Columbia Bank Bundle

Can Columbia Bank Sustain Its Growth Trajectory?

Columbia Banking System Inc., through its subsidiary Columbia Bank, has emerged as a significant player in the financial sector, particularly after its merger with Umpqua Holdings Corporation. This strategic move created a formidable West Coast bank, reshaping its market position and expanding its reach. Founded in 1993, Columbia Bank initially focused on community-centered banking, evolving into a prominent financial institution with a broad presence across the Western United States.

Understanding the Columbia Bank SWOT Analysis is crucial to grasping its future prospects. This analysis will delve into Columbia Bank's expansion plans for 2024, assessing its competitive landscape and the impact of banking industry trends. We'll explore its financial performance, including profitability drivers and risk management strategies, to provide a comprehensive view of its long-term growth potential within the financial institution outlook.

How Is Columbia Bank Expanding Its Reach?

The primary driver of Columbia Bank's Columbia Bank growth strategy is its strategic merger with Umpqua Holdings Corporation. This merger, finalized in March 2023, significantly broadened its geographic reach and customer base, particularly across the West Coast. The integration process, ongoing through 2024, is designed to optimize branch networks and consolidate operations.

The merger created the largest bank headquartered in the Pacific Northwest. The combined entity now boasts combined assets exceeding $50 billion and a network of over 400 branches. This extensive network spans Washington, Oregon, Idaho, California, Nevada, Utah, and Arizona, positioning the bank for enhanced market penetration.

Beyond geographical expansion, Columbia Bank is diversifying its product and service offerings. This includes enhanced commercial lending capabilities, wealth management services, and specialized banking solutions. The focus is on providing a seamless customer experience across all touchpoints, including its traditional branch network and its growing digital presence. For more information on the bank's target audience, see Target Market of Columbia Bank.

The merger with Umpqua Holdings Corporation has been pivotal in expanding Columbia Bank's footprint. This expansion provides access to new customer segments and increases market share in key growth regions. The bank now operates across seven states, including California, which offers significant market opportunities.

Columbia Bank is broadening its financial solutions to include enhanced commercial lending, wealth management, and specialized banking services. This diversification strategy aims to meet the evolving needs of its customers. The integration of digital platforms is a key focus to improve customer experience and support both branch and digital banking channels.

The bank is actively working on integrating its digital platforms to provide a seamless customer experience. This includes enhancements to mobile banking, online banking, and other digital channels. The goal is to support both its traditional branch network and its growing digital presence, enhancing customer convenience and accessibility.

The integration process, which is ongoing through 2024, focuses on optimizing branch networks, consolidating operations, and harmonizing product offerings. This includes streamlining back-office functions and aligning customer service standards. The successful integration is crucial for realizing the full potential of the merger and achieving operational efficiencies.

Key Expansion Strategies

Columbia Bank's expansion strategy is multifaceted, focusing on geographic growth, product diversification, and digital enhancements. These initiatives are designed to strengthen the bank's market position and enhance its Columbia Bank financial performance.

- Geographic Expansion: Leveraging the expanded branch network across the West Coast to increase market share.

- Product Diversification: Offering a wider range of financial products and services to meet diverse customer needs.

- Digital Transformation: Investing in digital platforms to improve customer experience and operational efficiency.

- Merger Synergies: Integrating operations to realize cost savings and improve overall profitability.

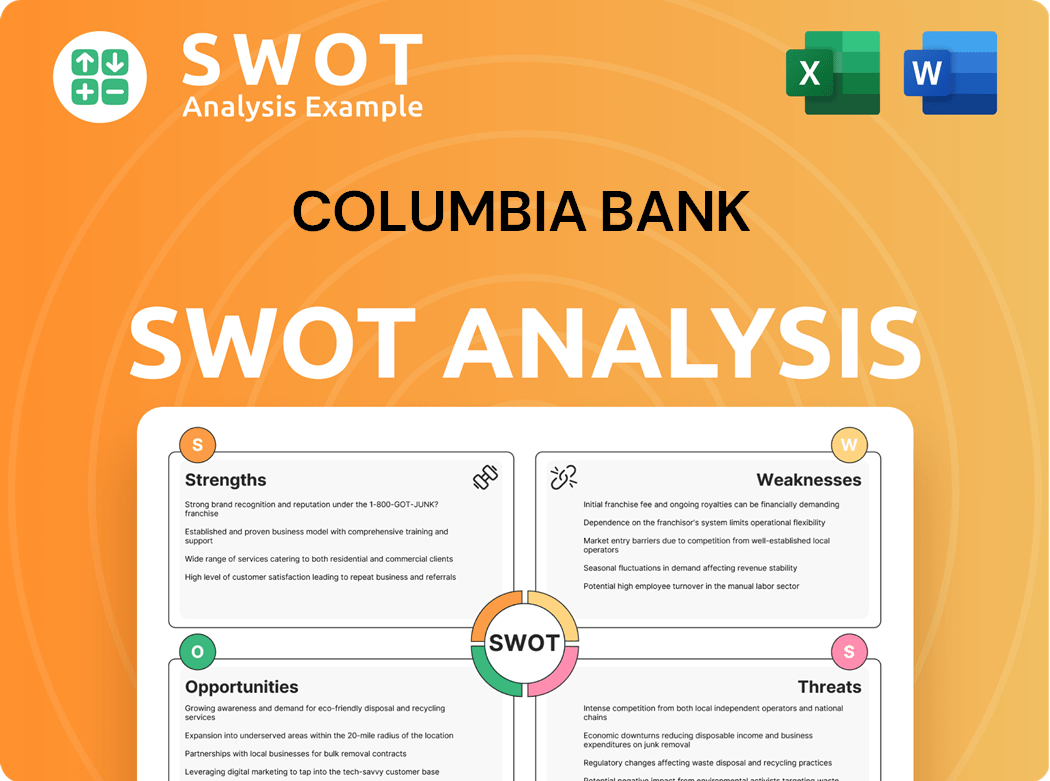

Columbia Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Columbia Bank Invest in Innovation?

The innovation and technology strategy of the bank is crucial for its ongoing expansion, especially after its merger with Umpqua. This combined entity focuses on using technology to improve operational efficiency, enhance customer experience, and introduce new digital offerings. A key part of this strategy involves integrating the technology infrastructures of both banks to create a unified and strong digital platform.

This integration includes investments in digital banking tools, mobile applications, and online account management systems to meet the needs of today's tech-savvy customers. The bank is committed to digital transformation, aiming to provide smooth and intuitive banking solutions across all channels, supporting its goals for growth by creating a more agile, efficient, and customer-focused banking experience.

The bank is also exploring the use of advanced technologies to drive innovation. While specific details on research and development investments or patents are not publicly detailed for 2024-2025, the industry trend suggests a focus on automation to streamline back-office operations and enhance efficiency. This approach is designed to support its growth objectives by creating a more agile, efficient, and customer-centric banking experience, positioning itself to compete effectively in a rapidly evolving financial landscape.

Digital Banking Focus

The bank is heavily investing in digital banking tools. This includes mobile applications and online account management systems. These investments are aimed at meeting the evolving demands of tech-savvy customers and improving overall customer experience.

Technology Integration

A key aspect of the bank's strategy is the integration of its technological infrastructures. This involves merging the systems of both banks to create a unified digital platform. This unified platform aims to streamline operations and improve efficiency.

Automation and Efficiency

The bank is likely focusing on automation to streamline back-office operations. This is a common trend in the banking industry. Automation helps in improving efficiency and reducing operational costs.

Data Analytics

The bank is likely utilizing technology to improve data analytics. Better data analytics leads to better decision-making. It also helps in personalizing customer interactions and enhancing risk management.

Customer-Centric Approach

The overall technology strategy is geared towards creating a customer-centric banking experience. This involves providing seamless and intuitive banking solutions across all channels. This approach helps in retaining and attracting customers.

Competitive Advantage

By focusing on technology, the bank aims to gain a competitive advantage. This includes improving efficiency, enhancing customer experience, and offering innovative digital products. This helps the bank compete effectively in a rapidly changing financial landscape.

Key Technology Initiatives

The bank's technology strategy is multifaceted, focusing on several key areas to drive growth and improve operational efficiency. These initiatives are designed to enhance customer experience, streamline internal processes, and ensure the bank remains competitive in the financial industry. The bank's focus on digital transformation is a key element of its competitive landscape.

- Digital Banking Platforms: Investments in mobile and online banking platforms are ongoing. These platforms are enhanced to provide customers with seamless and intuitive banking experiences.

- Data Analytics: The bank is likely using data analytics to improve decision-making. This includes better understanding customer behavior, personalizing services, and managing risks more effectively.

- Automation: Automation of back-office operations is a key focus. This helps in reducing costs and improving efficiency.

- Integration: The integration of technology systems from merged entities is a priority. This creates a unified platform for better management and customer service.

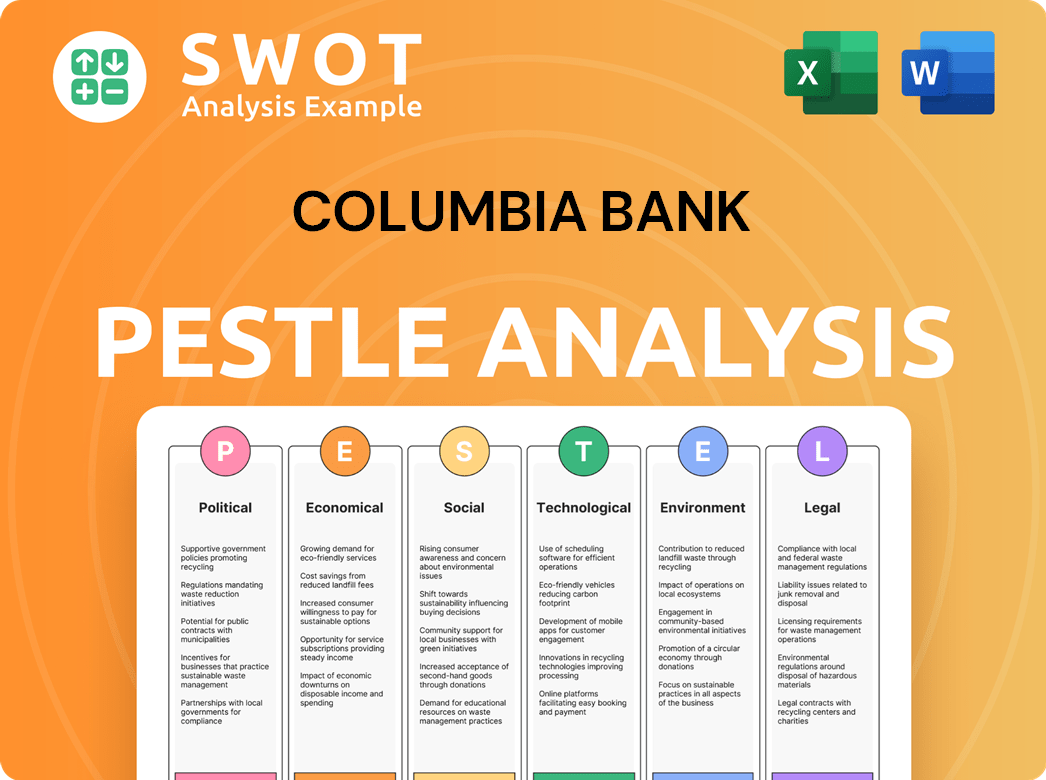

Columbia Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Columbia Bank’s Growth Forecast?

The financial outlook for Columbia Banking System is significantly influenced by the successful integration of Umpqua Holdings Corporation, completed in the first quarter of 2023. This merger has positioned the combined entity for enhanced financial performance. The early 2024 results reflect the benefits of increased scale and operational synergies, indicating a strong foundation for future growth. The bank's strategic planning focuses on leveraging these strengths to drive shareholder value.

For the first quarter of 2024, Columbia Banking System reported a net income of $105.1 million, or $0.62 per diluted share. The total assets of the bank stood at $50.36 billion as of March 31, 2024. These figures highlight the bank's robust financial health and its ability to generate profits. The bank aims to maintain healthy profit margins and achieve sustainable revenue growth through its expanded customer base and diversified service offerings. This approach is crucial for achieving long-term growth potential.

Analysts generally hold a positive outlook, anticipating continued realization of merger synergies and organic growth in key markets. Management is focused on optimizing its capital structure and maintaining strong liquidity to support strategic initiatives. The company's focus remains on consistent financial performance within a competitive banking environment. To understand the bank's core principles, you can read about the Mission, Vision & Core Values of Columbia Bank.

The Columbia Bank growth strategy is centered on the successful integration of Umpqua Holdings Corporation. This merger has expanded the bank's market presence and operational capabilities. The focus is on leveraging the combined strengths to drive shareholder value and achieve consistent financial performance.

Columbia Bank future prospects look promising, supported by the strong financial performance reported in early 2024. The bank aims for sustainable revenue growth through an expanded customer base and diversified service offerings. Analysts forecast continued growth, driven by merger synergies and organic expansion in key markets.

The financial institution outlook for Columbia Bank is positive, with a focus on optimizing capital structure and maintaining strong liquidity. The banking industry trends indicate a competitive environment, but the bank is well-positioned to leverage its expanded scale. The bank's strategic planning includes risk management strategies to navigate challenges.

Bank strategic planning at Columbia Bank involves leveraging the combined entity's strengths to drive shareholder value. This includes focusing on customer acquisition strategies and digital banking initiatives. The bank is also considering branch network optimization to enhance efficiency and customer service.

Key Financial Metrics and Strategies

Columbia Bank's financial performance is driven by several key metrics and strategies. The bank focuses on maintaining healthy profit margins and achieving sustainable revenue growth. The bank's expansion plans for 2024 include leveraging the merger synergies and organic growth in key markets.

- Merger Synergies: Realizing the benefits of the Umpqua Holdings Corporation integration.

- Organic Growth: Expanding in key markets through customer acquisition and service diversification.

- Capital Optimization: Managing capital structure and maintaining strong liquidity.

- Risk Management: Implementing risk management strategies to ensure financial stability.

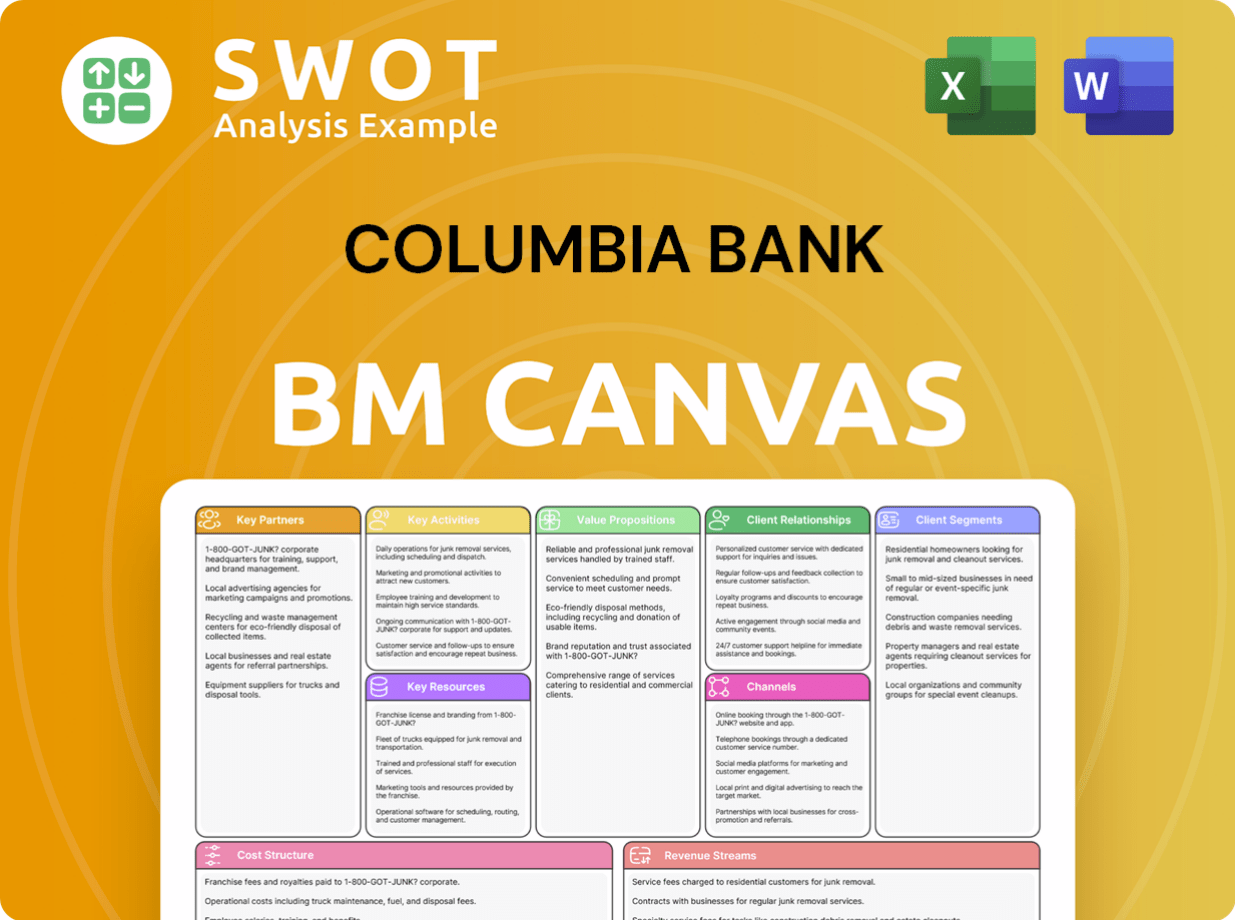

Columbia Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Columbia Bank’s Growth?

The growth strategy of Columbia Bank, especially following its merger with Umpqua Holdings Corporation, faces several potential risks and obstacles. These challenges could impact its financial performance and long-term growth potential. The Owners & Shareholders of Columbia Bank need to be aware of these factors when assessing the bank's future prospects.

A primary concern is the successful integration of the two entities. Mergers of this size often bring complexities related to integrating IT systems, aligning corporate cultures, and retaining key personnel. Failure to manage these aspects effectively could lead to operational disruptions, increased costs, and potential customer attrition, affecting the bank's market share analysis.

Market competition represents another continuous threat, particularly from larger national banks and agile fintech companies offering innovative digital solutions. Regulatory changes also pose a significant risk. The banking industry is heavily regulated, and new compliance requirements can impose substantial operational and financial burdens.

Integration Challenges

The merger integration involves combining different IT systems, which could cause delays and operational issues. Harmonizing the corporate cultures of both institutions is also crucial for maintaining employee morale and productivity. Retaining key talent and customer relationships is essential to prevent attrition and maintain revenue streams, impacting Columbia Bank's customer acquisition strategies.

Competitive Pressures

The banking industry is highly competitive, with larger banks and fintech companies constantly innovating. These competitors offer advanced digital solutions and aggressive pricing strategies. To stay competitive, Columbia Bank must continuously invest in technology and adapt its services to meet evolving customer demands. The bank's digital banking initiatives are critical for its success.

Regulatory Risks

The banking sector is subject to stringent regulations, and changes in these regulations can significantly impact operations. Compliance with new rules and requirements can be costly and time-consuming. The bank must allocate resources to ensure adherence to all regulatory standards, which can affect its profitability drivers. This also influences the bank's risk management strategies.

Economic and Financial Risks

Economic downturns, interest rate fluctuations, and credit quality deterioration can negatively affect loan portfolios. Rising interest rates can increase borrowing costs for customers, potentially leading to loan defaults. Managing these risks requires diversified lending portfolios and robust risk management frameworks. The impact of interest rates is a key factor in the bank's financial performance.

To mitigate these risks, Columbia Bank employs several strategies. These include diversifying its loan portfolio to reduce exposure to specific sectors or borrowers. The bank also uses robust risk management frameworks to identify, assess, and manage potential risks. Regular scenario planning helps the bank evaluate the potential impact of economic changes and develop mitigation strategies. These measures are vital for Columbia Bank's investment opportunities.

The bank must remain adaptable to navigate the changing economic climate and competitive landscape. This involves continuous monitoring of market trends and customer preferences. Investing in technological advancements and digital banking initiatives is crucial for staying ahead of competitors. The bank's strategic planning and its ability to adapt will determine its long-term growth potential.

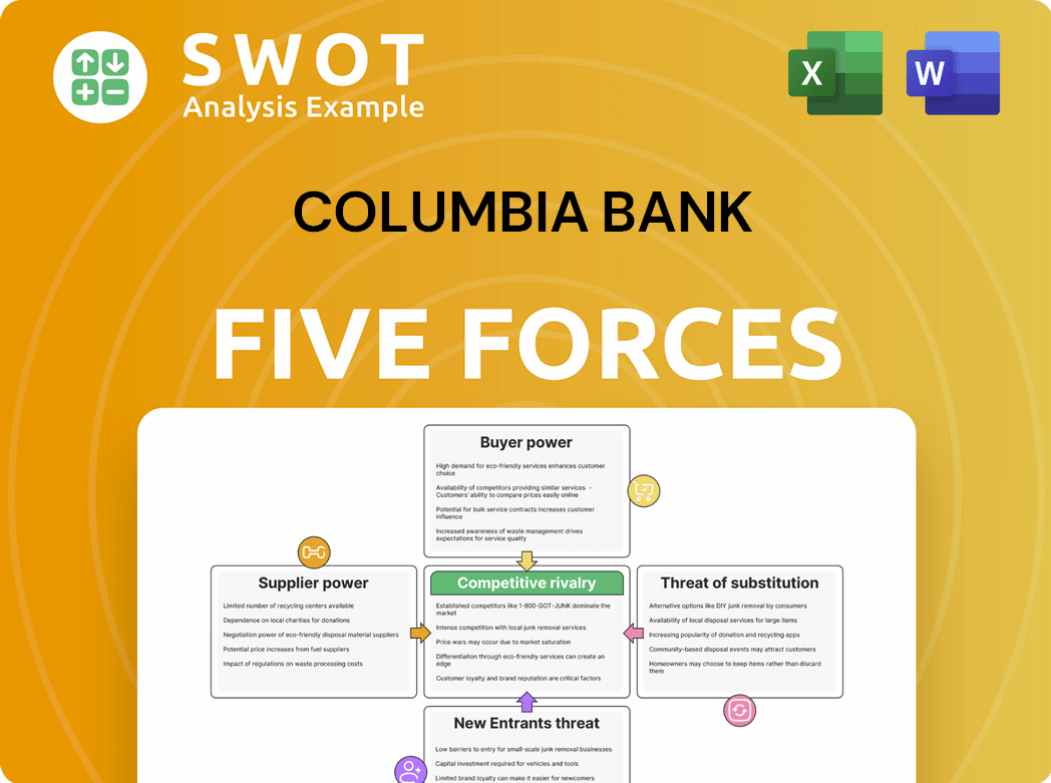

Columbia Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Columbia Bank Company?

- What is Competitive Landscape of Columbia Bank Company?

- How Does Columbia Bank Company Work?

- What is Sales and Marketing Strategy of Columbia Bank Company?

- What is Brief History of Columbia Bank Company?

- Who Owns Columbia Bank Company?

- What is Customer Demographics and Target Market of Columbia Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.