Green Dot Bundle

How Did Green Dot Revolutionize Banking?

Green Dot's story is a compelling journey of innovation in the financial services sector. Starting in 1999, the Green Dot SWOT Analysis reveals a company that has consistently adapted to meet the evolving needs of underserved communities. From its origins as Next Estate Communications to its current status as a leading fintech provider, Green Dot's evolution is a testament to its strategic vision and commitment to financial inclusion.

This exploration into the Green Dot company background will delve into the key milestones and strategic decisions that have shaped its trajectory. Understanding the history of Green Dot prepaid cards offers valuable insights into the broader trends in banking and financial technology. Examining Green Dot's early years and its subsequent growth provides a comprehensive understanding of its impact on the financial landscape.

What is the Green Dot Founding Story?

The story of the Green Dot company begins in 1999, when Steve Streit established Next Estate Communications. The company's initial vision centered on providing a novel payment solution for the emerging digital landscape.

The company's first product, the I-GEN debit card, was introduced in 2000. It was designed to enable online shopping for teenagers and internet users. Streit, who had a background in radio, recognized the need for a payment method that didn't rely on traditional credit cards.

The first I-GEN MasterCard was sold in 2001 at a Rite Aid in Virginia. This marked the beginning of Green Dot's journey in the financial services sector.

Early Years and Pivots

Initially targeting teenagers, the I-GEN card unexpectedly attracted a different demographic.

- The company's 'call center' (a small storage closet) started receiving calls from unbanked or underbanked adults.

- This surprising demand led to a strategic shift in 2001, with Green Dot focusing on serving this adult population.

- By 2003, the I-GEN card was available in over 18,000 stores across the nation.

- In 2004, the company officially rebranded as Green Dot, introducing the first cash-accepting network for reloading debit cards.

In 2007, Green Dot secured its initial funding of $20 million, with Sequoia Capital as an investor. The company's business model addressed a significant need in the market. It offered a practical alternative to traditional banking for millions of Americans who lacked access to conventional financial services. To learn more about the company's core values, you can read Mission, Vision & Core Values of Green Dot.

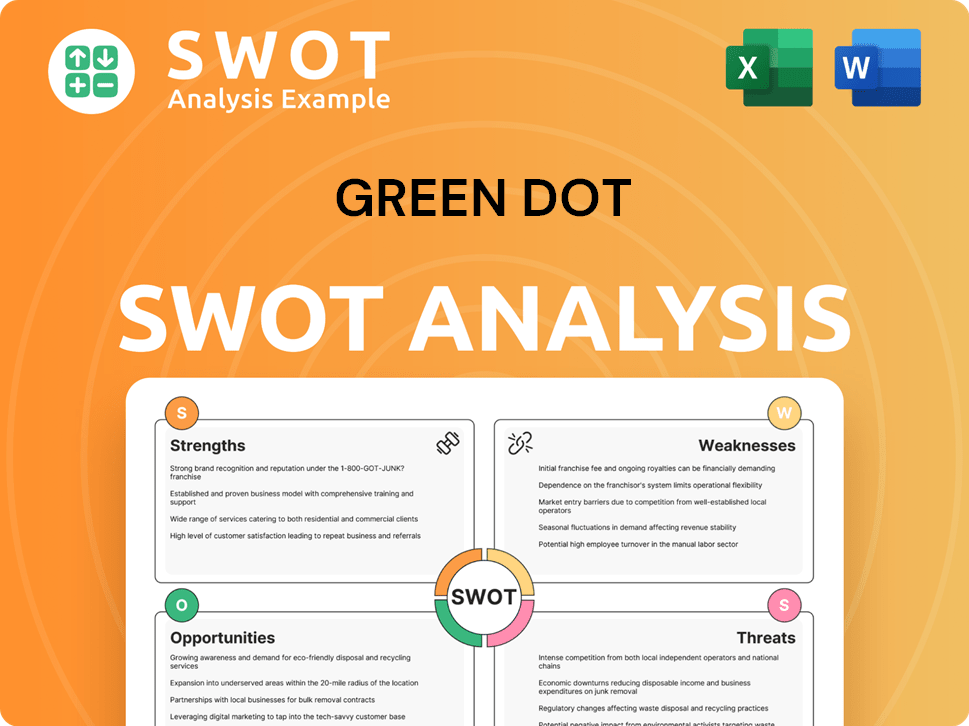

Green Dot SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Green Dot?

The early growth of the Green Dot company was marked by rapid expansion and strategic acquisitions. Initially focused on prepaid debit cards, it quickly broadened its reach through retail partnerships. This expansion set the stage for its evolution into a significant player in the financial services sector.

After the launch of the I-GEN card in 2000,

In 2012,

In 2014,

In 2016, GoBank became the principal payment processor for Uber drivers, solidifying

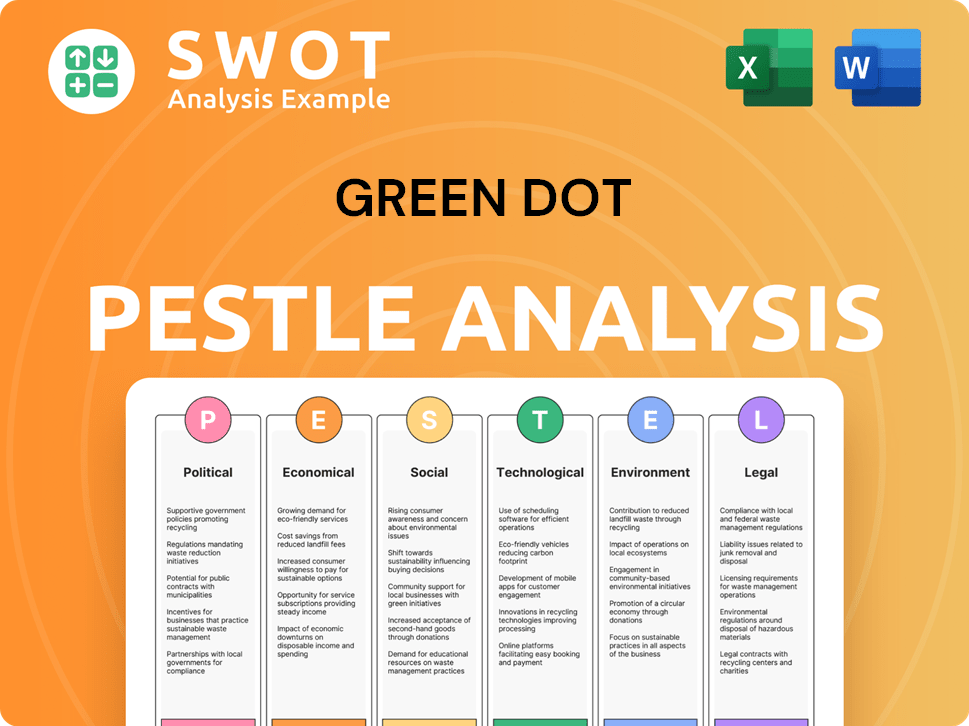

Green Dot PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Green Dot history?

The Green Dot company's journey has been marked by significant milestones and strategic shifts. It has evolved from a prepaid card provider to a financial technology platform, adapting to the changing landscape of financial services.

| Year | Milestone |

|---|---|

| 2012 | Acquired Loopt, a location-based social networking service, to enhance mobile capabilities. |

| 2013 | Launched GoBank, a mobile-first bank account, marking a significant move into digital banking. |

| 2014 | Partnered with Walmart to offer checking accounts, expanding its reach to a wider customer base. |

| 2016 | Collaborated with Uber for driver payments, integrating its services into the gig economy. |

| 2017 | Began powering Apple's Apple Pay Cash service, broadening its presence in digital payments. |

| 2025 | Announced new partnerships with Samsung Wallet and Crypto.com, enhancing embedded finance offerings. |

| March 2025 | Green Dot Bank received an 'Outstanding' Community Reinvestment Act (CRA) rating from the Federal Reserve. |

Green Dot has consistently innovated to stay ahead in the competitive financial services market. Its early move into mobile banking with GoBank was a pivotal step, and its partnerships with major companies like Walmart and Uber demonstrated its ability to integrate its services into large consumer ecosystems.

Mobile Banking

The launch of GoBank in 2013, a mobile-first bank account, was a key innovation. This initiative positioned Green Dot as a pioneer in digital banking, catering to the growing demand for mobile financial solutions.

Strategic Partnerships

Forming partnerships with major retailers and service providers, such as Walmart and Uber, expanded Green Dot's reach. These collaborations allowed Green Dot to integrate its services into established consumer platforms, increasing accessibility.

Embedded Finance

Recent partnerships with Samsung Wallet and Crypto.com reflect Green Dot's focus on embedded finance. This strategy allows Green Dot to offer its financial products and services within the platforms of other companies, enhancing user experience.

Community Reinvestment

The 'Outstanding' CRA rating from the Federal Reserve highlights Green Dot's commitment to community development. This recognition shows its dedication to serving the financial needs of underserved communities.

Technological Advancements

Green Dot has consistently adopted new technologies to improve its services. This includes leveraging mobile platforms and digital payment systems to enhance user convenience and security.

Product Diversification

Expanding beyond prepaid debit cards, Green Dot has diversified its offerings. This includes providing banking services and embedded finance solutions to meet various consumer and business needs.

Green Dot has faced challenges, including intense competition in the financial services market. The decline in the legacy prepaid debit card business and stock performance volatility have also posed difficulties.

Competition

Green Dot operates in a highly competitive market, facing rivals from traditional banks and fintech companies. This competition puts pressure on pricing and the need for continuous innovation.

Prepaid Card Decline

The shift in consumer preferences away from prepaid debit cards has impacted Green Dot's revenue. This decline necessitates strategic adjustments to focus on growing segments like embedded finance.

Financial Performance

Green Dot has experienced fluctuations in its financial performance, including periods of losses. The company has worked to improve its profitability and meet financial expectations.

Stock Volatility

Green Dot's stock has shown volatility, reflecting the challenges and uncertainties in the financial services sector. Addressing these issues is crucial for enhancing shareholder value.

Strategic Execution

Successfully navigating the competitive landscape requires effective strategic execution. The company has undertaken strategic pivots and leadership changes to adapt to market dynamics and improve its performance.

Regulatory Compliance

The financial services industry is heavily regulated, and Green Dot must comply with various regulations. This necessitates ongoing efforts to meet compliance standards and manage related costs.

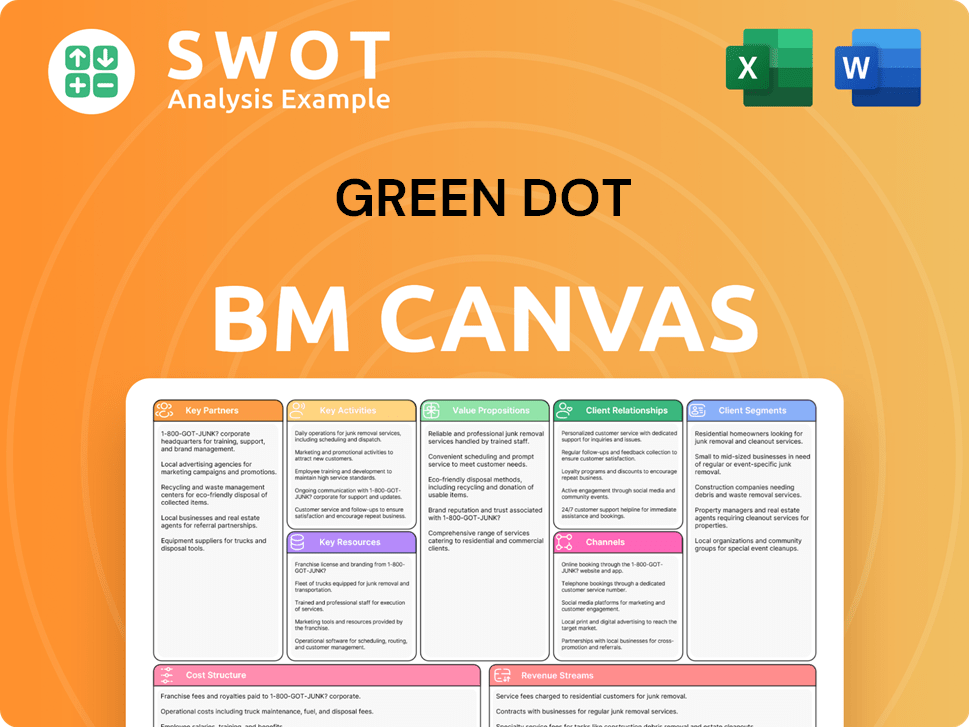

Green Dot Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Green Dot?

The Owners & Shareholders of Green Dot have witnessed a remarkable journey. From its inception as Next Estate Communications in 1999, the company, later known as Green Dot, has transformed the financial services landscape. Initially focused on prepaid debit cards for teenagers and internet users, it pivoted to serving the 'unbanked' and 'underbanked' populations. This strategic shift and subsequent innovations have shaped its history.

| Year | Key Event |

|---|---|

| 1999 | Steve Streit founded Green Dot Corporation, originally named Next Estate Communications. |

| 2000 | The company launched its first debit card, I-GEN, targeting teenagers and internet users. |

| 2001 | The first I-GEN MasterCard was sold, and the company shifted its focus to the 'unbanked' and 'underbanked'. |

| 2004 | I-GEN officially became Green Dot and launched a cash-accepting network for reloading debit cards. |

| 2010 | Green Dot Corporation went public on the New York Stock Exchange (NYSE: GDOT) with a valuation of $2 billion. |

| 2012 | The company acquired mobile location technology company Loopt for $43.4 million. |

| 2013 | Green Dot developed and launched GoBank, a mobile-first bank account. |

| 2014 | The company partnered with Walmart to offer checking accounts and acquired Santa Barbara Tax Products Group. |

| 2015 | Green Dot acquired AccountNow Inc. and AchieveCard. |

| 2016 | GoBank became the principal payment processor for Uber drivers. |

| 2017 | Green Dot acquired UniRush LLC for approximately $147 million and powered Apple Pay Cash P2P payment service. |

| 2021 | The company relocated its headquarters from Pasadena, California, to Austin, Texas. |

| January 1, 2025 | Green Dot relocated its headquarters to Provo, Utah. |

| February 27, 2025 | The company reported Fourth Quarter 2024 results, showcasing active account growth and expansion in embedded finance. |

| March 10, 2025 | Green Dot announced a review of strategic alternatives and a leadership transition, with William Jacobs as interim CEO. |

| May 6, 2025 | The company announced a partnership with Samsung to introduce new Samsung Wallet features, powered by Green Dot's Arc platform. |

| May 8, 2025 | Green Dot reported strong First Quarter 2025 results, including non-GAAP revenue up 24% year-over-year to $556.0 million and adjusted EBITDA up 53% to $90.6 million. |

Green Dot anticipates continued growth, particularly in its embedded finance and money movement services. The company is focused on strategic marketing for GO2bank and expanding its account programs.

The company projects non-GAAP revenue between $2.0 billion and $2.1 billion. Adjusted EBITDA is expected to range from $150 million to $160 million, and non-GAAP EPS is projected between $1.14 and $1.28.

Green Dot's B2B segment is expected to show strong growth in the low to mid-30% range for 2025. The Money Movement segment is projected to grow in the low single digits.

The company's ongoing review of strategic alternatives suggests potential future developments. Green Dot aims to maximize shareholder value and maintain its position in the embedded finance market.

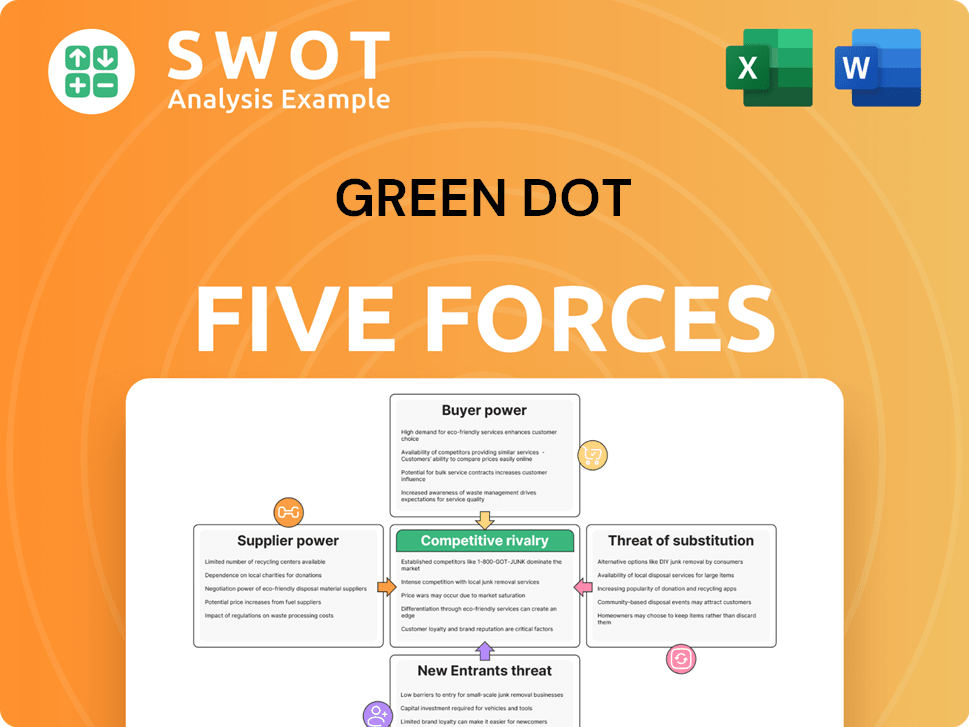

Green Dot Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Green Dot Company?

- What is Growth Strategy and Future Prospects of Green Dot Company?

- How Does Green Dot Company Work?

- What is Sales and Marketing Strategy of Green Dot Company?

- What is Brief History of Green Dot Company?

- Who Owns Green Dot Company?

- What is Customer Demographics and Target Market of Green Dot Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.