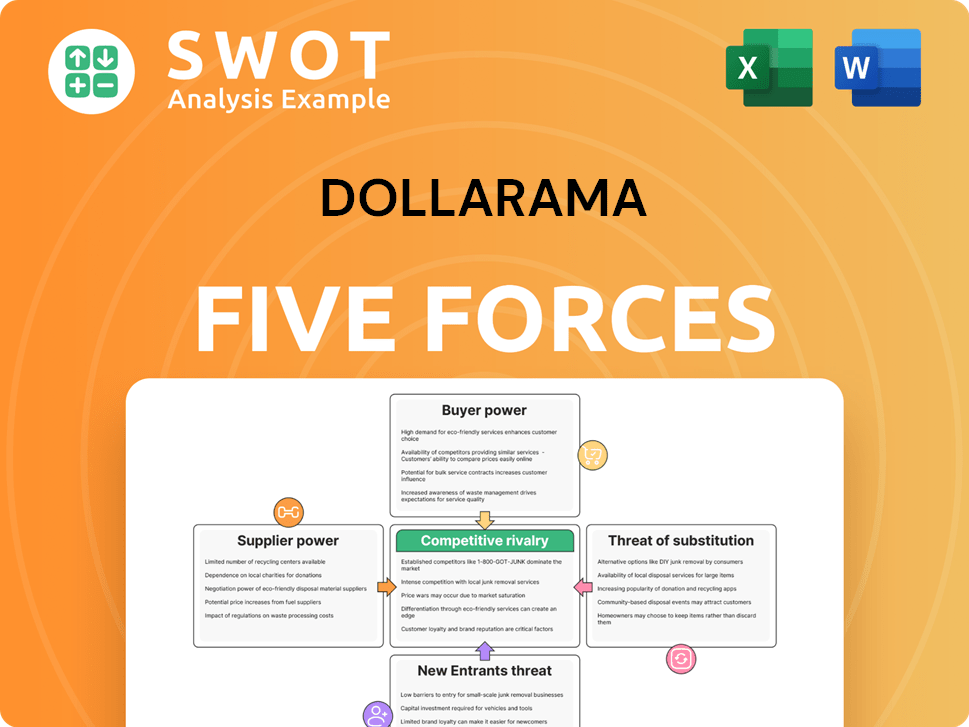

Dollarama Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Dollarama Company?

- What is Competitive Landscape of Dollarama Company?

- How Does Dollarama Company Work?

- What is Sales and Marketing Strategy of Dollarama Company?

- What is Brief History of Dollarama Company?

- Who Owns Dollarama Company?

- What is Customer Demographics and Target Market of Dollarama Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.