New York Community Bank Bundle

Can NYCB Thrive in Today's Banking Battleground?

New York Community Bank (NYCB) is currently navigating a complex financial terrain, making its competitive landscape a focal point for anyone tracking the banking industry. Recent strategic shifts and market pressures have put NYCB under the microscope, demanding a deep dive into its rivals and strategic positioning. Understanding the competitive dynamics is now more crucial than ever for investors and analysts alike.

This analysis explores the New York Community Bank SWOT Analysis, its key competitors, and strategies to maintain its market share. We'll examine the financial performance of New York Community Bank, its competitive advantages, and how it stacks up against other financial institutions. This comprehensive market analysis will provide actionable insights into NYCB's position within the banking sector and its future prospects in a challenging environment, considering the impact of interest rates and the latest news about New York Community Bank's competition.

Where Does New York Community Bank’ Stand in the Current Market?

New York Community Bancorp (NYCB) holds a significant position within the regional banking industry, particularly in the New York City metropolitan area. As of early 2024, NYCB reported total assets of $112.9 billion, positioning it as a notable player among regional banks in the United States. Its core operations historically centered on multi-family lending, with a strong focus on rent-regulated buildings in the New York City area, where it has established a substantial market presence.

Beyond its specialization in multi-family lending, NYCB also offers commercial real estate loans, specialty finance, and a range of commercial and retail banking services. Its geographic footprint extends through a branch network primarily across New York, New Jersey, Ohio, Florida, and Arizona, serving individuals, families, and businesses. The acquisition of Flagstar Bank in December 2022 marked a strategic move to diversify its operations.

However, the competitive landscape for NYCB has seen shifts. The bank reported a net loss of $2.7 billion in the fourth quarter of 2023, largely due to a $2.4 billion goodwill impairment charge related to the Flagstar acquisition and increased provisions for credit losses. This financial performance, coupled with a significant dividend cut and credit rating downgrades in early 2024, indicates a period of vulnerability and re-adjustment for NYCB within the competitive market.

NYCB has a strong presence in the New York City metropolitan area, particularly in multi-family lending. The bank's focus on rent-regulated buildings has given it a leadership position in this specific segment. The acquisition of Flagstar Bank expanded its reach and product lines.

NYCB reported a net loss of $2.7 billion in the fourth quarter of 2023. This loss was primarily due to a goodwill impairment charge and increased provisions for credit losses. The bank also faced a dividend cut and credit rating downgrades in early 2024.

NYCB's specialization in multi-family lending in the New York City area has been a key advantage. The acquisition of Flagstar Bank provided diversification. Its branch network across several states supports its customer base.

The acquisition of Flagstar Bank in December 2022 was a strategic move to diversify operations. This expanded NYCB's reach into new markets and product lines. The bank's focus is to broaden its customer base.

Impact on Competitive Standing

The recent financial challenges, including the reported net loss and credit rating downgrades, have impacted NYCB's competitive standing. These factors indicate a period of re-adjustment within the banking sector. The bank's ability to navigate these challenges will be crucial.

- Market share analysis reveals a need for strategic adjustments.

- The competitive landscape includes various financial institutions.

- Understanding NYCB's competitive advantages is essential.

- The financial performance of New York Community Bank is under scrutiny.

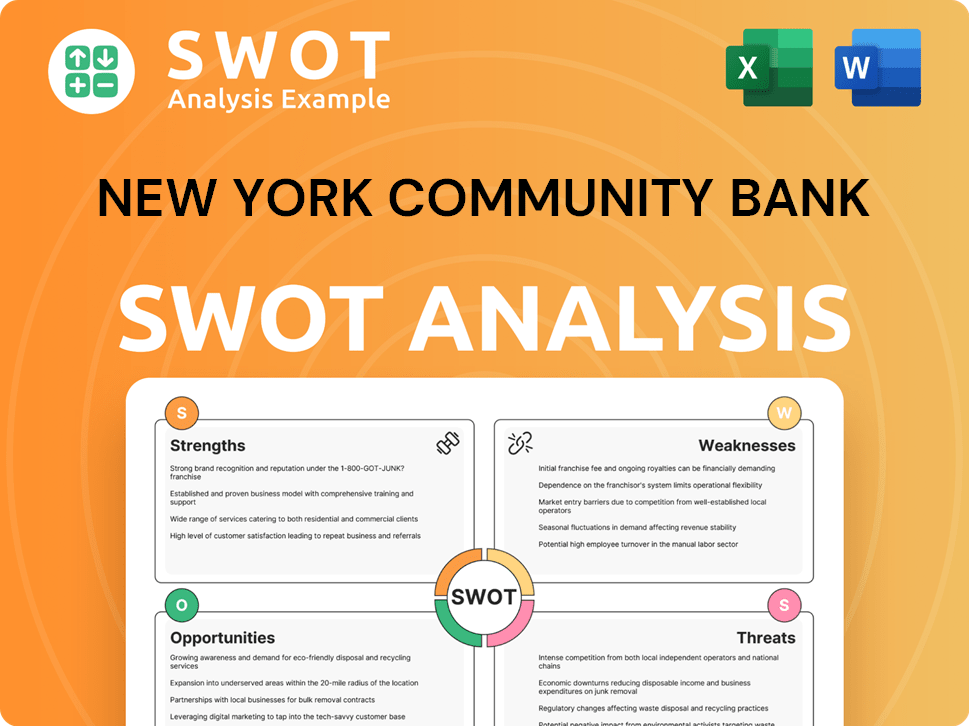

New York Community Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging New York Community Bank?

The competitive landscape for New York Community Bancorp (NYCB) is multifaceted, encompassing a range of financial institutions vying for market share in various segments. The bank faces competition from regional banks, national players, and emerging fintech companies, each employing different strategies to attract customers and maintain profitability. Understanding this competitive environment is crucial for assessing NYCB's strategic positioning and future prospects.

The banking industry's dynamics, including interest rate fluctuations and regulatory changes, further shape the competitive environment. NYCB's performance and strategic decisions are heavily influenced by these external factors, necessitating continuous adaptation and innovation. The following analysis provides insights into the key competitors and the competitive pressures faced by NYCB.

The competitive landscape of New York Community Bank (NYCB) is complex and dynamic, involving a variety of players in the banking industry. NYCB's ability to maintain and grow its market share depends on its capacity to compete effectively against these rivals. The following sections detail the key competitors and the competitive pressures NYCB faces.

Direct Competitors in Lending

Direct competitors include regional banks with a strong presence in the New York metropolitan area, such as Valley National Bank and M&T Bank. These institutions compete directly with NYCB in multi-family and commercial real estate lending. They often compete on loan terms and interest rates.

National Banks

Larger national banks like JPMorgan Chase, Bank of America, and Wells Fargo pose a competitive challenge. These institutions offer a wider range of products and services, backed by extensive branch networks and digital capabilities. They compete with NYCB across broader commercial lending and retail banking services.

Mortgage Lenders

The acquisition of Flagstar Bank has placed NYCB in more direct competition with larger mortgage lenders and servicers. This expansion increases its competition in the mortgage market, requiring NYCB to enhance its mortgage offerings and customer service.

Indirect Competitors

Emerging players and non-bank lenders represent an indirect competitive threat, especially in specialized lending segments. Fintech companies are increasingly offering streamlined digital lending solutions, potentially bypassing traditional banking structures. These companies can offer competitive rates and user-friendly platforms.

Market Dynamics

Mergers and acquisitions within the banking sector can consolidate market power and introduce new competitive dynamics. The challenges faced by regional banks in early 2023, following the failures of Silicon Valley Bank and Signature Bank, intensified competition for deposits and customer trust, impacting NYCB and its peers.

Strategic Considerations

NYCB must continuously adapt its strategies to maintain a competitive edge. This includes optimizing loan terms, enhancing digital capabilities, and managing risks associated with interest rate fluctuations. Understanding the competitive landscape is essential for NYCB's strategic planning and long-term success.

The competitive landscape for NYCB is influenced by various factors, including interest rates, economic conditions, and regulatory changes. For instance, rising interest rates can impact loan demand and profitability. Economic downturns can increase credit risk and affect loan performance. Regulatory changes can alter compliance costs and competitive dynamics. To understand the complete picture, it is essential to consider the broader context of the Brief History of New York Community Bank and its evolution within the banking sector.

Key Competitive Factors

NYCB's competitive position is shaped by several key factors:

- Loan Pricing and Terms: Competitive interest rates and flexible loan terms are crucial for attracting and retaining borrowers.

- Customer Service: Excellent customer service and relationship banking are vital for building loyalty and differentiating NYCB from competitors.

- Digital Capabilities: Investing in digital banking platforms and online services enhances customer convenience and operational efficiency.

- Branch Network: A well-placed branch network provides accessibility and supports customer interactions.

- Risk Management: Effective risk management practices are essential for maintaining financial stability and investor confidence.

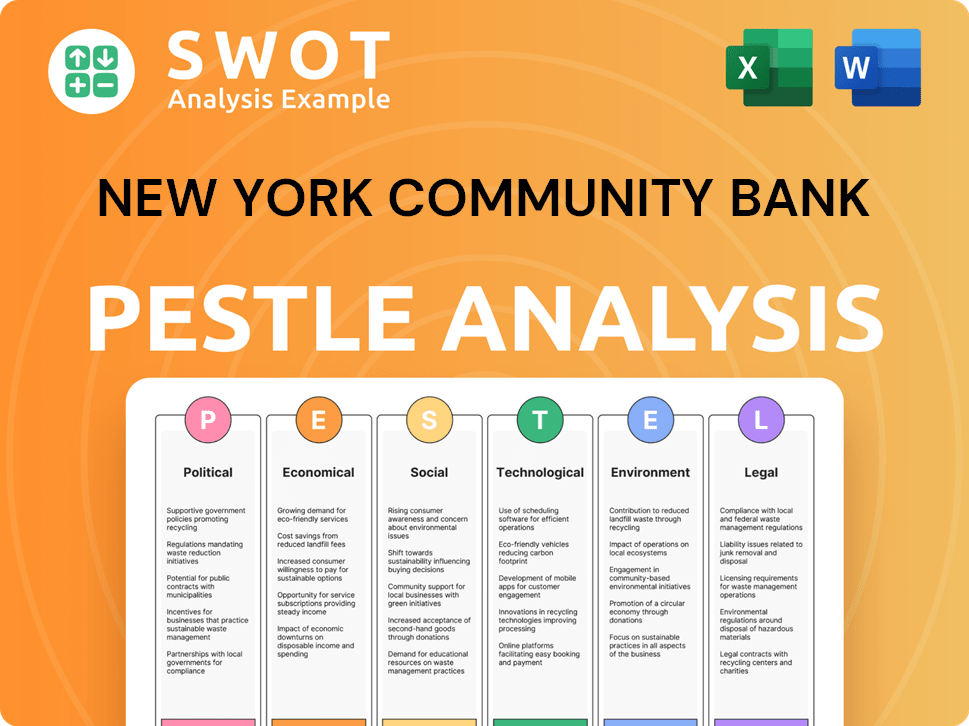

New York Community Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives New York Community Bank a Competitive Edge Over Its Rivals?

The competitive landscape for New York Community Bancorp (NYCB) is shaped by its historical strengths and recent strategic moves. Understanding NYCB's competitive advantages requires a look at its core competencies and how they've evolved. The bank's focus on the New York City multi-family lending market, particularly rent-regulated buildings, has been a cornerstone of its strategy.

A key strategic move was the acquisition of Flagstar Bank in December 2022, which aimed to diversify revenue streams and expand its geographic footprint. This acquisition significantly altered NYCB's competitive position, adding new products and markets. However, the integration has presented challenges, impacting its financial performance in the short term.

The banking industry is constantly evolving, with factors like interest rates, regulatory changes, and market dynamics influencing financial institutions. Analyzing NYCB's competitive advantages involves evaluating its ability to adapt to these changes and maintain its market position. For more information, consider exploring the details of Owners & Shareholders of New York Community Bank.

NYCB's expertise in multi-family lending, especially in rent-regulated buildings, is a significant advantage. This specialization allows for efficient underwriting and risk management. This focus has provided a deep understanding of market dynamics and regulatory nuances.

A well-established branch network in core operating regions fosters strong community ties. This network supports customer loyalty, particularly among retail and small business clients. This presence provides a competitive edge in local markets.

The acquisition of Flagstar Bank aimed to diversify revenue and expand geographic reach. This move added mortgage banking capabilities and a national presence. The integration, however, has presented operational and financial challenges.

NYCB's ability to navigate regulatory changes and market shifts is crucial. Adapting to evolving industry trends is essential for maintaining its competitive edge. The bank's resilience depends on its capacity to manage current financial challenges.

Competitive Advantages in Detail

NYCB's competitive advantages are multifaceted, stemming from its specialization in the multi-family lending market and its expansion through acquisitions. These advantages include deep market knowledge, a strong branch network, and the diversification achieved through the Flagstar acquisition. However, the sustainability of these advantages depends on NYCB's ability to manage risks and adapt to market changes.

- Market Specialization: NYCB's expertise in the New York City multi-family lending market, particularly rent-regulated buildings, allows for efficient underwriting and risk management.

- Branch Network: A well-established branch network fosters strong community ties and customer loyalty, especially among retail and small business clients.

- Acquisition of Flagstar Bank: This acquisition aimed to diversify revenue streams and expand geographic reach, adding mortgage banking and a national presence.

- Adaptability: The bank’s ability to navigate regulatory changes and market shifts is essential for maintaining its competitive edge.

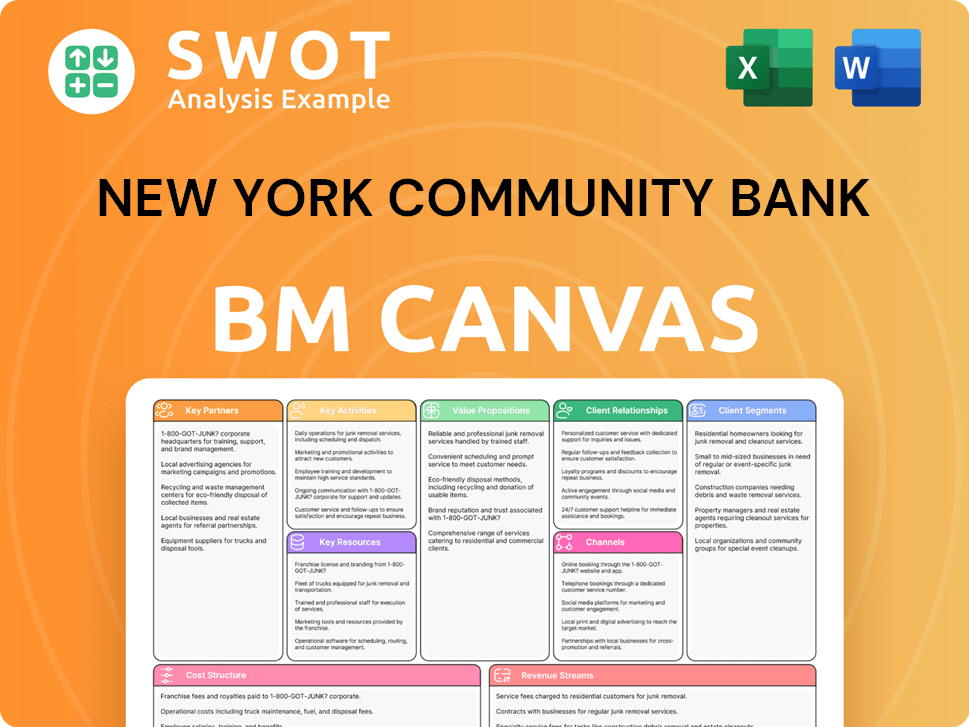

New York Community Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping New York Community Bank’s Competitive Landscape?

The banking industry is experiencing significant changes driven by technological advancements and evolving consumer preferences, creating both challenges and opportunities for New York Community Bancorp (NYCB). The competitive landscape is shaped by digital transformation, regulatory changes, and global economic shifts, impacting loan demand, credit quality, and overall profitability. Understanding these trends is crucial for NYCB to maintain its position and adapt to the evolving market dynamics.

NYCB faces immediate pressures related to asset quality, capital adequacy, and investor confidence, as highlighted by recent financial performance. The bank's ability to integrate Flagstar Bank effectively and address concerns about its commercial real estate portfolio will be vital. Despite these challenges, opportunities exist for NYCB to leverage its expanded presence, capitalize on specialized lending segments, and form strategic partnerships to enhance its digital offerings and customer reach.

Technological advancements are reshaping banking, with increasing demand for digital services and mobile banking. Regulatory changes, particularly those stemming from recent regional banking turmoil, are likely to impose stricter capital requirements. Consumer preferences are shifting towards more convenient, digital-first banking experiences, challenging traditional branch-based models.

NYCB faces challenges including recent financial losses and credit rating downgrades, indicating pressures related to asset quality and investor confidence. Integrating Flagstar Bank effectively and addressing concerns about its commercial real estate portfolio are critical. Global economic shifts, including interest rate fluctuations, can directly impact loan demand and credit quality.

NYCB can capitalize on its expanded presence in mortgage banking through the Flagstar acquisition, leveraging technology to streamline processes. Opportunities exist in specialized lending segments underserved by larger banks. Strategic partnerships with fintech companies could enhance digital offerings and reach new customer segments.

Adapting the business model, strengthening the balance sheet, and strategically deploying resources will be crucial. Focusing on customer experience, investing in digital infrastructure, and managing risks effectively are key. NYCB must navigate the evolving competitive landscape to secure its future position.

Key Considerations for NYCB

NYCB must prioritize strategic initiatives to navigate the evolving financial landscape. The bank needs to enhance its digital offerings, manage its commercial real estate portfolio effectively, and maintain investor confidence. Understanding the competitive landscape is essential for long-term success.

- Focus on Digital Transformation: Invest in technology to enhance digital banking platforms and improve customer experience.

- Manage Risk: Effectively manage the commercial real estate portfolio and address potential credit quality issues.

- Strategic Partnerships: Explore partnerships with fintech companies to expand offerings and reach new customer segments.

- Strengthen Financial Performance: Improve profitability and capital adequacy through strategic initiatives and disciplined execution.

For further insights, explore the Marketing Strategy of New York Community Bank.

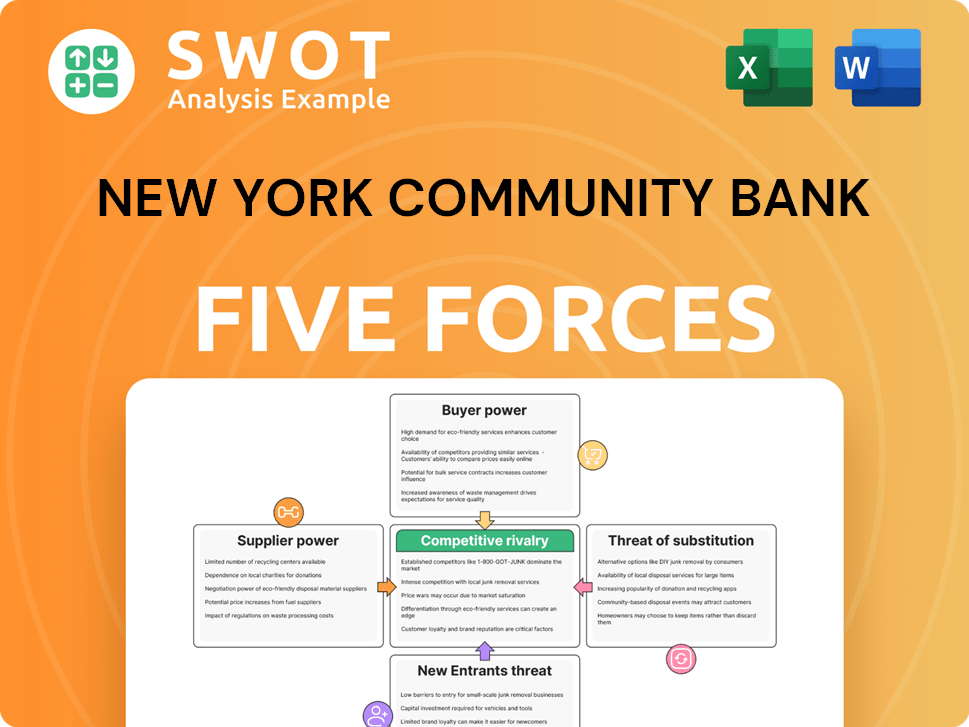

New York Community Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of New York Community Bank Company?

- What is Growth Strategy and Future Prospects of New York Community Bank Company?

- How Does New York Community Bank Company Work?

- What is Sales and Marketing Strategy of New York Community Bank Company?

- What is Brief History of New York Community Bank Company?

- Who Owns New York Community Bank Company?

- What is Customer Demographics and Target Market of New York Community Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.