Old Second Bundle

How Does Old Second Company Thrive in a Competitive Banking Arena?

Navigating the complex waters of the Old Second SWOT Analysis is crucial for any investor or strategist. The financial services market is a battlefield, and understanding the Old Second Company competitive landscape is paramount. This analysis dives deep into the challenges and opportunities facing Old Second Bank, a key player in the Chicago area.

Understanding Old Second Bank competitors is vital for assessing its market position. This exploration of the banking industry competition will reveal the key rivals and the strategies Old Second employs to maintain its edge. We'll examine its financial performance compared to competitors, its market share in Illinois, and its strategic initiatives to ensure long-term success in the face of evolving customer expectations and technological advancements.

Where Does Old Second’ Stand in the Current Market?

Old Second Bancorp, Inc. maintains a solid market position within the competitive Illinois banking sector. The bank's core operations revolve around offering a comprehensive suite of financial products and services. These include deposit accounts, various loan products, wealth management, trust, and treasury management services, designed to cater to a diverse customer base.

The value proposition of Old Second centers on its community-focused approach, emphasizing personalized service and local decision-making. This strategy has allowed the bank to cultivate strong relationships with its customers. While embracing digital transformation, the bank remains committed to its traditional relationship banking model, differentiating itself from larger institutions.

Old Second has a strong localized presence, particularly in the suburban markets surrounding Chicago. Its operations are concentrated in key counties within the greater Chicago metropolitan area, including Kane, DuPage, Kendall, and Will counties. This focused regional strategy allows the bank to leverage its deep understanding of local market dynamics and foster strong community ties.

For the fiscal year ending December 31, 2024, the company reported a net income of $58.1 million. Its return on average assets (ROAA) and return on average equity (ROAE) metrics generally align with or slightly exceed those of its peer group, indicating efficient asset utilization and profitability.

Old Second's competitive advantages stem from its long-standing presence and tailored services within specific community markets. This allows it to compete effectively against both larger national banks and smaller, independent local banks. The bank focuses on personalized service and local decision-making, which helps it retain a loyal customer base.

As of late 2024, Old Second reported total assets of approximately $6.2 billion, positioning it among the larger community banks in the region. Its market share within its primary service areas reflects a strong localized presence. While its market share in the overall Illinois banking market is modest compared to giants like JPMorgan Chase or Bank of America, Old Second holds a particularly strong position in several of its specific community markets.

Analyzing the Brief History of Old Second provides additional context to its market position. The bank's strategic initiatives, such as embracing digital transformation while maintaining a community focus, contribute to its ability to compete in the financial services market. The competitive landscape of Old Second Company includes both national and local banks, making its ability to maintain a strong market position crucial for its future growth.

Key Takeaways

Old Second Bank's competitive advantages include its focus on personalized service and local decision-making, allowing it to maintain a loyal customer base. The bank's financial performance, with a net income of $58.1 million in 2024, reflects efficient asset utilization. Understanding the Old Second Company competitive landscape is vital for investors and analysts.

- Strong localized presence in key suburban markets.

- Emphasis on traditional relationship banking.

- Competitive edge against both national and local banks.

- Focus on community-focused banking.

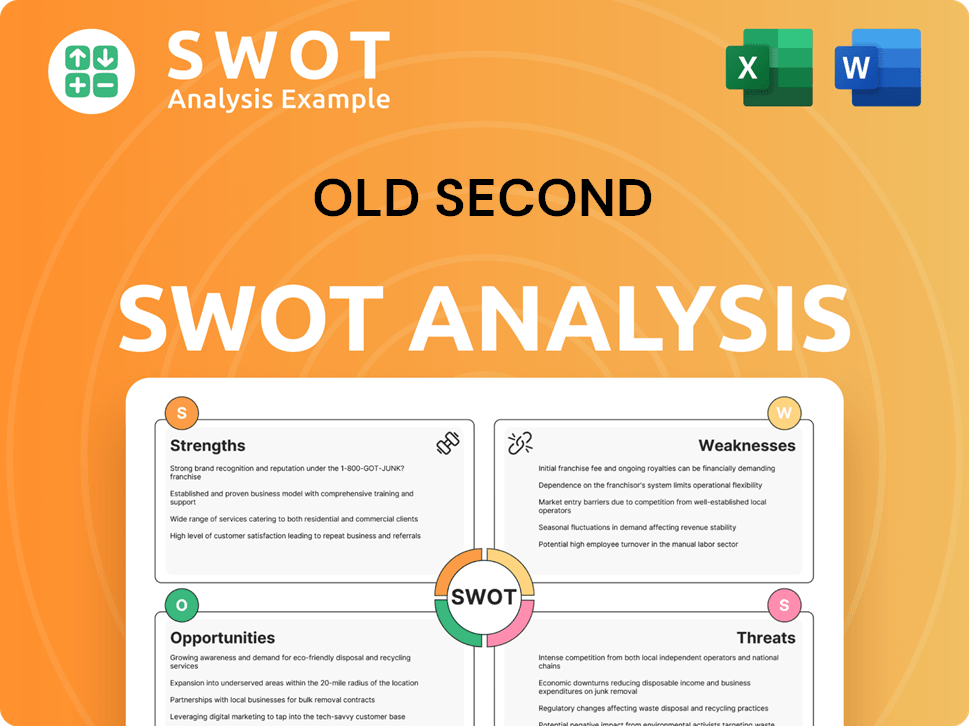

Old Second SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging Old Second?

The competitive landscape for Old Second Bancorp, Inc. is characterized by intense competition within the greater Chicago area's banking sector. This environment is shaped by a diverse range of financial institutions, from regional and community banks to national and super-regional players, as well as emerging fintech companies. Understanding the competitive dynamics is crucial for assessing Old Second's market position and strategic initiatives, including its Growth Strategy of Old Second.

The banking industry in the region is highly fragmented, with numerous institutions vying for market share. This fragmentation, combined with the presence of both traditional and non-traditional competitors, creates a complex environment where Old Second must navigate challenges and capitalize on opportunities to maintain and enhance its competitive position. The competitive landscape analysis requires a detailed examination of key players, their strategies, and their impact on Old Second's performance.

Old Second faces direct competition from regional and community banks that have a strong presence in the same geographic markets. These institutions offer similar products and services, often competing on local market presence and community engagement. This competition includes institutions like Wintrust Financial Corporation, which operates a large network of community bank subsidiaries across Chicagoland, offering a similar range of deposit and loan products. First Midwest Bancorp, prior to its acquisition by Old National Bancorp, was a major competitor with a significant footprint, and the resulting entity has become a larger regional player.

Direct Competitors

Direct competitors include regional and community banks that offer similar deposit and loan products. These banks often compete on local market presence and community engagement. Key players include Wintrust Financial Corporation, and Byline Bancorp, Inc.

Indirect Competitors

Indirect competition comes from larger national and super-regional banks, such as JPMorgan Chase, Bank of America, and Wells Fargo. These banks have vast resources and extensive branch networks. Credit unions also pose indirect competition, particularly for retail banking services.

Emerging Competitors

Fintech companies specializing in online lending, payment processing, and digital-only banking are emerging competitors. These companies challenge traditional banks on efficiency and user experience. Market shifts, such as mergers and acquisitions, intensify competition.

Competitive Strategies

Competition involves factors like scale, technological innovation, and pricing power. Larger institutions often compete on these aspects. Community banks focus on local market presence and community engagement. Fintechs compete on efficiency and user experience.

Market Dynamics

Consolidation within the banking industry intensifies competition, creating larger entities with enhanced capabilities. Mergers can increase market share concentration, leading to greater pricing pressure for smaller institutions. Recent trends impact Old Second's market position.

Impact of Fintech

Fintech companies are disintermediating specific product lines, challenging traditional banks. Their focus on efficiency and user experience attracts customers. Fintechs' impact requires banks to adapt and innovate to stay competitive.

Key Competitive Factors

The competitive landscape is shaped by several factors. These include the size and scope of competitors, their financial resources, and their strategic focus. Understanding these factors is essential for a comprehensive financial analysis.

- Market Share: Analyzing the market share of competitors provides insights into their dominance and influence.

- Product and Service Offerings: Comparing the range of products and services offered by competitors helps identify strengths and weaknesses.

- Pricing Strategies: Evaluating the pricing strategies of competitors reveals their approach to attracting and retaining customers.

- Technological Innovation: Assessing the technological capabilities of competitors highlights their ability to adapt and compete in the digital age.

- Customer Service: Examining customer service quality provides insights into customer satisfaction and loyalty.

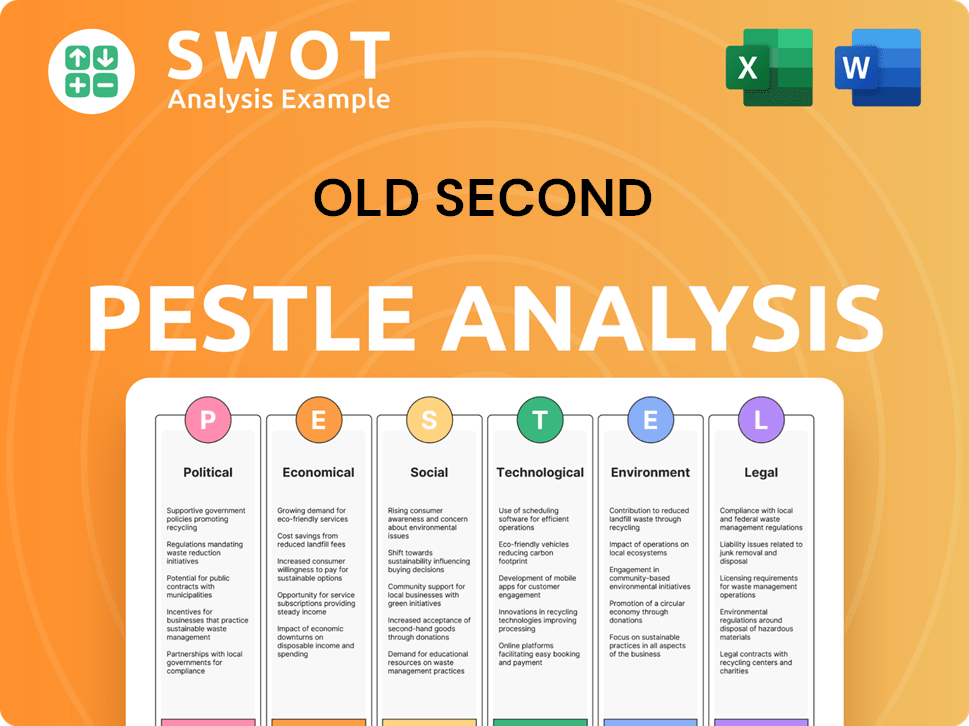

Old Second PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives Old Second a Competitive Edge Over Its Rivals?

Old Second Bancorp, Inc. navigates the Old Second Company competitive landscape by leveraging a blend of traditional strengths and modern adaptations. The bank's enduring presence, spanning over 150 years, has cultivated significant brand equity and customer loyalty, particularly within its local Illinois markets. This long-standing history forms a solid foundation for its competitive advantage, allowing it to build trust and develop personalized relationships with customers, setting it apart from larger, less regionally focused institutions. This deep-rooted community focus is a key differentiator in the banking industry competition.

A core competitive advantage is the relationship-based banking model, especially in commercial lending. Old Second emphasizes direct, personal interactions with business clients, providing customized financial solutions that go beyond standard loan products. This approach often leads to stronger client relationships and repeat business, contributing to its ability to maintain a stable market position. Furthermore, the bank has strategically invested in digital banking platforms to enhance customer convenience, ensuring it remains competitive in terms of accessibility while retaining its personal touch. This hybrid approach is a key element in its Old Second Financial analysis.

The bank's relatively lean operational structure, compared to larger national banks, allows for greater agility and potentially lower overhead costs. This can translate into competitive pricing for certain products or better returns, enhancing its market position. The bank's consistent profitability and sound financial health further contribute to its stability and ability to invest in growth initiatives. For instance, in 2024, Old Second reported a net income of $58.1 million, reflecting its financial strength and resilience within the competitive landscape.

Old Second's deep-rooted community ties and long-standing presence foster trust and customer loyalty. This localized approach allows for a better understanding of local market needs. This intimate knowledge enables tailored product offerings and responsive service, distinguishing it from larger competitors.

The bank emphasizes direct, personal interactions with business clients, providing customized financial solutions. This approach leads to stronger client relationships and repeat business. This model extends beyond standard loan products to include treasury management and advisory services.

Strategic investments in digital banking platforms enhance customer convenience and accessibility. This ensures the bank remains competitive in terms of accessibility while retaining its personal touch. This blend of traditional relationship banking with modern digital capabilities provides a hybrid advantage.

A relatively lean operational structure allows for greater agility and potentially lower overhead costs. This can translate into competitive pricing for certain products or better returns. This efficiency contributes to the bank's overall financial health and stability.

Key Competitive Advantages

Old Second's competitive edge stems from its community focus, relationship-based banking, and operational efficiency. These strengths are continually reinforced through local marketing, community involvement, and personalized customer service. These factors make it challenging for competitors to fully replicate its localized market penetration and customer loyalty, as highlighted in the Old Second Bank competitors analysis.

- Strong brand recognition and customer loyalty due to its long history.

- Personalized service and customized financial solutions.

- Efficient operations leading to competitive pricing and better returns.

- Strategic investments in digital banking for enhanced customer convenience.

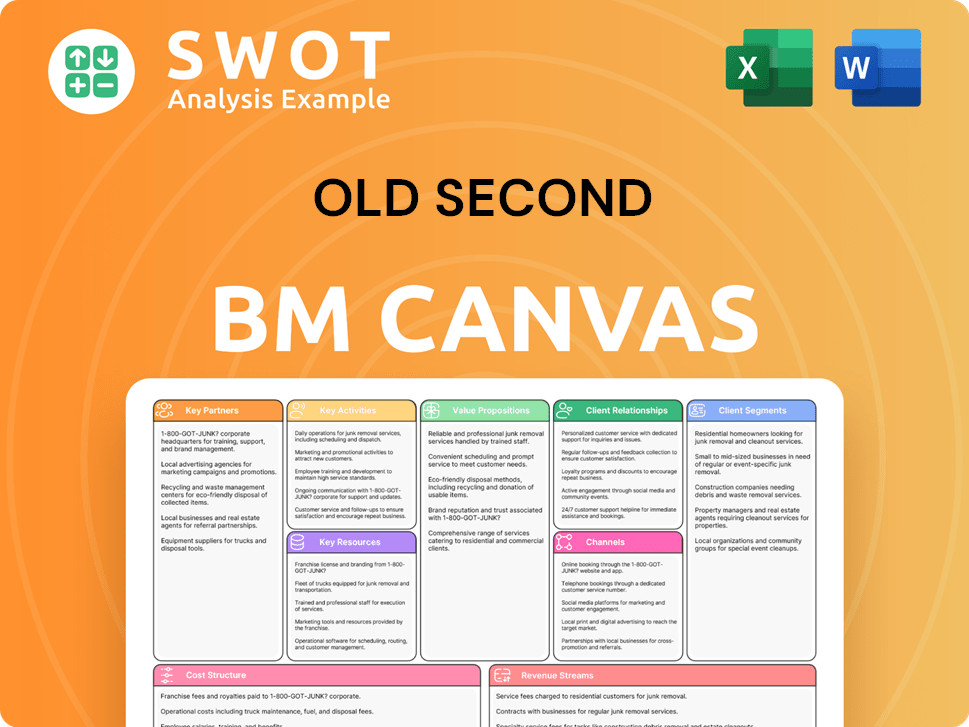

Old Second Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping Old Second’s Competitive Landscape?

The competitive landscape for Old Second Bancorp, Inc. is shaped by the dynamic banking industry, where technological advancements, regulatory changes, and economic fluctuations continuously redefine the playing field. Understanding the industry trends, future challenges, and opportunities is crucial for assessing Old Second's market position and future prospects. A Marketing Strategy of Old Second can further illuminate how the company navigates this environment.

The financial services market is experiencing rapid transformation, driven by customer expectations for digital banking solutions and the rise of fintech companies. This necessitates a proactive approach to innovation and strategic partnerships to remain competitive. Furthermore, geopolitical uncertainties and macroeconomic conditions, such as interest rate changes, can significantly impact the bank's performance, demanding a flexible and resilient business model.

The banking industry is increasingly influenced by technological advancements, with a strong emphasis on digital banking and data analytics. Customers now expect seamless digital experiences, driving banks to invest heavily in their digital infrastructure. Regulatory changes, including those related to data privacy and cybersecurity, are also shaping the industry.

Key challenges include the need to keep pace with fintech innovators, manage increasing compliance costs, and navigate geopolitical and macroeconomic uncertainties. Economic downturns and changes in interest rates can directly impact loan demand and credit quality. Furthermore, maintaining customer loyalty in a competitive market requires continuous improvement of service offerings.

Opportunities lie in leveraging data analytics for personalized services, expanding into underserved markets, and forming strategic partnerships with fintech companies. The demand for personalized financial advice and community-focused banking services remains strong. Focusing on these areas can enhance customer relationships and drive growth.

Old Second's community-centric model positions it well to capitalize on the demand for personalized services. Its focus on local markets allows for deeper customer relationships and targeted service offerings. Strategic partnerships and digital enhancements can further strengthen its competitive edge in the financial services market.

Strategic Initiatives and Outlook

To thrive, Old Second will likely focus on digital capabilities, branch network optimization, and maintaining strong credit quality. The bank might selectively pursue growth opportunities aligned with its community banking ethos. This includes expanding into underserved segments and deepening relationships with existing clients. Recent data indicates that community banks are increasingly focusing on digital transformation to meet customer demands, with a projected increase in digital banking adoption by 15% in the next two years.

- Enhance digital banking platforms and mobile applications.

- Leverage data analytics to personalize customer experiences and product offerings.

- Explore strategic partnerships with fintech companies to expand service offerings.

- Focus on maintaining strong credit quality and capital positions.

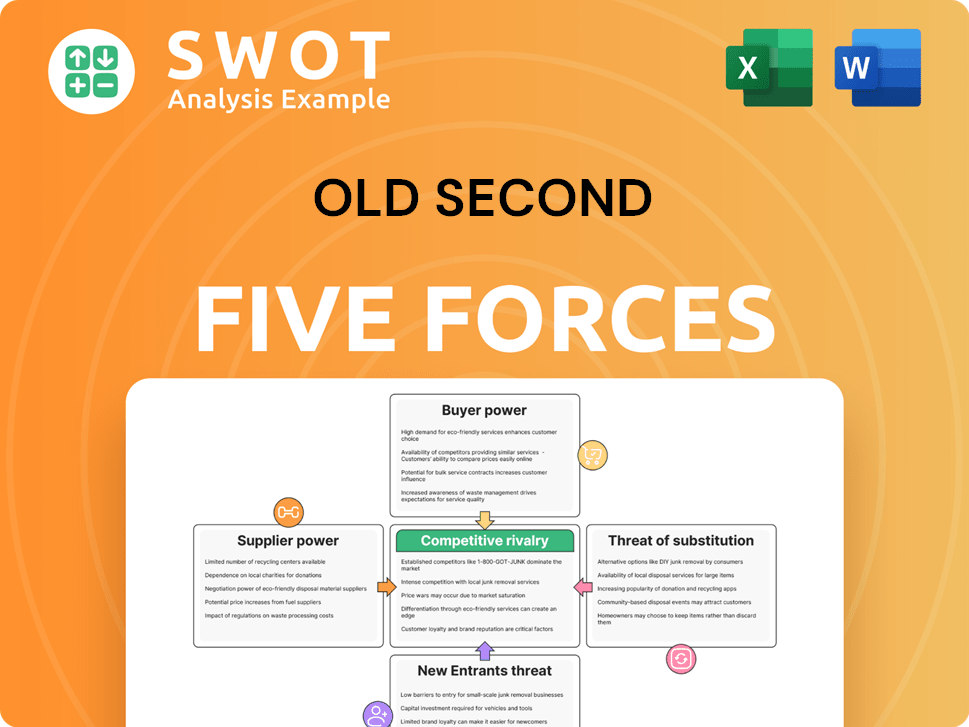

Old Second Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Old Second Company?

- What is Growth Strategy and Future Prospects of Old Second Company?

- How Does Old Second Company Work?

- What is Sales and Marketing Strategy of Old Second Company?

- What is Brief History of Old Second Company?

- Who Owns Old Second Company?

- What is Customer Demographics and Target Market of Old Second Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.