DCB Bank Bundle

How Does DCB Bank Stack Up in India's Banking Arena?

The Indian banking sector is a vibrant ecosystem, and DCB Bank, a prominent player, has a fascinating history. From its roots in the 1930s to its current status as a publicly listed entity, DCB Bank's journey reflects the evolution of the financial services market. With a focus on serving individuals and small businesses, DCB Bank has carved a niche for itself.

To truly understand DCB Bank's position, we must delve into its competitive landscape. This analysis will explore DCB Bank's market share analysis, identify its key rivals, and assess its DCB Bank SWOT Analysis. Examining DCB Bank's financial performance review and competitive advantages is crucial for understanding its growth strategy within the banking industry analysis.

Where Does DCB Bank’ Stand in the Current Market?

DCB Bank operates as a mid-sized private sector bank within the highly competitive Indian banking industry. Its core operations encompass a wide range of financial services, including retail, micro-SME, SME, and mid-corporate banking, along with offerings in agriculture, commodities, and government sectors. The bank serves approximately 2.5 million customers.

The bank's value proposition centers on providing diverse financial solutions to a broad customer base. With a network of 464 branches across 20 states and 2 Union Territories as of March 31, 2025, it focuses on both urban and rural markets. This approach allows DCB Bank to cater to various financial needs, from individual retail customers to small and medium-sized enterprises.

While specific market share figures are marginal in the overall banking sector, DCB Bank strategically positions itself by focusing on specific segments. The bank has a significant presence in rural and semi-urban areas, which constitute about 59% of its total branch network. This targeted approach helps it compete effectively within its chosen niches.

DCB Bank's primary offerings include retail, micro-SME, SME, and mid-corporate banking, along with services for agriculture, commodities, and government sectors. The bank has shifted its focus to more conservative segments like mortgages, MSME, agri, and gold loans. This strategic shift has resulted in a loan book skewed towards retail lending, comprising 89% of the portfolio.

In FY 2025, DCB Bank reported a Profit After Tax (PAT) of INR 615 crore, reflecting a 15% increase from FY 2024. The bank's advances grew by 25% year-on-year, and deposits increased by 22% in FY 2025. The bank's balance sheet size was INR 68,955 crore as of September 30, 2024, representing a growth of 19.49% year-on-year.

As of March 31, 2025, the Gross Non-Performing Assets (NPA) stood at 2.99%, with Net NPA at 1.12%. The bank's Capital Adequacy Ratio was 16.77% as of March 31, 2025, indicating a strong capital position. This robust financial health supports DCB Bank's ability to navigate the competitive landscape.

Key Strategies and Future Outlook

DCB Bank aims to double its balance sheet every three to four years. The bank's strategy focuses on retail lending, with a significant portion secured by self-occupied house property. As of September 30, 2024, mortgages comprised 45% of advances, and Agri & Inclusive Banking (AIB) contributed 25%. This strategic focus is crucial for its future growth.

- Focus on retail lending and specific segments like mortgages and agri loans.

- Expansion of branch network, particularly in rural and semi-urban areas.

- Maintaining strong asset quality and capital adequacy ratios.

- Digital banking initiatives to enhance customer experience and operational efficiency.

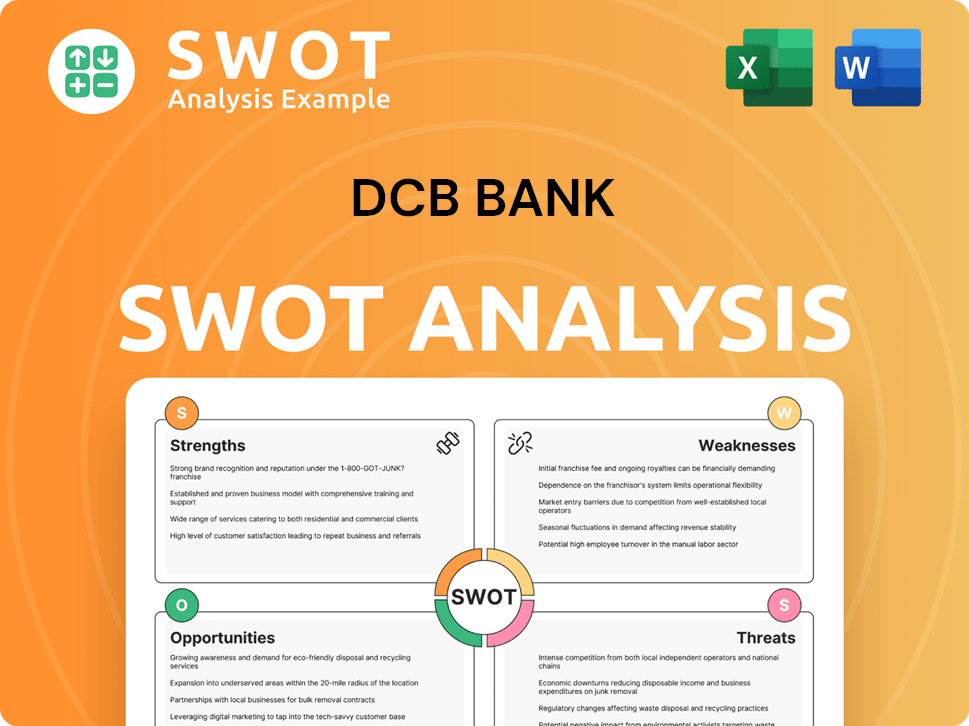

DCB Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

Who Are the Main Competitors Challenging DCB Bank?

The DCB Bank operates within a highly competitive landscape in the Indian private banking sector. This environment is characterized by a diverse array of financial institutions vying for market share and customer loyalty. Understanding the DCB Bank competitors and the broader competitive landscape is crucial for assessing its strategic positioning and future prospects.

The banking industry analysis reveals that DCB Bank faces challenges from both established and emerging players. Competition spans various aspects, including pricing, innovation, branding, distribution, and technology. This necessitates a continuous adaptation of strategies to maintain a competitive edge in the financial services market.

DCB Bank's competitive environment is shaped by a range of factors, including the size and scope of its rivals, their technological capabilities, and their customer base. The bank's performance is influenced by its ability to differentiate itself and effectively compete against these various players.

Key Competitors

The primary competitors of DCB Bank include major private sector banks like Axis Bank, HDFC Bank, ICICI Bank, and Kotak Mahindra Bank. These banks possess extensive branch networks, larger customer bases, and significant technological capabilities, offering a broader range of products and services.

Other Significant Competitors

Other significant competitors include Bandhan Bank, City Union Bank, CSB Bank, Federal Bank, IDFC First Bank, IndusInd Bank, Karnataka Bank, Karur Vysya Bank, RBL Bank, South Indian Bank, Tamilnad Mercantile Bank, and YES Bank. These institutions challenge DCB Bank across different segments and strategic areas.

Competition in Specific Business Lines

In mortgages and loans against property (LAP), DCB Bank competes with numerous banks and housing finance companies. In the Agri & Inclusive Banking segment, it competes with other private and public sector banks, as well as specialized microfinance institutions and NBFCs.

Digital Transformation and Fintech

The increasing focus on digital transformation and fintech collaborations across the Indian banking sector introduces new and emerging players that can disrupt traditional competitive dynamics through innovative digital solutions and customer-centric approaches.

Comparative Benchmarking

City Union Bank is often used as a comparative benchmark in the DCB Bank analysis, providing insights into relative valuation and performance metrics within the sector.

Focus on Inclusive Banking

Bandhan Bank, with its strong focus on inclusive banking, intensifies competition in semi-urban and rural areas, similar to DCB Bank's approach. This creates a direct rivalry in these specific market segments.

Strategic Implications

The competitive landscape necessitates that DCB Bank continuously evaluates its DCB Bank key strategies to maintain and enhance its market position. This includes focusing on innovation, customer service, and operational efficiency. An understanding of the DCB Bank challenges and opportunities is crucial.

- Market Share: DCB Bank's market share analysis must consider the competitive pressures from larger banks and emerging fintech companies.

- Financial Performance: The bank's DCB Bank financial performance review should be benchmarked against its peers to identify areas for improvement.

- Customer Base: Understanding the DCB Bank customer base analysis is essential for tailoring products and services to meet specific needs.

- Digital Initiatives: DCB Bank's digital banking initiatives are critical for staying competitive in the rapidly evolving banking sector.

- Future Outlook: The DCB Bank future outlook depends on its ability to adapt to changing market dynamics and effectively manage its competitive environment.

For further insights into the ownership structure and stakeholders, explore Owners & Shareholders of DCB Bank.

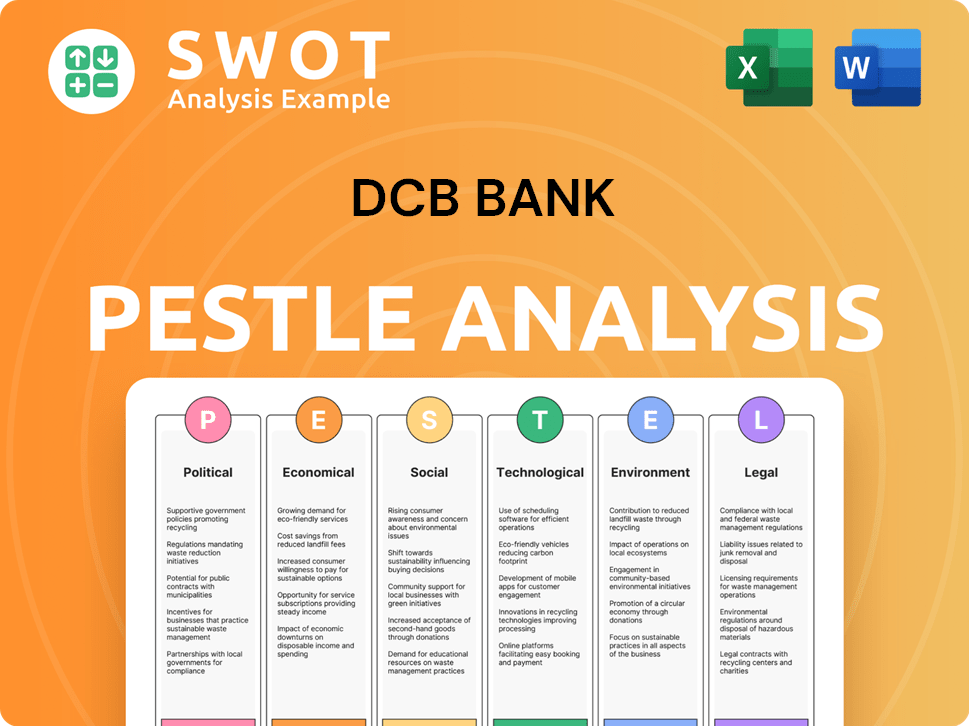

DCB Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What Gives DCB Bank a Competitive Edge Over Its Rivals?

DCB Bank's competitive advantages are rooted in its strategic focus, strong regional presence, and customer-centric approach. The bank has carved out a niche in specific segments, allowing it to build expertise and offer tailored financial solutions. This targeted approach differentiates it from larger competitors and fosters deeper relationships with its customer base.

The bank's commitment to the Agri-Inclusive Banking (AIB) segment is a key differentiator. With a significant number of branches dedicated to AIB, DCB Bank serves underserved rural and semi-urban markets. This focus allows the bank to provide specialized products and services, catering to the unique needs of agricultural and microfinance customers. Furthermore, DCB Bank emphasizes a secured loan portfolio, contributing to its asset quality and risk management.

DCB Bank's ability to adapt its offerings, such as customized loan repayments for agricultural loans, highlights its understanding of its target customers. Coupled with its digital banking initiatives, including a mobile app in multiple regional languages, DCB Bank enhances accessibility and convenience, further solidifying its competitive position. These strategies have enabled DCB Bank to maintain a healthy financial performance within the competitive landscape.

DCB Bank concentrates on specific segments like mortgages, gold loans, MSME, and agri-inclusive banking. This focus allows for specialized expertise and tailored financial products. This strategic approach helps DCB Bank compete effectively in niche markets.

The bank has a significant presence in rural and semi-urban areas, with approximately 59% of its branches in these regions. This deep penetration allows DCB Bank to serve customer segments often underserved by larger banks. This regional focus contributes to its competitive advantage.

DCB Bank offers customized loan repayments for agricultural loans, demonstrating an understanding of its customers' needs. The bank also provides a mobile banking app in nine regional languages. This customer-focused approach enhances accessibility and convenience.

Approximately 94% of DCB Bank's advances book was secured as of September 30, 2024. This focus on secured loans, primarily backed by self-occupied house property, contributes to its asset quality and risk management. This strategy supports its financial stability.

Key Competitive Strengths of DCB Bank

DCB Bank's competitive advantages include a focused business model, strong regional presence, and customer-centric approach. Its Agri-Inclusive Banking (AIB) segment, with 198 branches dedicated to it as of January 2024, is a key differentiator. The bank's emphasis on a secured loan portfolio and digital banking initiatives further strengthens its position within the Marketing Strategy of DCB Bank.

- Focused niche segments: mortgages, gold loans, MSME, and agri-inclusive banking.

- Strong presence in rural and semi-urban areas, serving underserved markets.

- Customer-centric approach with customized loan products and digital banking.

- Emphasis on a secured loan portfolio, contributing to asset quality.

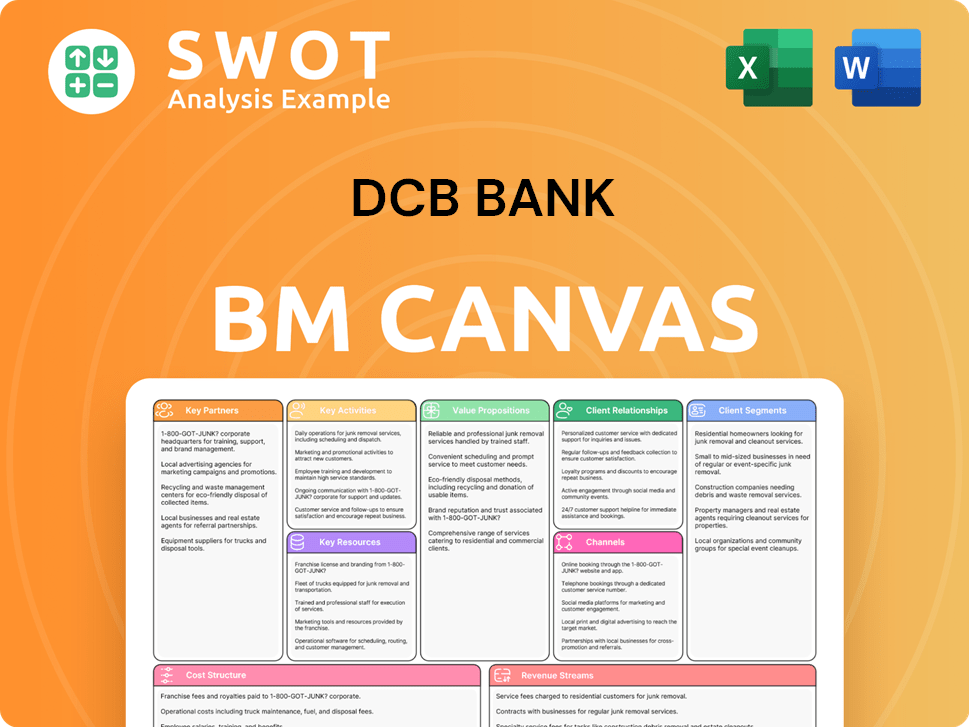

DCB Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What Industry Trends Are Reshaping DCB Bank’s Competitive Landscape?

The Indian banking sector is experiencing rapid transformation, driven by technology and evolving customer expectations. This dynamic environment significantly shapes the competitive landscape for institutions like DCB Bank. The focus on digital innovation, AI, and personalized services is crucial for banks to remain competitive. Keeping up with these trends is vital for DCB Bank to maintain its market position and achieve its growth objectives.

The competitive landscape for DCB Bank is defined by both challenges and opportunities. While the bank faces the need to invest heavily in technology and manage rising costs, it can leverage digital banking and strategic partnerships to expand its reach and enhance customer experiences. The ability to adapt to regulatory changes and focus on niche segments will be critical for future success. Understanding the competitive environment is key for DCB Bank to navigate the changing financial services market.

Key trends include enhanced digitization, the adoption of AI and ML, and a focus on hyper-personalization. Digital banking units (DBUs), open banking, and embedded finance are also emerging. The Indian BFSI sector is expected to invest $15 billion in IT in 2025, highlighting the need for continuous investment in digital infrastructure. GenAI is expected to significantly improve productivity in Indian financial services, with potential gains of up to 46% by 2030.

A major challenge is keeping pace with rapid technological advancements and substantial IT spending by larger banks. Rising costs of funds and the need to strengthen the liability mix also pose challenges. Stress in the microfinance book and potential increases in slippages in the mortgage book require close monitoring. Maintaining Net Interest Margins (NIMs) is another challenge.

Increased adoption of digital banking provides an opportunity to expand reach and improve customer experience. Leveraging AI and data analytics can lead to more personalized services and improved operational efficiency. Strategic partnerships with fintech companies and exploring new business models like Banking-as-a-Service (BaaS) also offer opportunities. Regulatory changes, such as the Banking Laws (Amendment) Bill, 2024, can present opportunities for more efficient operations.

DCB Bank's competitive position will evolve based on its ability to leverage technology for personalized offerings, maintain strong asset quality, and strategically grow its niche segments. The bank aims to double its loan book over the next 3-4 years, implying a 22-23% growth CAGR. The bank's retail-focused, diversified, and secured portfolio is expected to help it navigate economic headwinds and remain resilient.

Key Strategies for DCB Bank

DCB Bank's future success depends on several key strategies. These include leveraging technology for personalized offerings, maintaining strong asset quality, and strategically growing its niche segments. The bank focuses on granular retail loans and enhancing digital capabilities to achieve its growth targets.

- Enhance digital capabilities, including AI-driven solutions for customer service, fraud detection, and risk management.

- Focus on granular retail loans and expand digital reach, especially in rural and semi-urban areas.

- Explore strategic partnerships with fintech companies and new business models like BaaS.

- Improve operational efficiency and cost-to-income ratio.

The Growth Strategy of DCB Bank involves a focus on retail-focused, diversified, and secured portfolios, which is expected to help the bank navigate economic challenges and maintain resilience. The bank's ability to adapt to the evolving financial services market and execute these strategies will determine its long-term success and competitive position. DCB Bank’s performance will be shaped by its ability to leverage technology and maintain a strong asset base.

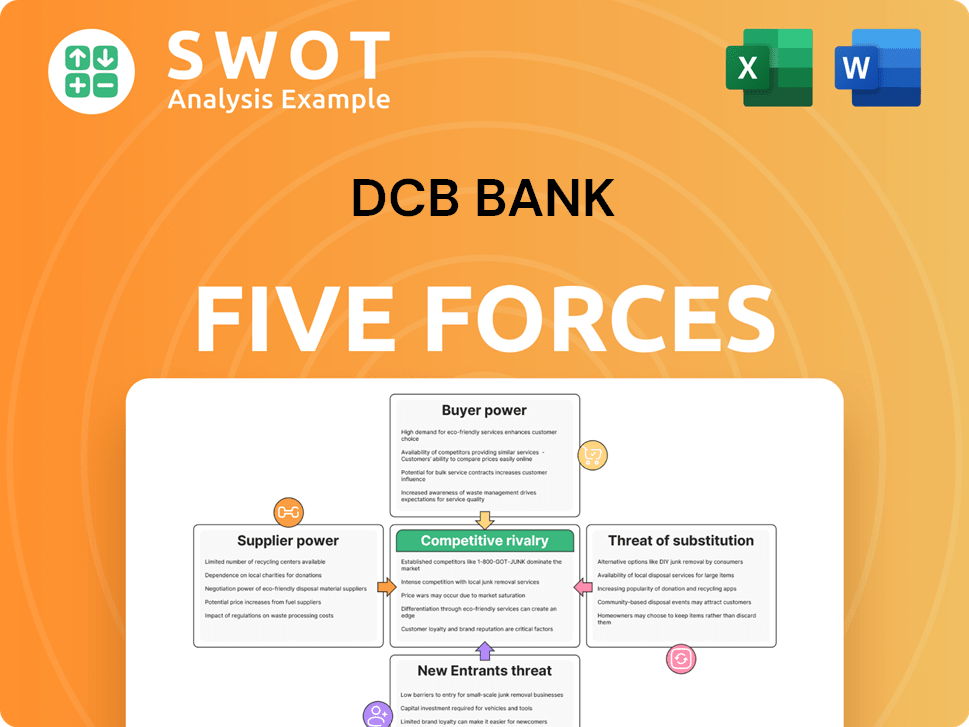

DCB Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What are Mission Vision & Core Values of DCB Bank Company?

- What is Growth Strategy and Future Prospects of DCB Bank Company?

- How Does DCB Bank Company Work?

- What is Sales and Marketing Strategy of DCB Bank Company?

- What is Brief History of DCB Bank Company?

- Who Owns DCB Bank Company?

- What is Customer Demographics and Target Market of DCB Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.