Dime Community Bank Bundle

How Does Dime Community Bank Stack Up in the NYC Banking Battleground?

Navigating the complex financial world requires a keen understanding of its players. In the bustling New York metropolitan area, Dime Community Bank stands as a notable institution, but how does it fare against its rivals? This analysis dives deep into the Dime Community Bank SWOT Analysis, exploring its competitive strengths, weaknesses, opportunities, and threats within the dynamic banking sector.

This report provides a comprehensive bank analysis, examining Dime Community Bank's market position and its key competitors. We'll explore its financial performance, market share, and strategic initiatives, offering insights into industry trends and the challenges it faces. Understanding Dime Community Bank's competitive landscape is crucial for anyone looking to make informed decisions in the financial world, whether it's assessing its stock price, or understanding its future outlook.

Where Does Dime Community Bank’ Stand in the Current Market?

Dime Community Bank's core operations revolve around providing financial services to individuals, businesses, and organizations, primarily within the New York metropolitan area. Their value proposition centers on relationship-based banking, offering tailored financial solutions and personalized service to a specific customer base. This approach allows them to compete effectively in a market dominated by larger financial institutions. The bank focuses on commercial real estate lending and other commercial and retail banking services.

The bank's market position is strongly influenced by its geographic focus and product offerings. Dime Community Bank strategically concentrates its branch network in the greater New York metropolitan area, particularly in Long Island and New York City. This localized approach allows them to understand and cater to the specific needs of small to medium-sized businesses and local consumers. Their product lines include deposit accounts, commercial and residential real estate loans, commercial and industrial loans, and various retail banking services. The Owners & Shareholders of Dime Community Bank benefit from the bank's consistent performance.

As of late 2023, Dime Community Bancshares, Inc. (DCOM) reported total assets of approximately $13.5 billion. This positions the bank among the larger community banks in the region, though significantly smaller than national and super-regional banks. The bank's financial health, as indicated by its asset size and consistent profitability, generally compares favorably to other community banks of similar scale, often demonstrating strong asset quality and capital ratios.

Specific market share figures for 2024-2025 are subject to ongoing market dynamics and are often reported with a lag. The bank's consistent focus on relationship-based banking and commercial real estate lending has historically cemented its presence. The bank's strategic focus on commercial lending, particularly in multi-family and commercial real estate, reflects a move towards higher-value commercial relationships while maintaining its community banking roots.

Dime Community Bank's financial performance is generally strong compared to other community banks of similar size. The bank typically demonstrates strong asset quality and capital ratios. The bank's financial health, as indicated by its asset size and consistent profitability, generally compares favorably to other community banks of similar scale.

Industry trends in the banking sector include increasing competition from both traditional banks and fintech companies. There is a growing emphasis on digital banking services and customer experience. Community banks like Dime are adapting by investing in technology and focusing on personalized service to maintain their competitive edge.

Dime Community Bank's geographic presence is concentrated in the greater New York metropolitan area. The bank has a strong branch network in Long Island and New York City. This localized focus allows Dime to cater to specific customer segments, including small to medium-sized businesses and local consumers.

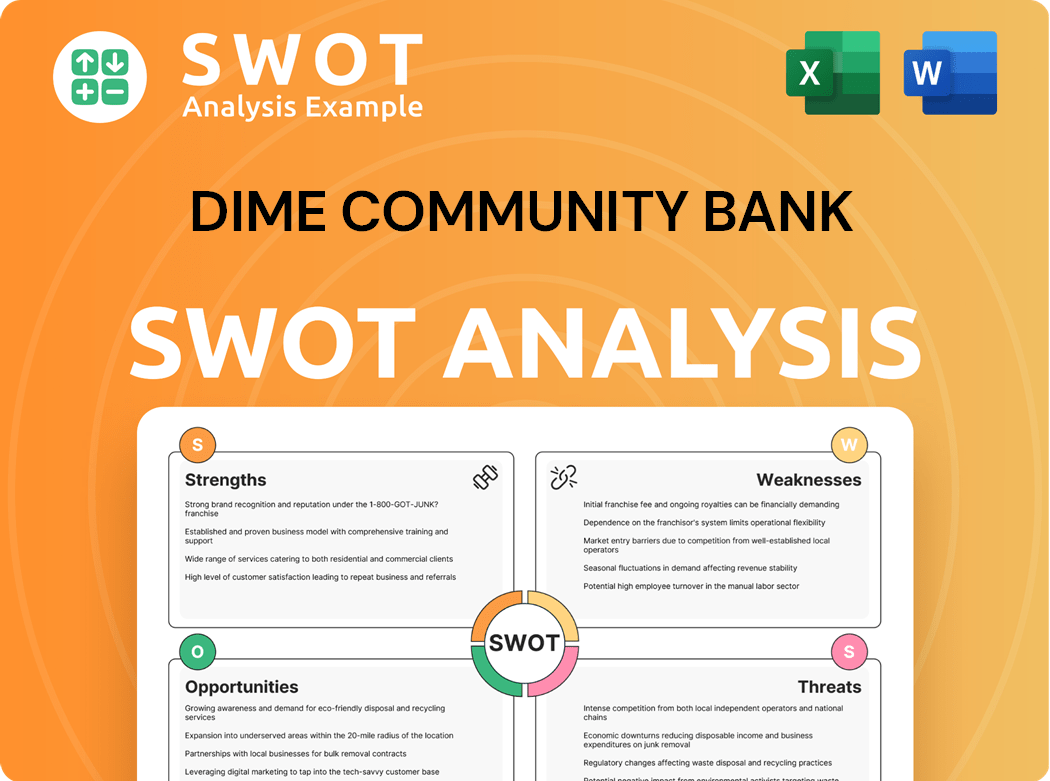

Key Strengths of Dime Community Bank

Dime Community Bank's key strengths include its strong local presence, focus on relationship-based banking, and expertise in commercial real estate lending. The bank's commitment to personalized service and tailored financial solutions helps it to retain customers. The bank's financial performance is generally strong compared to other community banks.

- Strong local presence in the New York metropolitan area.

- Focus on relationship-based banking and personalized service.

- Expertise in commercial real estate lending.

- Consistent financial performance and asset quality.

Dime Community Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging Dime Community Bank?

The Dime Community Bank operates within a complex competitive landscape, facing diverse rivals in the New York metropolitan area. Its strategic positioning and market share are significantly influenced by the actions and performance of its competitors. Understanding the competitive environment is crucial for assessing Dime Community Bank's financial performance and formulating effective strategies.

The Bank Analysis requires a thorough examination of both direct and indirect competitors, including their loan products, interest rates, and service offerings. This analysis is essential for evaluating Dime Community Bank's ability to maintain its market position and adapt to changing industry trends. The competitive dynamics also impact Dime Community Bank's stock price and its overall future outlook.

The competitive landscape for Dime Community Bank includes a range of institutions, from large national banks to smaller community banks and emerging fintech companies. These competitors vie for customers in a market that is influenced by factors such as branch locations, online banking services, and the provision of various financial products. The regulatory environment also plays a crucial role in shaping the competitive dynamics.

Direct Competitors

Direct competitors include regional banks like New York Community Bank (NYCB), Valley National Bank, and Flushing Bank. These banks often offer similar services and target the same customer segments. For example, NYCB, with its focus on multi-family lending, directly competes with Dime for commercial real estate business.

Indirect Competitors

Indirect competition comes from larger national banks such as JPMorgan Chase, Bank of America, and Wells Fargo. These banks have extensive resources and a broad range of products, including investment banking and wealth management. They leverage their scale and technological capabilities to attract customers.

Fintech Competitors

Fintech companies are an emerging competitive threat, especially in digital payments, online lending, and mobile banking. These companies often offer more agile and user-friendly solutions, potentially attracting customers seeking innovative financial services.

Impact of Mergers and Acquisitions

Mergers and acquisitions within the banking sector have led to consolidation, impacting market share and the size of rivals. The integration of acquired entities by larger regional players can shift competitive dynamics, influencing Dime's strategic initiatives.

Customer Base

Understanding the customer base is crucial. Dime serves a diverse customer base, including individuals, small and medium-sized businesses (SMBs), and commercial real estate clients. The bank's ability to retain and attract customers depends on factors like personalized service and competitive offerings.

Strategic Initiatives

Dime Community Bank's strategic initiatives, such as expanding its digital banking capabilities and enhancing its product offerings, are crucial for maintaining a competitive edge. These initiatives are designed to attract and retain customers in a dynamic market.

Analyzing the competitive landscape requires a comprehensive understanding of Dime Community Bank's rivals. This includes assessing their financial performance, market share, and strategic moves. For instance, in 2024, NYCB reported assets of approximately $116.4 billion, highlighting its significant presence in the market. The recent acquisitions and strategic expansions by competitors, such as Valley National Bank, which had assets of around $61.8 billion in 2024, also influence the competitive dynamics. Fintech companies, with their focus on digital solutions, continue to grow, with some, like SoFi, reporting substantial growth in their lending portfolios. To gain a deeper insight into the bank's strategies, consider reading about the Growth Strategy of Dime Community Bank.

Key Competitive Factors

Several factors drive competition in the banking sector, including pricing, service quality, and technological innovation. Dime Community Bank must excel in these areas to remain competitive.

- Interest Rates: Competitive interest rates on loans and deposits are crucial for attracting and retaining customers.

- Service Quality: Providing excellent customer service, including personalized attention and efficient transaction processing, is essential.

- Technology: Investing in digital banking platforms, mobile apps, and online services is vital to meet customer expectations and compete with fintech companies.

- Branch Network: While digital banking is growing, a physical branch network remains important for some customers, especially for those who prefer in-person interactions.

- Product Offerings: Offering a comprehensive suite of financial products, including checking and savings accounts, loans, and investment options, is essential.

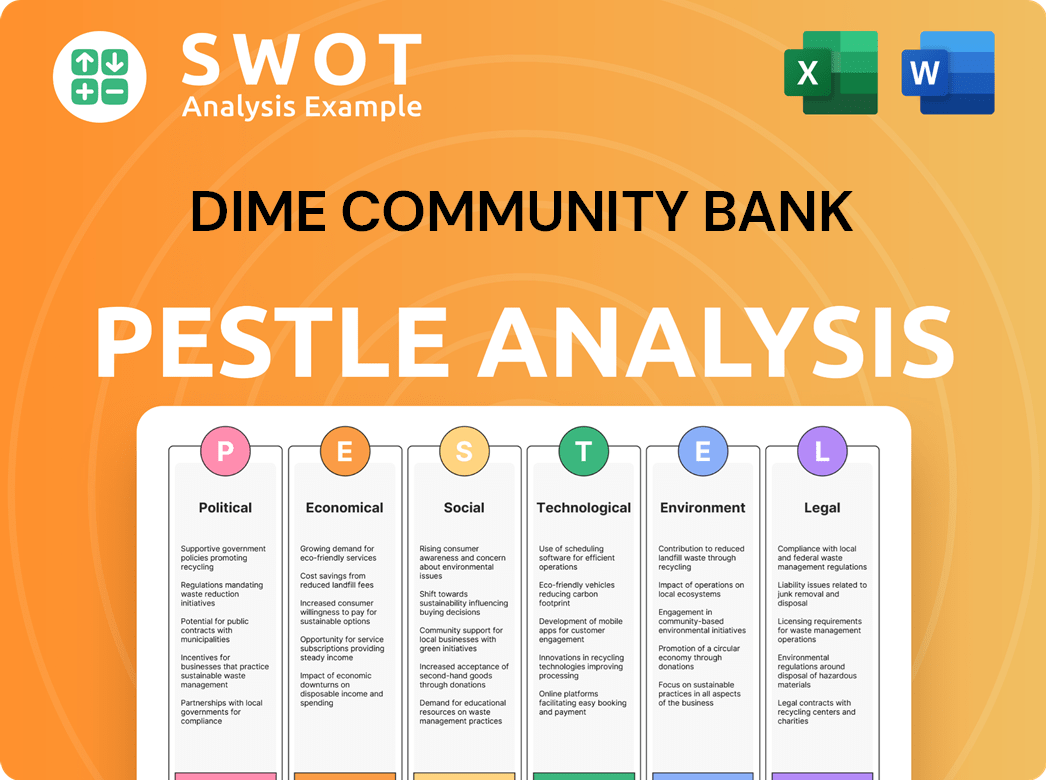

Dime Community Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives Dime Community Bank a Competitive Edge Over Its Rivals?

The competitive advantages of Dime Community Bank are deeply rooted in its community-focused model and long-standing presence in the New York metropolitan area. A key strength is its strong brand equity and reputation, built over 160 years, which fosters deep customer loyalty, especially among local businesses and long-term residents. This longevity provides a profound understanding of local market dynamics, including real estate trends and community preferences. Understanding the Marketing Strategy of Dime Community Bank can give you insight into how they maintain their competitive edge.

Another significant advantage is its relationship-based banking approach. Unlike larger, more transactional institutions, Dime emphasizes personalized service and direct customer relationships. This often results in higher customer retention and greater opportunities for cross-selling products. For instance, its commercial lending teams are known for their expertise in the local real estate market, offering tailored financing solutions. This local expertise also extends to its credit underwriting, allowing for a more nuanced risk assessment within its specific market.

Furthermore, Dime's focus on commercial real estate lending, particularly multi-family properties, provides specialized expertise that differentiates it from more broadly diversified banks. This specialization has allowed it to build a strong portfolio and develop a reputation as a go-to lender in this sector. While not proprietary technology in the traditional sense, its established distribution network of branches in key neighborhoods provides a tangible presence and accessibility that digital-only competitors cannot replicate. These advantages, while not always protected by patents, are sustainable due to the time and effort required to build trust and local market knowledge, though they do face threats from increasing digital adoption and the aggressive expansion of larger banks.

Dime Community Bank benefits from a strong brand reputation built over 160 years. This long-standing presence has cultivated deep customer loyalty, particularly among local businesses and long-term residents. This history allows for a deep understanding of the local market dynamics.

Dime emphasizes personalized service and direct relationships with its customers, unlike larger institutions. This approach leads to higher customer retention rates and increased opportunities for cross-selling. Commercial lending teams possess expertise in the local real estate market.

The bank specializes in commercial real estate lending, particularly multi-family properties. This specialization differentiates it from more broadly diversified banks. Dime has built a strong portfolio and a reputation as a go-to lender in this sector.

Dime maintains a tangible presence through its established branch network in key neighborhoods. This provides accessibility that digital-only competitors cannot replicate. These advantages are sustainable because of the time and effort required to build trust and local market knowledge.

Key Competitive Advantages

Dime Community Bank's competitive advantages are rooted in its community focus and long-standing presence in the New York metropolitan area. These strengths include a strong brand reputation, relationship-based banking, and specialized lending expertise. The bank's established branch network also provides a tangible presence that digital competitors cannot easily match.

- Strong Brand Equity: Over 160 years of building trust and loyalty.

- Relationship-Based Banking: Personalized service leads to higher retention.

- Specialized Lending: Expertise in commercial real estate, especially multi-family properties.

- Established Branch Network: Tangible presence in key neighborhoods.

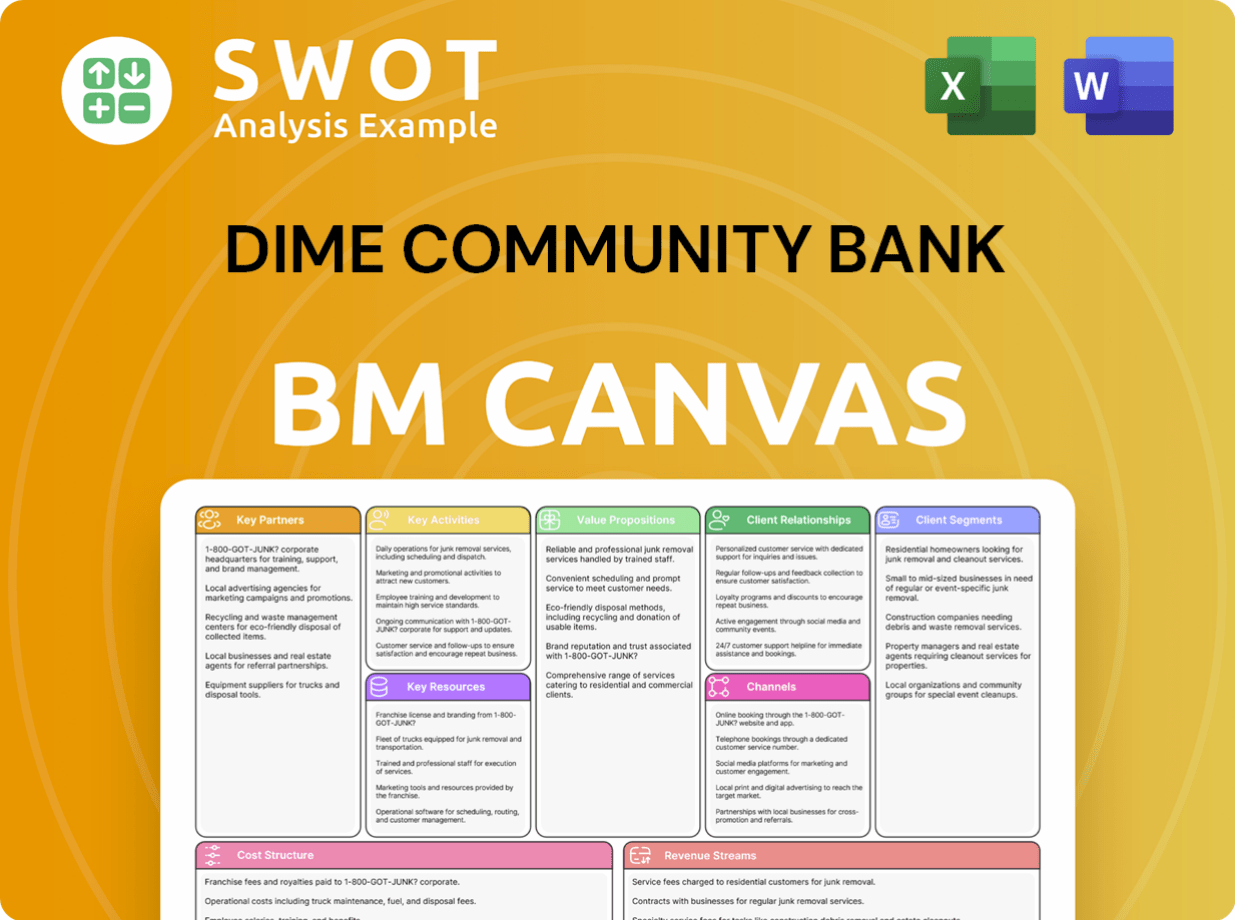

Dime Community Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping Dime Community Bank’s Competitive Landscape?

The banking sector is currently undergoing significant shifts, driven by technological advancements and evolving customer expectations. For a comprehensive Bank Analysis of institutions like Dime Community Bank, understanding these industry trends is crucial for assessing their Competitive Landscape. The ability to adapt to digital transformation while maintaining a strong community focus will be key to future success. For more insight, you can read a Brief History of Dime Community Bank.

Dime Community Bank faces challenges from fintech startups and economic uncertainties, yet it also has opportunities to leverage its local expertise and customer relationships. The bank's strategic initiatives, including digital expansion and potential partnerships, will be critical in navigating the evolving financial landscape. Analyzing its Market Share and Financial Performance in light of these trends will provide a clearer picture of its position and future prospects.

Digital banking and mobile platforms are reshaping customer expectations, requiring significant technology investments. Regulatory changes and evolving compliance requirements impact profitability and operational complexity. The rise of fintech companies is disrupting traditional banking models, intensifying competition.

Keeping pace with rapid digital transformation while preserving a community-focused identity is crucial. Aggressive competition from fintech startups with lower overhead costs poses a threat. Economic uncertainties, such as potential recessions or shifts in real estate markets, could impact loan portfolio quality.

The demand for personalized service and local expertise remains strong, particularly for small businesses. Expanding digital offerings can complement physical presence, reaching a broader customer base. Strategic partnerships with fintech companies can integrate innovative technologies without in-house development.

Focus on enhancing digital capabilities while preserving core community banking values. Explore strategic acquisitions to gain market share and consolidate within the banking sector. Strengthen relationships with local businesses to offer specialized financial solutions.

Key Considerations for Dime Community Bank

Dime Community Bank's ability to adapt to industry changes will be critical for its Future Outlook. Understanding the Competitive Landscape and the impact of Industry Trends is essential. Strategic initiatives, such as digital expansion and potential acquisitions, will shape its Market Position.

- Prioritize investments in digital banking platforms to meet evolving customer expectations.

- Focus on strengthening relationships with local businesses and offering tailored financial solutions.

- Explore strategic partnerships or acquisitions to enhance market share and technology capabilities.

- Monitor the Regulatory Environment and economic conditions for potential impacts on Financial Performance.

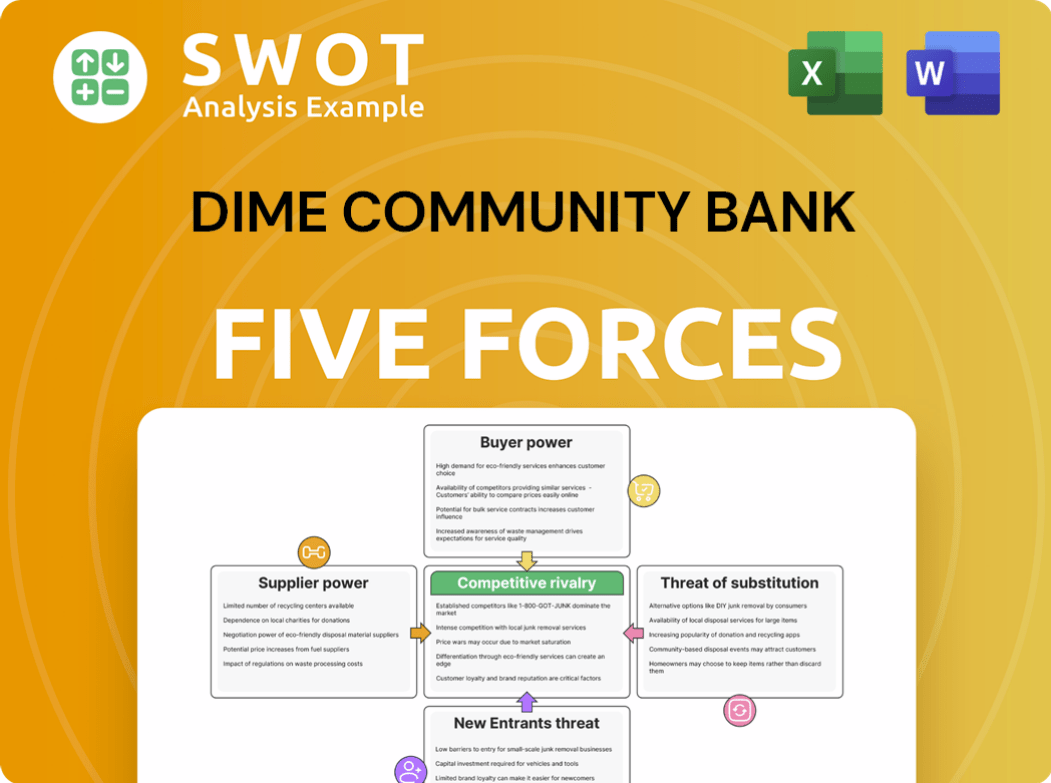

Dime Community Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of Dime Community Bank Company?

- What is Growth Strategy and Future Prospects of Dime Community Bank Company?

- How Does Dime Community Bank Company Work?

- What is Sales and Marketing Strategy of Dime Community Bank Company?

- What is Brief History of Dime Community Bank Company?

- Who Owns Dime Community Bank Company?

- What is Customer Demographics and Target Market of Dime Community Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.