Arbor Bundle

How is Arbor Realty Trust Redefining Growth in 2025?

Arbor Realty Trust (ABR), a leading REIT in commercial real estate finance, has consistently demonstrated a robust approach to navigating market dynamics. From its strategic financial maneuvers, such as the recent $1.15 billion repurchase facility with JPMorgan Chase Bank, to its established position as a top-tier lender, Arbor's trajectory is one of calculated expansion. This analysis dives into the core of Arbor's strategic planning, examining its growth strategies and future prospects in a fluctuating economic landscape.

This exploration will delve into the Arbor SWOT Analysis, providing a comprehensive view of its strengths, weaknesses, opportunities, and threats. We'll examine Arbor's business development initiatives, including its innovative financing solutions and its ability to adapt to changing interest rate environments. Understanding Arbor Company's future market trends and competitive landscape is crucial for investors and strategists alike, and this analysis aims to provide actionable insights into the company's potential for sustained growth.

How Is Arbor Expanding Its Reach?

Arbor Realty Trust is actively pursuing several expansion initiatives to fuel its future growth. These initiatives focus on both product diversification and market penetration, demonstrating a proactive approach to adapting to evolving market conditions and maximizing opportunities. The company's strategic moves are geared towards strengthening its market position and enhancing shareholder value.

The company continues to offer a range of customized financing solutions, including bridge financing, mezzanine financing, and preferred equity investments. These solutions are tailored to meet the diverse needs of borrowers. This approach allows Arbor to cater to a broad client base, supporting its growth strategy.

Arbor's expansion initiatives are supported by its strong performance in key areas. The company's ability to adapt and innovate has been critical in navigating market challenges and capitalizing on opportunities.

In Q1 2025, Arbor generated $370 million in new bridge loans. The company is targeting $1.5 billion to $2 billion in bridge loan production for the full year 2025. This focus on bridge loans is a key component of Arbor's growth strategy.

Arbor reported $200 million in its single-family rental business and $92 million in construction lending for Q1 2025. Guidance for construction lending is set at $250 million to $500 million for 2025. These segments contribute significantly to Arbor's diversified portfolio.

Agency loan originations saw a decrease to $605.9 million in Q1 2025, a 56% drop from Q4 2024. However, the company's servicing portfolio remained stable at $33.48 billion. Arbor's agency volume guidance for 2025 is $3.5 billion to $4 billion, with a pipeline of approximately $2 billion.

Arbor successfully modified $4.1 billion in loans in 2024, with borrowers injecting an additional $130 million. This demonstrates the company's effective loan portfolio management and its ability to support borrowers. This proactive approach helps maintain portfolio quality.

Strategic Focus and Market Adaptability

Arbor's strategic focus on bridge lending and single-family rental businesses contributed to its solid performance in 2024. The company's ability to navigate a challenging market environment highlights its adaptability. These strategic moves are crucial for the Arbor Company Growth Strategy.

- Focus on expanding bridge loan production.

- Growth in the single-family rental and construction lending sectors.

- Maintaining a strong agency business with an emphasis on increasing activity.

- Effective loan portfolio management through modifications and borrower support.

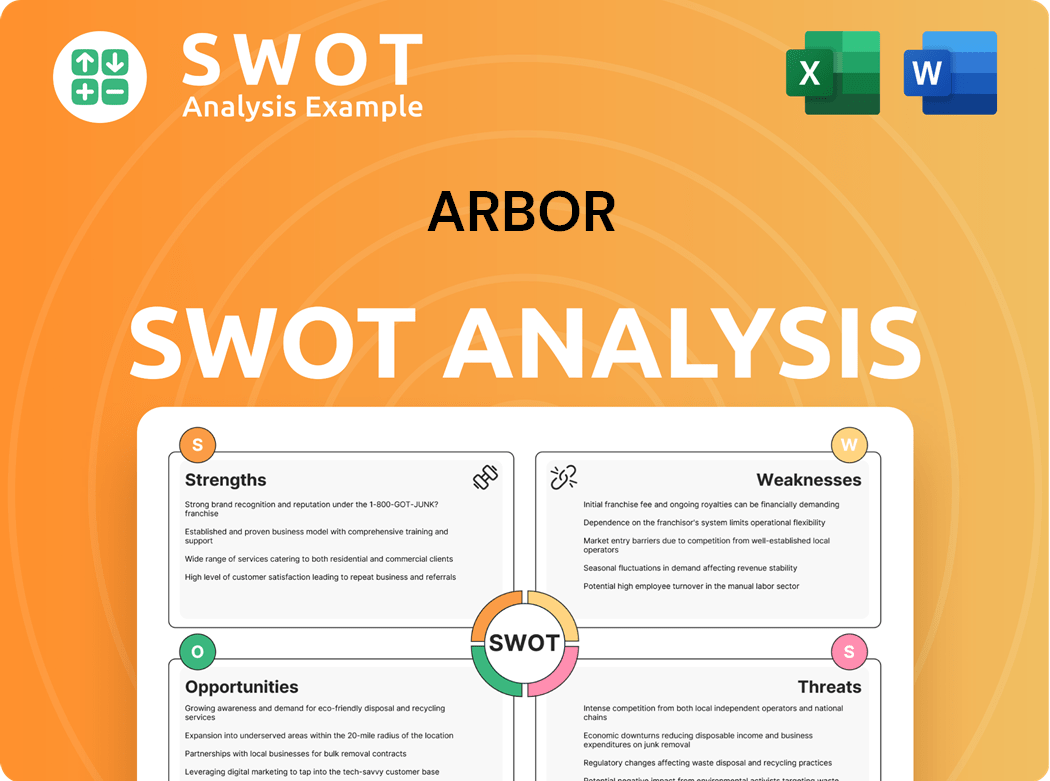

Arbor SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

How Does Arbor Invest in Innovation?

The company integrates technology and innovation to improve its operational efficiency and service offerings within the real estate finance sector. While specific details on recent research and development investments or cutting-edge technologies like artificial intelligence and the Internet of Things aren't extensively disclosed, the focus on customized solutions and efficient loan servicing suggests ongoing technological integration.

The company's platform includes various loan products such as bridge, CMBS, mezzanine, and preferred equity loans, which require robust systems for origination, underwriting, and servicing. This indicates a need for advanced technological infrastructure to manage these complex financial products effectively.

The investor relations portal and earnings call processes, including live webcasts and telephonic access, demonstrate a reliance on digital platforms for transparent communication and engagement with stakeholders. This digital presence is crucial for maintaining investor confidence and providing timely information.

Data-Driven Decision-Making

Partnering with Chandan Economics for industry-leading research reports focused on multifamily and single-family real estate investing highlights a data-driven approach. This approach relies on advanced analytical tools and data processing capabilities.

Investor Communication

The company's investor relations portal and earnings calls, which include live webcasts and telephonic access, show a reliance on digital platforms. These platforms facilitate transparent communication and engagement with stakeholders.

Technological Integration

The commitment to customized solutions and efficient loan servicing implies ongoing technological integration. This integration is essential for streamlining operations and improving customer service.

Loan Servicing Systems

The various loan products offered, such as bridge, CMBS, mezzanine, and preferred equity loans, require robust systems. These systems are necessary for origination, underwriting, and servicing.

Market Analysis Tools

The focus on providing timely research and key insights suggests an investment in information systems. These systems support strategic decision-making and thought leadership within the industry.

Strategic Decision-Making

A data-driven approach to market analysis, supported by advanced analytical tools, is crucial. This approach is essential for strategic planning and identifying opportunities.

Key Technological Aspects

The company's technological strategy focuses on enhancing operational efficiency and improving service offerings. This includes the use of digital platforms for investor relations and data-driven decision-making. For more insights, consider reading about the Marketing Strategy of Arbor.

- Data Analytics: Leveraging data analytics for market analysis and strategic planning.

- Digital Platforms: Utilizing digital platforms for investor relations, communication, and loan servicing.

- Automation: Implementing automation to streamline loan origination, underwriting, and servicing processes.

- Cybersecurity: Ensuring robust cybersecurity measures to protect sensitive financial data.

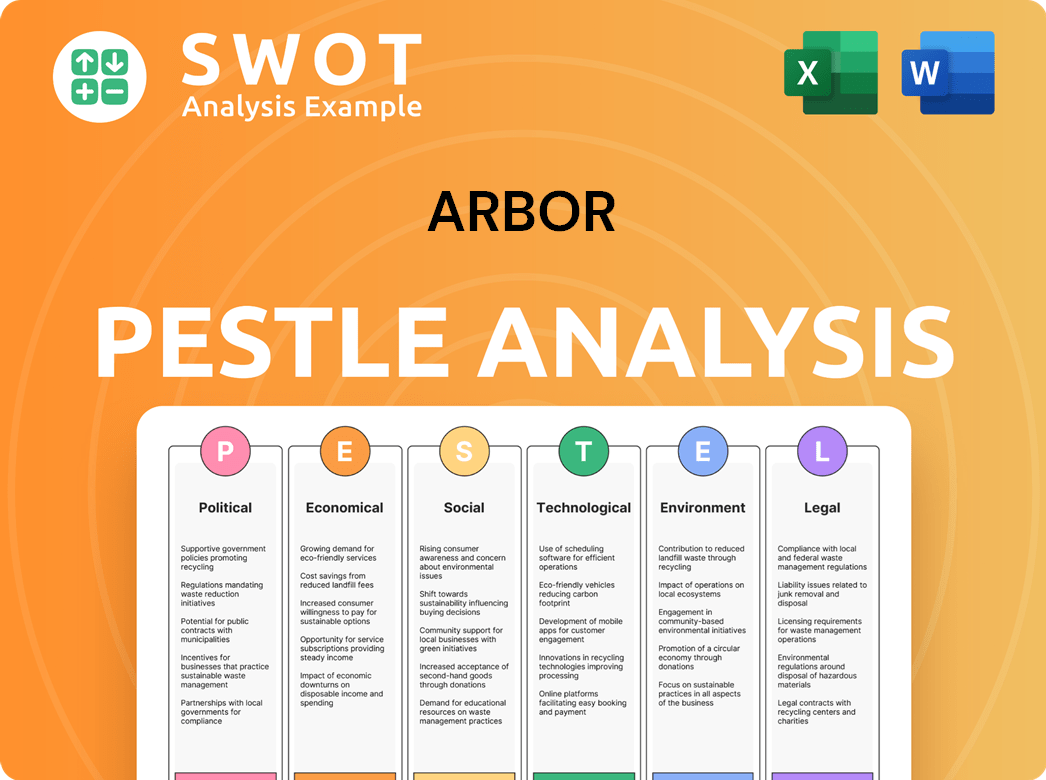

Arbor PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Is Arbor’s Growth Forecast?

The financial outlook for Arbor Realty Trust in 2025 anticipates a challenging period, yet one with the potential for growth in 2026. The company is navigating a higher interest rate environment, which impacts its originations business. Additionally, it faces earnings headwinds from real estate-owned (REO) assets and delinquencies.

In the first quarter of 2025, Arbor reported a GAAP net income of $0.16 per diluted share, a decrease from $0.31 in the first quarter of 2024. Despite these challenges, Arbor maintains a strong dividend yield and has taken steps to strengthen its financial position.

For Q1 2025, distributable earnings were $57.3 million, or $0.28 per share, with $0.31 per share excluding specific one-time losses. The company has adjusted its 2025 earnings guidance, projecting quarterly distributable earnings in the range of $0.30 to $0.35 per share. This strategic adjustment is a key part of the Revenue Streams & Business Model of Arbor, reflecting its proactive approach to market dynamics.

Interest income for Q1 2025 was $240.693 million, a decrease from $321.292 million in Q1 2024. The average balance of the loan and investment portfolio during Q1 2025 was $11.39 billion, with a weighted average yield of 8.15%.

Arbor declared a quarterly cash dividend of $0.30 per share for Q1 2025, aligning with its updated guidance. For the full year 2024, the company achieved distributable earnings of $1.74 per share.

The company's total allowance for loan losses was $240.9 million at March 31, 2025. This reflects Arbor's proactive management of risk within its loan portfolio.

Arbor successfully reduced its debt-to-equity ratio from 4:1 to 2.8:1 in 2024, representing a 30% deleveraging. In March 2025, it secured a new $1.15 billion repurchase facility, generating approximately $80 million in additional liquidity.

Strategic Financial Moves

Arbor's strategic moves, including dividend declarations and debt reduction, indicate a focus on maintaining shareholder value and financial stability. These actions are critical components of its Arbor Company Growth Strategy. The company's ability to secure a new repurchase facility also highlights its proactive approach to managing liquidity and supporting future growth.

- Focus on originations business.

- Managing REO assets.

- Maintain strong dividend yield.

- Debt-to-equity ratio reduction.

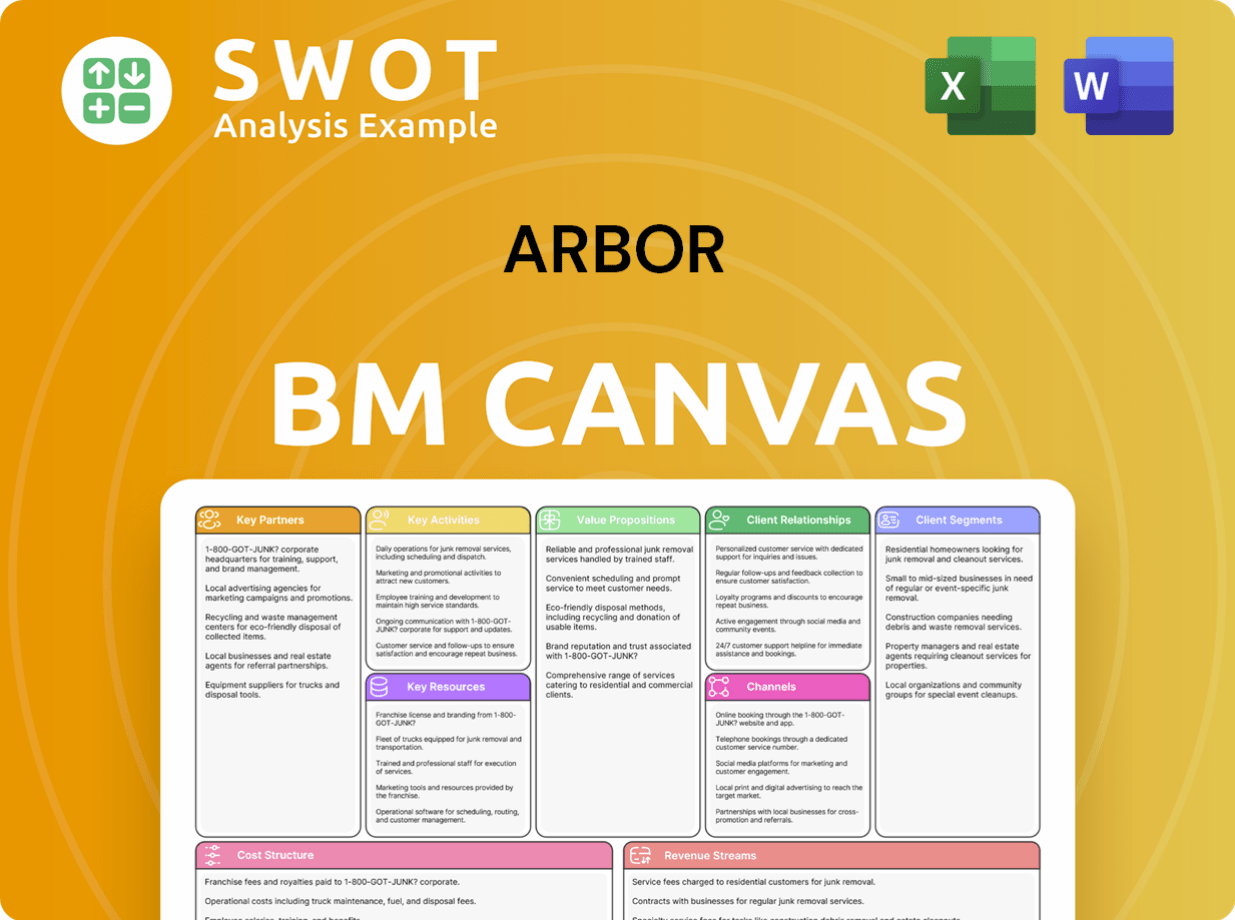

Arbor Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Risks Could Slow Arbor’s Growth?

The potential risks and obstacles for Arbor Company's growth strategy primarily stem from the volatile commercial real estate market and the impact of interest rates. These factors can significantly influence the company's financial health and operational efficiency. The company's ability to navigate these challenges will be critical for realizing its future prospects.

The prolonged instability in the commercial real estate sector, driven by inflation and high interest rates, has led to decreased property values, increased loan delinquencies, and defaults. These market conditions directly affect Arbor's business and financial performance. The company must manage these risks effectively to sustain its growth trajectory.

Arbor faces the challenge of managing loan delinquencies and real estate-owned (REO) assets, which temporarily affect earnings. The repositioning of these assets is expected to take up to 24 months. The company's strategic adjustments are aimed at mitigating potential losses and safeguarding portfolio integrity.

Market Volatility

The volatile commercial real estate market poses a significant risk, potentially impacting property values and increasing delinquencies. This instability can directly affect Arbor's financial performance and strategic goals. Understanding and adapting to market fluctuations are crucial for sustainable growth.

Interest Rate Environment

High and fluctuating interest rates remain a key challenge, possibly limiting loan origination volumes. These rates can also affect asset recovery timelines and overall profitability. Managing the impact of interest rate changes is essential for Arbor's financial planning.

Loan Delinquencies and REO Assets

Loan delinquencies and real estate-owned (REO) assets represent a temporary drag on earnings, requiring strategic management. The process of repositioning these assets can take up to 24 months, impacting short-term financial results. Effective asset management is key to minimizing losses.

Market Competition

Competition from larger banks and private lenders in the single-family rental and multifamily sectors could squeeze margins. This competitive pressure requires Arbor to continuously innovate and maintain a strong market position. Strategic planning is crucial for sustaining profitability.

Regulatory Changes

Regulatory changes in multifamily lending, such as those proposed by the FHA, could alter origination costs. Adapting to these regulatory shifts is vital for maintaining compliance and operational efficiency. The company must stay informed about evolving industry standards.

Risk Management

Arbor's rigorous risk management and underwriting practices are essential to mitigate potential losses and safeguard portfolio integrity. These practices are critical for maintaining financial stability and investor confidence. Effective risk management is central to the company's strategy.

As of March 31, 2025, the company had 23 non-performing loans with an unpaid principal balance (UPB) of $511.1 million, before related loan loss reserves. This represents a significant financial exposure that the company must actively manage. Addressing these non-performing loans is critical for maintaining financial stability.

The company took back $197 million in REO assets during Q1 2025, with plans to reposition these assets over 12 to 24 months. The successful repositioning of these assets is crucial for recovering value and improving financial performance. This process requires careful planning and execution.

Arbor's strategic adjustments, including liquidity enhancements and efficient securitization deals, are designed to navigate these challenges effectively. For more insights into the company's history and background, you can review the Brief History of Arbor.

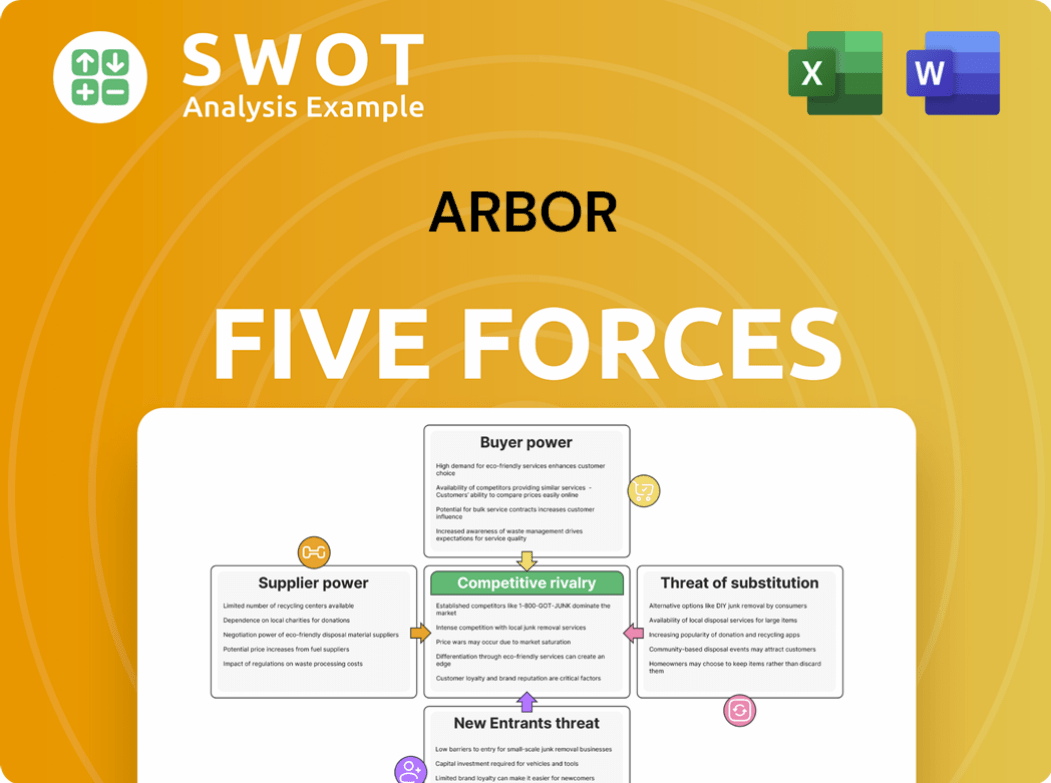

Arbor Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Arbor Company?

- What is Competitive Landscape of Arbor Company?

- How Does Arbor Company Work?

- What is Sales and Marketing Strategy of Arbor Company?

- What is Brief History of Arbor Company?

- Who Owns Arbor Company?

- What is Customer Demographics and Target Market of Arbor Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.