The Delivery Group Bundle

How Does The Delivery Group Stack Up in the UK Delivery Arena?

The UK delivery sector is a battlefield, constantly reshaped by e-commerce booms and shifting consumer demands. Understanding the The Delivery Group SWOT Analysis is crucial to grasping its position. This analysis delves into the competitive landscape to uncover key players and the strategies shaping the future of parcel and mail delivery.

This exploration of the Delivery Group's competitive landscape will dissect its market position, examining its services and business model within the Delivery Group industry. We will analyze its key competitors, assessing their strengths and weaknesses to provide a comprehensive Delivery Group market analysis. This will help you understand who are Delivery Group's main rivals and how they compare in terms of market share and customer satisfaction, offering valuable insights into the company's growth strategy and future outlook.

Where Does The Delivery Group’ Stand in the Current Market?

The Delivery Group holds a significant position within the UK's Downstream Access (DSA) market, particularly excelling in high-volume mail and parcel distribution. The company's core operations encompass mail sortation, delivery management, and comprehensive e-commerce fulfilment services. Their services cater to a diverse customer base, including retail, financial services, and public sectors.

The company strategically focuses on efficiency and cost-effectiveness, crucial in the competitive landscape. This focus allows them to offer competitive solutions for high-volume logistics. The Delivery Group has expanded its services beyond traditional mail to encompass the fast-growing e-commerce sector, reflecting a strategic shift to capture growth opportunities in online retail.

Geographically, The Delivery Group primarily operates within the UK, utilizing a network of hubs and partnerships for nationwide coverage. This strategic positioning supports their ability to compete effectively. The company's ability to offer cost-effective solutions for high-volume logistics positions it favorably against traditional postal operators.

While specific market share figures for 2024-2025 are proprietary, the DSA market remains a significant segment within the broader postal services industry. The Delivery Group competes with other key players for a substantial share of business mail and e-commerce parcels. The company's focus on high-volume distribution is a key aspect of its business model.

The company provides mail sortation, delivery management, and e-commerce fulfilment services. Their services are designed to meet the needs of various sectors, including retail and financial services. The expansion into e-commerce fulfilment reflects a strategic move to capitalize on the growth in online retail.

The Delivery Group's operations are primarily concentrated within the UK. They leverage a network of hubs and partnerships to ensure efficient nationwide coverage. This strategic geographic focus allows them to compete effectively in the delivery market.

Industry assessments often highlight the company's operational scale and efficiency as key strengths. Their ability to offer cost-effective solutions for high-volume logistics positions them favorably. The focus on efficiency is a critical factor in the Delivery Group competitive landscape.

Key Strengths and Competitive Advantages

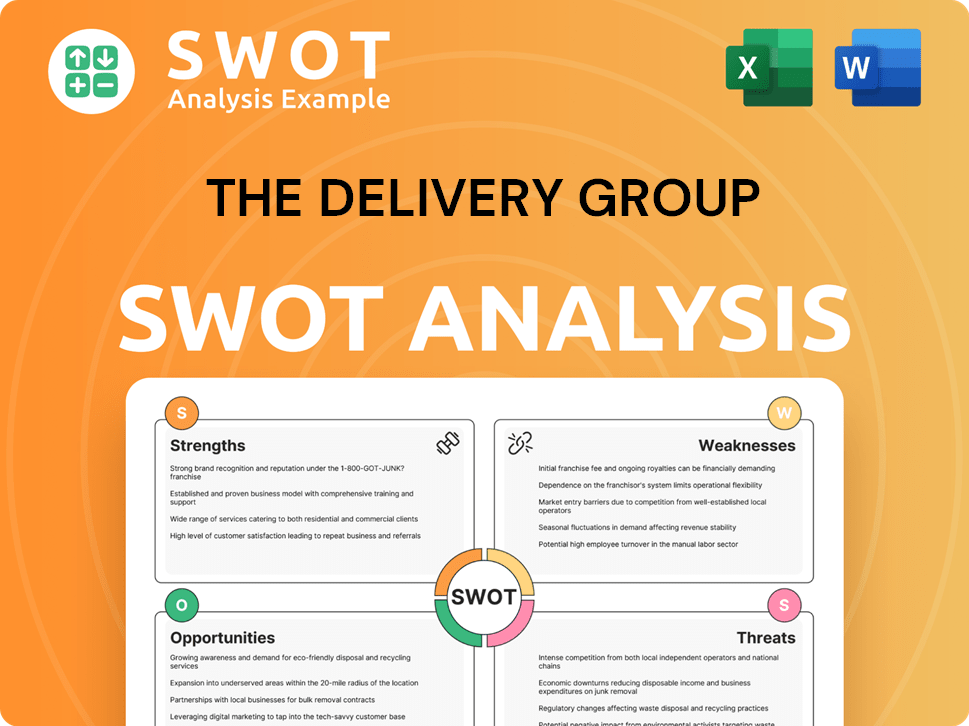

The Delivery Group's strengths lie in its operational scale, efficiency, and focus on high-volume logistics. This positions them well against traditional postal operators and other Delivery Group competitors. Their expansion into e-commerce demonstrates a proactive approach to market changes.

- Cost-effective solutions for high-volume logistics.

- Strong presence in the B2B mail sector.

- Expanding footprint in the B2C e-commerce fulfilment space.

- Strategic partnerships for nationwide coverage.

The Delivery Group SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging The Delivery Group?

The Growth Strategy of The Delivery Group operates within a competitive landscape, facing challenges from both established postal services and agile logistics providers. Understanding the key competitors is crucial for assessing its market position and future prospects. This analysis provides insights into the competitive dynamics within the direct mail, DSA, and broader e-fulfilment sectors.

The competitive environment is shaped by factors such as pricing, service reliability, technological innovation, and geographical reach. The company's ability to navigate this landscape will significantly influence its financial performance and market share. The following sections delve into the specific competitors and their strategies.

Direct Mail and DSA Competitors

In the direct mail and DSA sector, the primary competitor is Royal Mail. Other significant competitors include Whistl and UK Mail (now part of DHL Parcel UK).

Royal Mail

Royal Mail, as the incumbent, remains a key competitor, also acting as a final-mile delivery partner for DSA providers. Royal Mail's extensive network and brand recognition give it a strong position in the market. In 2024, Royal Mail's revenue from letters and parcels was approximately £4.6 billion.

Whistl

Whistl is a major player in bulk mail, offering similar DSA services and competing on price and service efficiency. Whistl has been expanding its services and infrastructure to increase its market share. Whistl's annual revenue in 2024 was estimated to be around £700 million.

UK Mail (DHL Parcel UK)

UK Mail, now part of DHL Parcel UK, provides a comprehensive range of parcel and mail services, leveraging a strong international network. DHL's backing provides significant resources and a global reach. DHL Parcel UK's revenue in 2024 was approximately £1.2 billion.

E-fulfilment and Parcel Delivery Competitors

In the broader e-fulfilment and parcel delivery market, the company faces competition from global logistics giants such as DPD, Evri (formerly Hermes), and Amazon Logistics.

DPD

DPD is strong in the B2C parcel delivery segment, offering advanced tracking and flexible delivery options. DPD has invested heavily in its infrastructure and technology. DPD's revenue in the UK in 2024 was around £2.3 billion.

Evri (formerly Hermes)

Evri is another major player in the B2C parcel delivery market, known for its competitive pricing and extensive network. Evri handles a significant volume of parcels, particularly for e-commerce businesses. Evri's revenue in 2024 was approximately £1.8 billion.

Amazon Logistics

Amazon Logistics, while primarily serving Amazon's e-commerce operations, is expanding its delivery network and services, posing a competitive challenge. Amazon's logistics arm leverages its vast infrastructure and technological capabilities. Amazon Logistics' revenue from third-party deliveries in the UK was estimated at £1.5 billion in 2024.

Competitive Strategies and Market Dynamics

The competitive dynamics in the delivery market are shaped by several factors, including pricing strategies, technological innovation, and brand recognition. The company's ability to compete effectively depends on its ability to offer competitive pricing, reliable service, and innovative solutions. The market is also influenced by mergers and acquisitions, such as DHL's acquisition of UK Mail, which lead to consolidation and increased competition.

- Pricing Strategies: Competitors often employ aggressive pricing to gain market share, particularly in the bulk mail and parcel delivery segments.

- Technological Innovation: Continuous innovation in delivery technology, such as real-time tracking and locker networks, is crucial for maintaining a competitive edge.

- Service Reliability: Ensuring reliable and timely delivery is essential for customer satisfaction and retention.

- Brand Recognition: Strong brand recognition and reputation can attract customers and build loyalty.

- Geographic Reach: Extensive distribution networks and geographic coverage are critical for serving a wide range of customers.

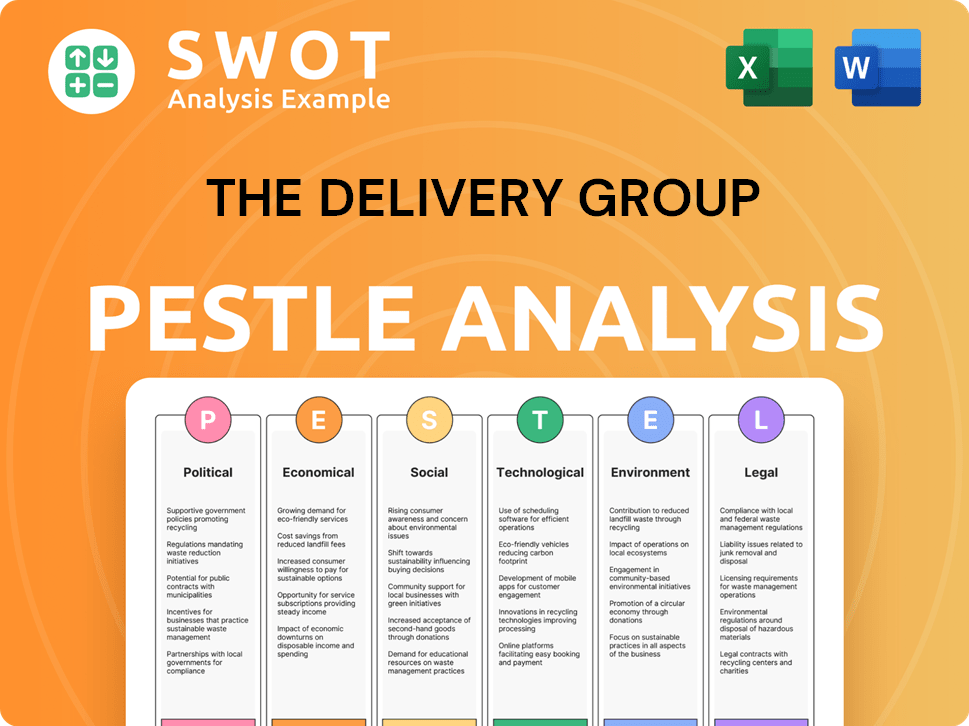

The Delivery Group PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives The Delivery Group a Competitive Edge Over Its Rivals?

The Brief History of The Delivery Group showcases its evolution and strategic positioning within the delivery sector. The company has carved a niche for itself, focusing on Downstream Access (DSA) services, which allows it to optimize mail and parcel sortation. This specialization enables cost-effective solutions for high-volume clients, a key aspect of its competitive strategy.

The Delivery Group's business model emphasizes operational efficiency and strategic partnerships. By managing the initial stages of mail and parcel processing and integrating with final-mile delivery networks, it offers competitive pricing. This approach allows the company to maintain a strong market presence without the overhead of a complete end-to-end delivery infrastructure.

Furthermore, the company has adapted to the e-commerce boom by expanding its services to include warehousing and pick-and-pack operations. The company's ability to optimize existing technologies and processes for efficiency is a significant advantage. This adaptability has been crucial for maintaining its competitive edge in a dynamic market.

The Delivery Group's expertise in Downstream Access (DSA) allows it to optimize mail and parcel sortation, which is a key differentiator. This specialization enables the company to offer cost-effective solutions. This focus on efficiency has helped them carve out a niche in the Delivery Group competitive landscape.

The company leverages a robust network and strategic partnerships to ensure nationwide reach and reliability. This hybrid model allows it to offer competitive pricing without the overhead of managing a complete delivery infrastructure. These partnerships are vital for maintaining its competitive advantages.

The Delivery Group has expanded its services to meet the needs of e-commerce businesses, including warehousing and pick-and-pack services. This expansion has allowed them to adapt to the evolving demands of online retail. This adaptability is a key factor in the company's growth strategy in the delivery market.

The company focuses on building strong client relationships and offering tailored solutions for diverse business needs. This customer-centric approach contributes to customer loyalty. This focus on customer satisfaction is crucial for maintaining its competitive edge.

Key Competitive Advantages

The Delivery Group's competitive advantages are rooted in its operational model, strategic partnerships, and adaptability to market changes. Its focus on DSA services and e-commerce fulfilment positions it well within the Delivery Group industry. The company's ability to offer tailored solutions and maintain strong client relationships is crucial for sustained growth.

- Specialized expertise in Downstream Access (DSA) for optimized sortation.

- Robust network and strategic partnerships for nationwide reach.

- Adaptability to e-commerce demands through warehousing and fulfilment services.

- Focus on customer relationships and tailored solutions.

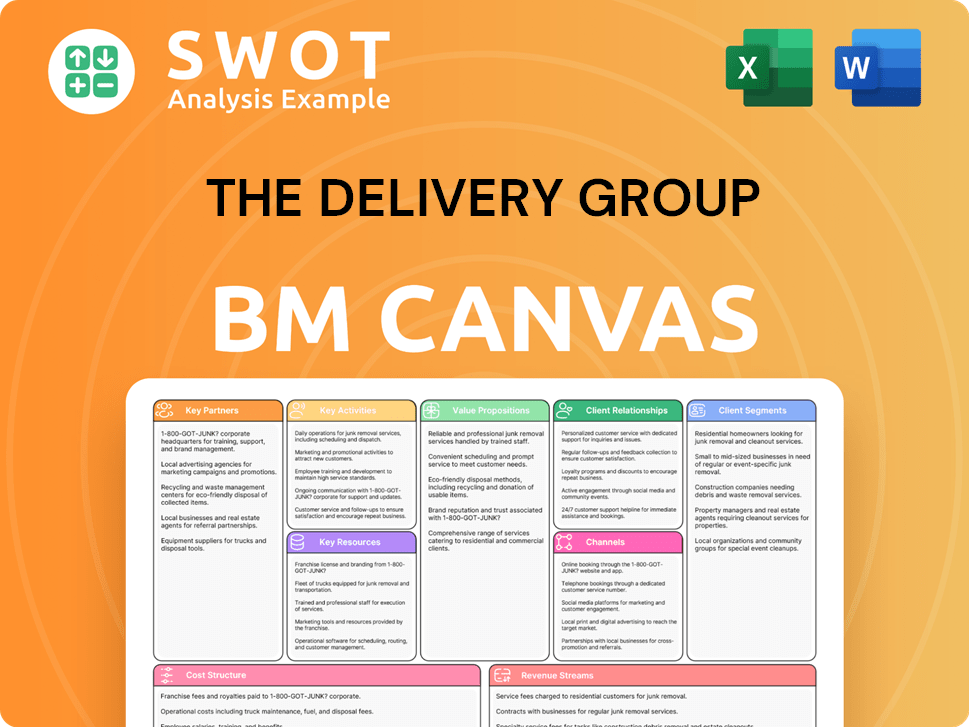

The Delivery Group Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping The Delivery Group’s Competitive Landscape?

The delivery industry, including the Delivery Group, is experiencing significant shifts driven by e-commerce growth and technological advancements. Understanding the Delivery Group competitive landscape requires an analysis of these industry trends, potential challenges, and emerging opportunities. The company's future outlook depends on its ability to adapt and innovate within this dynamic environment.

The Delivery Group faces challenges such as managing rising operational costs and intense competition from established and emerging players. However, the continued expansion of e-commerce and the increasing demand for efficient delivery services present significant opportunities for growth. A comprehensive Delivery Group market analysis is crucial for strategic decision-making.

E-commerce continues to grow exponentially, driving demand for delivery services. Consumer preferences are evolving towards faster and more sustainable delivery options. Technological advancements, such as automation and AI, are transforming logistics operations. Regulatory changes impact environmental impact and labor practices.

Managing escalating e-commerce parcel volumes while maintaining cost-effectiveness. Increased competition from global logistics companies with advanced technology. Rising fuel and labor costs, impacting operational margins. The need to adapt to new market entrants offering specialized solutions.

Expanding its network and investing in automation and data analytics. Capitalizing on the increasing demand for sustainable logistics solutions. Exploring niche markets requiring specialized handling or international e-commerce fulfilment. Leveraging its DSA expertise to strengthen e-commerce capabilities.

Focus on integrating logistics services to remain competitive. Strengthening its e-commerce capabilities to meet market demands. Adapting to technological advancements and regulatory changes. Developing strategic partnerships to enhance service offerings.

Key Factors Influencing the Delivery Group's Competitive Position

The Delivery Group's ability to navigate the evolving Delivery Group industry depends on several key factors. These include its operational efficiency, technological adoption, and strategic partnerships. Furthermore, understanding the Delivery Group's business model and its adaptability to market changes is crucial.

- E-commerce Growth: E-commerce sales are projected to reach $7.9 trillion globally by 2026, increasing the demand for delivery services.

- Last-Mile Delivery: The last-mile delivery segment is expected to grow significantly, with the market size estimated to reach $125 billion by 2028.

- Technological Integration: Investment in automation and AI-driven logistics is increasing, with companies allocating a significant portion of their budgets to these technologies.

- Sustainability: The demand for sustainable delivery options is rising, with consumers increasingly prioritizing eco-friendly practices.

- Competitive Landscape: The competitive landscape is intense, with major players like UPS and FedEx, and emerging players, competing for market share. For example, a 2024 report indicates that UPS holds approximately 22% of the global market share in package delivery.

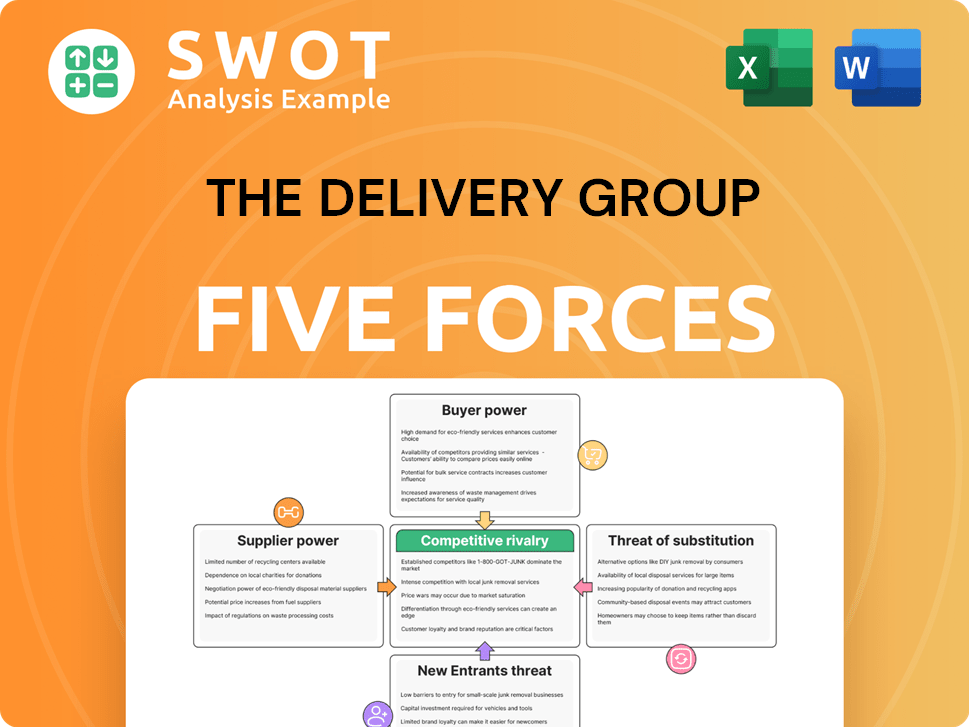

The Delivery Group Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of The Delivery Group Company?

- What is Growth Strategy and Future Prospects of The Delivery Group Company?

- How Does The Delivery Group Company Work?

- What is Sales and Marketing Strategy of The Delivery Group Company?

- What is Brief History of The Delivery Group Company?

- Who Owns The Delivery Group Company?

- What is Customer Demographics and Target Market of The Delivery Group Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.