OneMain Holdings Bundle

How Well Do You Know OneMain Holdings?

Journey back in time to uncover the fascinating OneMain Holdings SWOT Analysis and its century-long legacy. From its inception in 1912 as Commercial Credit Company, OneMain Financial has navigated economic shifts, evolving to meet the needs of today's consumers. Discover how this financial services giant has become a leading provider of personal loans.

The story of OneMain Holdings, a key player in the consumer loans market, is a compelling narrative of adaptation and growth. The company's commitment to providing personal loans has shaped its trajectory, from its early days to its current status. Understanding the OneMain history provides valuable insights into the evolution of financial services and the challenges it has overcome.

What is the OneMain Holdings Founding Story?

The story of OneMain Holdings, now known as OneMain Financial, begins with the Commercial Credit Company. Founded on July 1, 1912, in Baltimore, Maryland, by Alexander Duncan, the company's history is deeply rooted in the early 20th-century financial landscape.

Duncan's vision was to address the unmet need for accessible credit. This was particularly true for individuals and businesses who didn't fit the mold of traditional bank lending. This initiative provided a crucial financial resource to a segment of the population that was largely underserved. The company's evolution reflects the changing dynamics of consumer finance.

The company's initial focus was on providing financing for commercial transactions. It acted as a bridge between manufacturers and their customers. The company expanded into direct consumer lending. The first product was likely a form of commercial factoring or loan, enabling the purchase of goods. The name 'Commercial Credit Company' reflected its initial focus on commercial financing. Early funding came from Duncan and his associates, possibly augmented by early investors. The economic context of the early 20th century, characterized by industrial expansion and increasing consumer demand, provided fertile ground for the company's establishment. Businesses and individuals sought credit to fuel growth and consumption, which led to the evolution of OneMain Financial.

Key Takeaways:

The founding of OneMain Financial, then Commercial Credit Company, was in 1912.

- Alexander Duncan established the company in Baltimore, Maryland.

- The primary goal was to provide credit to individuals and businesses.

- The company's initial focus was on commercial financing.

- The economic conditions of the early 20th century supported the company's growth.

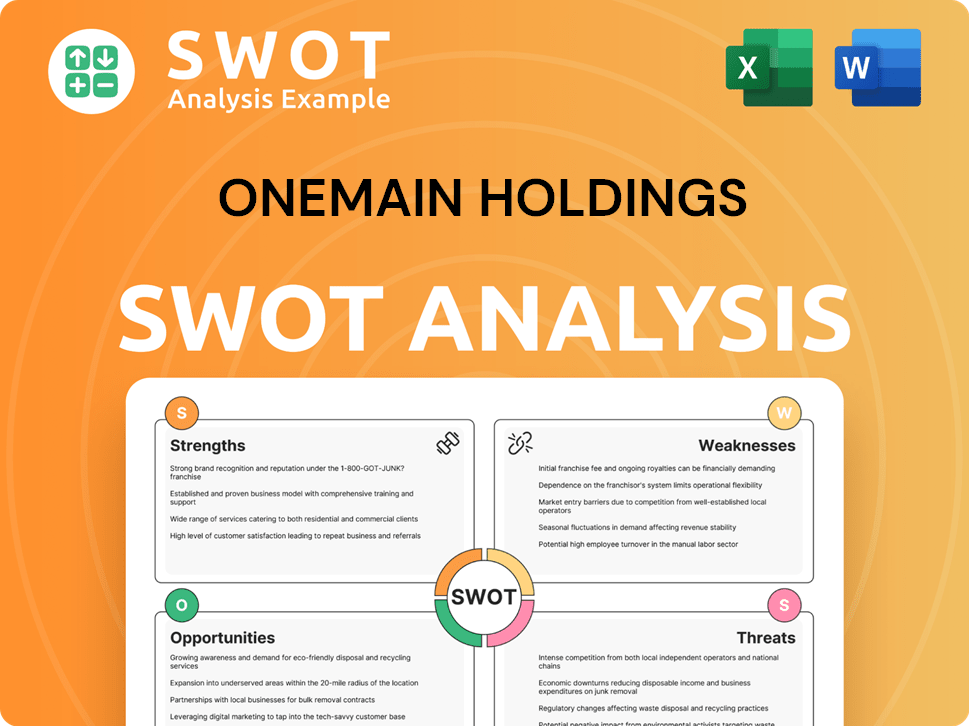

OneMain Holdings SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of OneMain Holdings?

The early growth of Commercial Credit Company set the stage for its future as a major player in the financial services sector. Initially focused on commercial financing, the company expanded its reach by diversifying into consumer lending. This strategic move allowed it to broaden its customer base and product offerings, laying the groundwork for sustained growth.

The company's journey included several significant corporate changes. In 1968, Commercial Credit Company was acquired by Control Data Corporation, integrating it into a larger corporate structure. This acquisition was followed by a spin-off of the financial services arm, marking a shift in its operational focus.

In 1998, the company, then known as Associates First Capital Corporation, was acquired by Citigroup. Under Citigroup, the consumer finance operations underwent rebranding and streamlining. This period set the stage for a pivotal moment in its history.

The year 2011 marked a significant turning point with the divestiture from Citigroup and the rebranding as OneMain Financial. This move signaled a return to its roots as an independent entity, primarily focused on personal loans. This strategic shift allowed OneMain Financial to concentrate on its core business.

The merger with Springleaf Holdings in 2015 led to the formation of OneMain Holdings, Inc. This merger significantly expanded its reach and scale, solidifying its position in the nonprime lending market. The company has continuously adapted its strategies, embracing both a branch-based and online lending model to meet evolving customer preferences and market demands. For insights into how OneMain Holdings approaches its market, consider exploring the Marketing Strategy of OneMain Holdings.

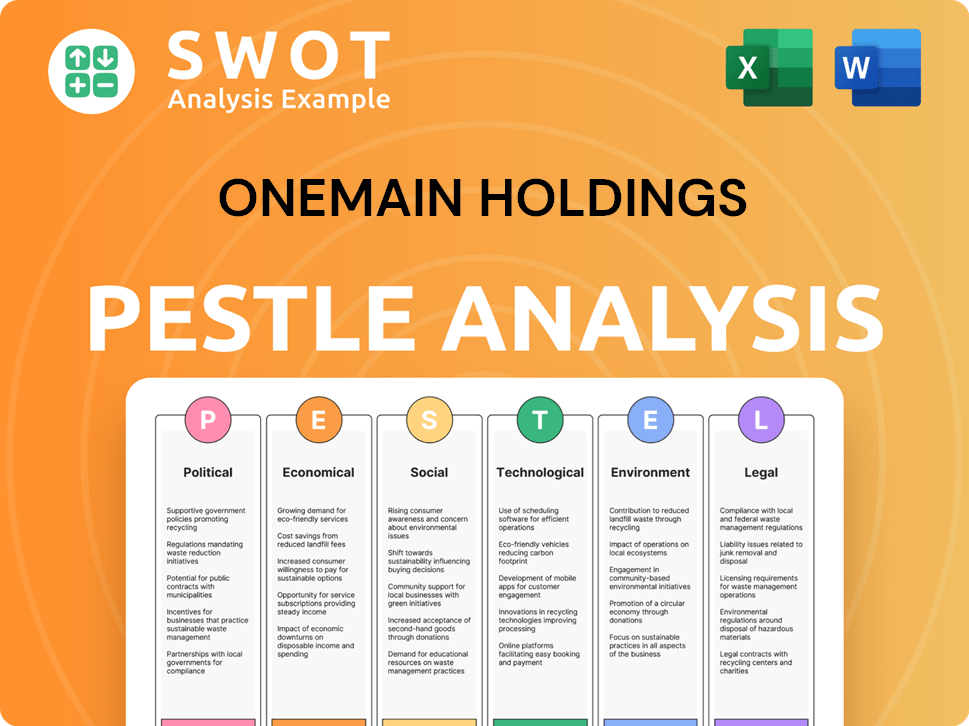

OneMain Holdings PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in OneMain Holdings history?

The history of OneMain Holdings, a prominent player in the financial services sector, is marked by significant milestones. The company's journey includes strategic expansions, mergers, and adaptations to the evolving financial landscape, solidifying its position in the consumer lending market. Understanding the OneMain history provides insights into its growth and operational strategies.

| Year | Milestone |

|---|---|

| 2015 | Merger with Springleaf Holdings, significantly expanding its operational footprint and customer reach. |

| 2019 | Acquisition of the subprime auto lender, Mariner Finance, broadening its financial services offerings. |

| 2024 | Recognized as one of America's Most Responsible Companies by Newsweek, highlighting its commitment to corporate responsibility. |

OneMain Financial has consistently innovated to meet the needs of its customers. A key innovation has been its focus on personalized lending solutions, particularly for nonprime consumers, and it has developed a hybrid operating model combining a branch network with a digital platform.

Personalized Lending Solutions

OneMain Financial specializes in providing personal loans tailored to individual financial situations, particularly for those with less-than-perfect credit histories. This approach allows the company to serve a segment often underserved by traditional banks.

Hybrid Operating Model

The company operates through a combination of physical branches and a digital platform, providing customers with the option to manage their loans online or receive in-person support. This model enhances accessibility and customer service.

Technological Advancements

OneMain Holdings has invested in technology to streamline the loan application process and enhance its digital offerings. These advancements improve efficiency and customer experience.

OneMain Holdings has faced several challenges, including economic downturns and regulatory scrutiny. The company has had to adapt to evolving consumer protection laws and maintain responsible lending practices while ensuring profitability.

Economic Downturns

The 2008 financial crisis and subsequent economic fluctuations have presented challenges for OneMain Financial, impacting loan performance and financial stability. The company has had to navigate periods of increased risk and uncertainty.

Regulatory Scrutiny

Operating in the financial services industry requires compliance with numerous regulations, including those related to consumer protection and responsible lending. OneMain Holdings must continually adapt to new laws and guidelines.

Competitive Landscape

The financial services market is highly competitive, with new fintech companies and traditional lenders vying for market share. OneMain Financial must continually innovate and improve its offerings to stay competitive.

Subprime Lending

OneMain Financial specializes in consumer loans to borrowers with less-than-perfect credit, which inherently involves higher risk. Managing this risk is crucial for the company's financial health.

Strategic Restructuring

The company has undertaken strategic restructuring efforts to adapt to changing market conditions and improve operational efficiency. These actions have included streamlining processes and optimizing resource allocation.

Technological Investments

OneMain Holdings has made significant investments in technology to enhance its digital platforms and improve customer experience. These investments are aimed at staying competitive in the evolving financial landscape.

For further insights into the company's core values and mission, you can explore the mission, vision, and core values of OneMain Holdings.

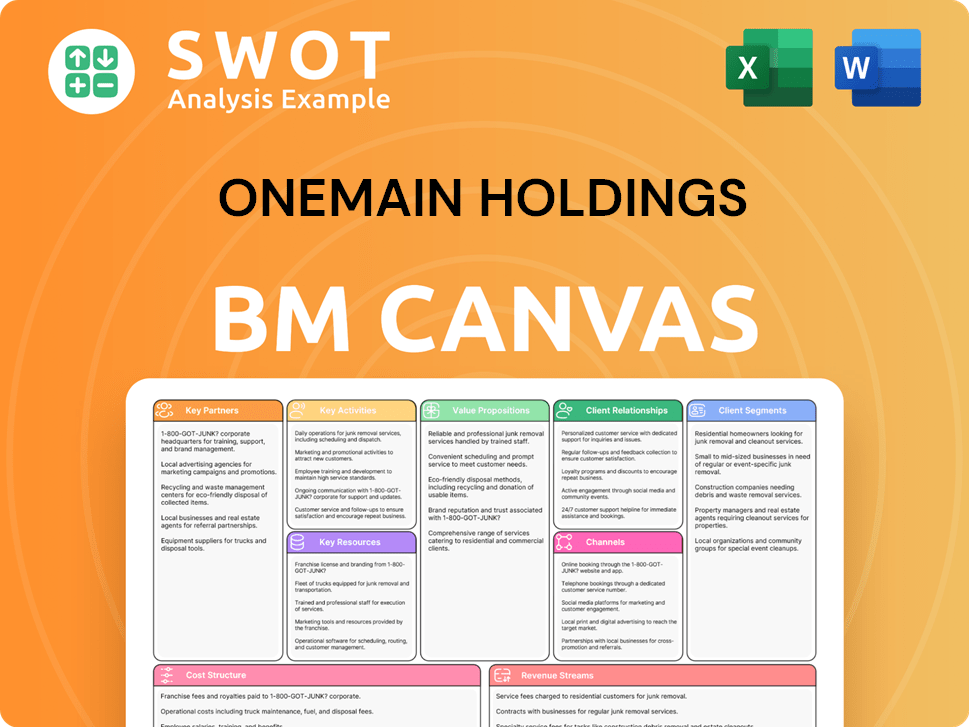

OneMain Holdings Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for OneMain Holdings?

The evolution of OneMain Holdings, formerly known as Commercial Credit Company, reflects a significant journey through the financial services sector. The company's history is marked by strategic acquisitions, divestitures, and a consistent focus on consumer lending. From its inception in 1912 to its current standing, OneMain Holdings has adapted to market changes and economic shifts, solidifying its position in the nonprime lending market. The company's commitment to digital transformation and customer experience has been key to its sustained success, as detailed in Target Market of OneMain Holdings.

| Year | Key Event |

|---|---|

| 1912 | Alexander Duncan founded Commercial Credit Company in Baltimore, Maryland. |

| 1968 | Commercial Credit Company was acquired by Control Data Corporation. |

| 1998 | Associates First Capital Corporation, including the former Commercial Credit Company, was acquired by Citigroup. |

| 2011 | Citigroup divested its consumer finance unit, which was rebranded as OneMain Financial. |

| 2015 | OneMain Financial merged with Springleaf Holdings, becoming OneMain Holdings, Inc. |

| 2020 | OneMain Holdings acquired a portfolio of personal loans from Trim. |

| 2022 | OneMain Holdings partnered with SavvyMoney to provide free credit score and financial insights to its customers. |

| 2023 | The company continued to invest in its digital capabilities, enhancing online loan application and management tools. |

| 2024 | OneMain Holdings was recognized as one of America's Most Responsible Companies by Newsweek. |

| 2025 | OneMain Holdings continues to focus on its strategic initiatives, including expanding its digital presence and enhancing customer experience. |

OneMain Holdings is heavily investing in digital capabilities to improve the customer experience. This includes streamlining the loan application process and enhancing online account management tools. The company leverages data analytics and AI to improve underwriting and personalize financial solutions, creating a more efficient process. This focus on digital transformation is crucial for staying competitive in the financial services sector.

OneMain Holdings is expanding its digital presence and enhancing customer experience. The company is also exploring new product offerings that align with its mission. These initiatives are designed to improve the financial well-being of its customers. The company's focus on responsible lending and its hybrid online-and-branch model positions it well for future growth.

As of the first quarter of 2025, OneMain Holdings reported a net income of $150 million. This demonstrates the company's financial stability and its capacity for future investment. The company's strong financial performance allows it to continue investing in its strategic initiatives. This financial strength supports its continued growth and market position.

OneMain Holdings maintains a prominent role in the nonprime lending sector. The company is committed to providing essential financial services to underserved populations. Its focus on responsible lending and customer service differentiates it from competitors. OneMain Holdings is well-positioned to navigate future economic shifts and competitive pressures.

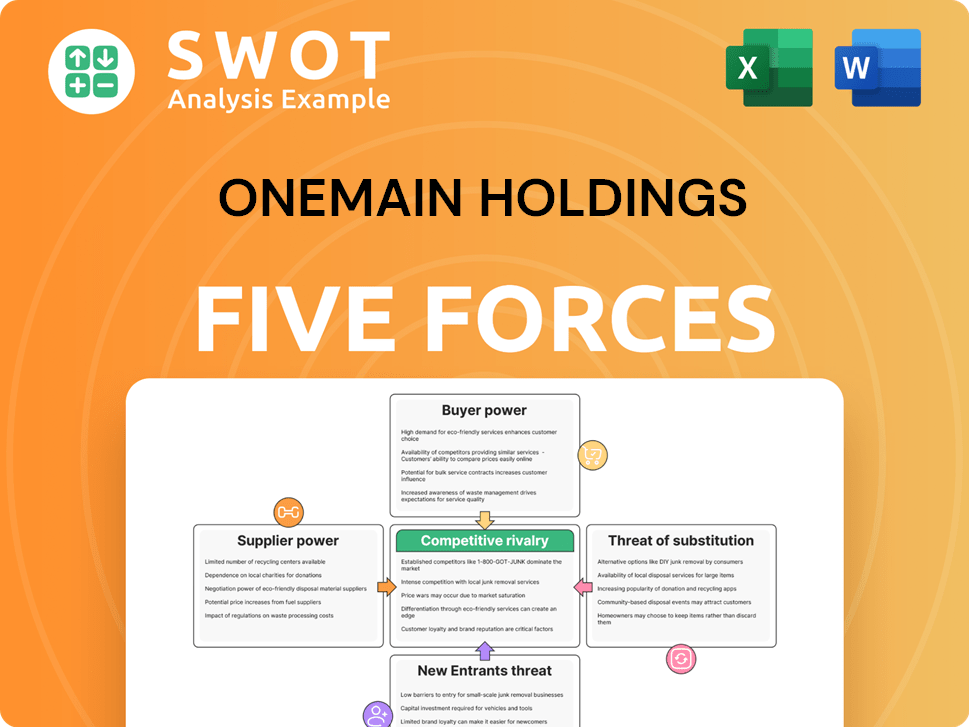

OneMain Holdings Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of OneMain Holdings Company?

- What is Growth Strategy and Future Prospects of OneMain Holdings Company?

- How Does OneMain Holdings Company Work?

- What is Sales and Marketing Strategy of OneMain Holdings Company?

- What is Brief History of OneMain Holdings Company?

- Who Owns OneMain Holdings Company?

- What is Customer Demographics and Target Market of OneMain Holdings Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.