Glacier Bank Bundle

How Did Glacier Bank Rise to Regional Banking Prominence?

From its modest roots in Kalispell, Montana, Glacier Bank has evolved into a financial powerhouse. Founded in 1955 as First Federal Savings and Loan, the bank's journey reflects a remarkable transformation. This evolution highlights a strategic blend of community focus and ambitious expansion within the competitive banking industry.

Glacier Bank's story is one of consistent growth, marked by strategic bank acquisitions and a commitment to its "super community banking" model. As of March 31, 2025, the bank boasts 227 locations across eight Western states, a testament to its successful expansion. Understanding the Glacier Bank SWOT Analysis provides further insights into its strategic positioning and future prospects within the Montana banks and broader banking industry landscape.

What is the Glacier Bank Founding Story?

The story of Glacier Bank, now a significant player in the banking industry, began in 1955. It started as First Federal Savings and Loan in Kalispell, Montana. This founding marked the inception of what would become a prominent regional bank.

The initial vision was driven by local businessmen. They saw a need for financial services within their community. This early focus on community needs has remained a key aspect of the bank's operations.

The bank's formation involved a group of local businessmen. Alton Pierce, Owen Sowerwein, Milt Mercord, and Ruben Nordem were key figures. They identified an opportunity to serve the financial needs of their community. The initial capital of $172,000 was raised from 127 Flathead citizens, with a charter costing $150,000. Bob Gattis was the first managing officer.

Early Days and Community Focus

First Federal Savings and Loan focused on deposit accounts and real estate lending. This model was common in the mid-20th century, supporting local economies.

- The bank's early funding came from the local community.

- This community-driven approach highlighted the bank's local roots.

- The commitment to local service continues to be a core value.

- The bank's history reflects its deep ties to the community.

The early business model centered on deposit accounts and real estate lending. This approach was typical of savings and loan associations during that era. These institutions played a crucial role in local economies. They facilitated homeownership and savings for individuals.

A notable aspect of its early days was the community-driven funding. This showcased the strong local support and the bank's initial vision. This commitment to local service remains a fundamental part of Glacier Bank's operations today. To learn more about the values that drive the bank, check out the Mission, Vision & Core Values of Glacier Bank.

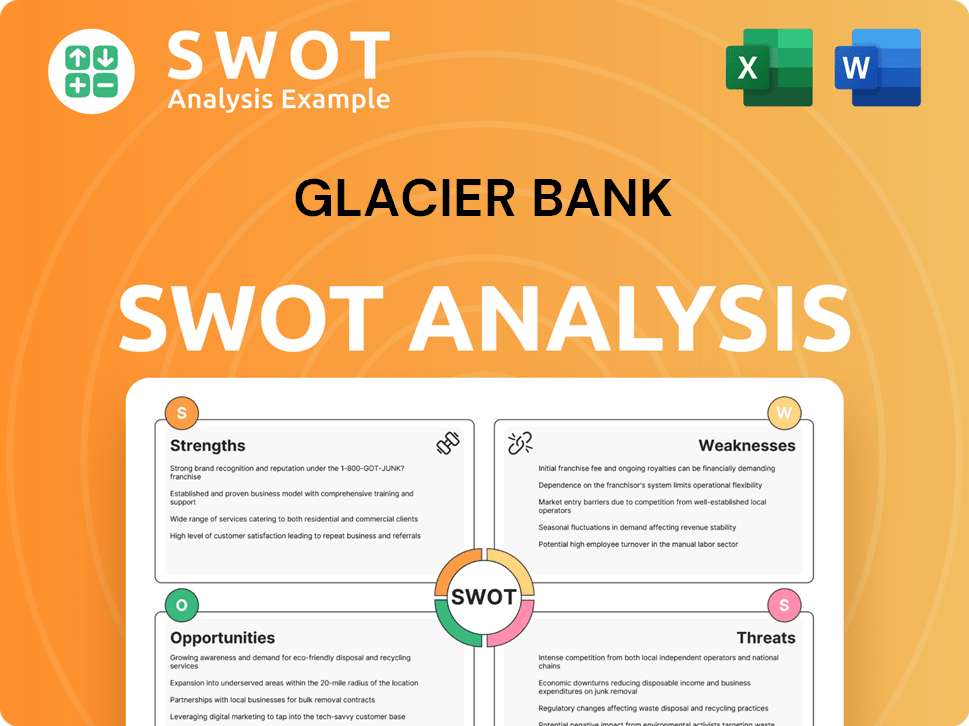

Glacier Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Glacier Bank?

The early years of Glacier Bank, formerly known as First Federal Savings Bank of Montana, were characterized by strategic expansion and pivotal acquisitions. This period saw the company evolve from a local savings and loan into a multi-bank holding company, significantly increasing its assets and geographical footprint. Key decisions and acquisitions laid the foundation for its growth within the

In 1977, Charles Mercord took over as managing officer and chief executive of the bank. A critical step occurred in 1984 when First Federal Savings and Loan of Kalispell went public as First Federal Savings Bank of Montana. This move provided crucial capital for future

The acquisition of Glacier National Bank of Columbia Falls in 1989 was a significant move, boosting First Federal's assets to over $165 million. This led to the renaming of the bank to First Federal Savings Bank of Montana, reflecting its broader scope. This was one of the first instances of a thrift acquiring a bank in the U.S.

In 1990, Glacier Bancorp Inc. was established as the parent company, and in 1992, First Federal was officially renamed Glacier Bank. The acquisition of Evergreen Bancorp in 1992 added $46.2 million in assets. By 1997, Glacier's assets had grown to over $580 million, with loans increasing by nine percent.

The company expanded its footprint by acquiring Missoula Bancshares, Inc. in 1996 and HUB Financial Corporation in 1998. The 1999 acquisition of Mountain West Bank of Idaho marked its entry into Idaho. By 1999, the loan portfolio showed a shift, with commercial loans at 42%, real estate at 36%, and consumer loans at 22%, indicating a more balanced approach.

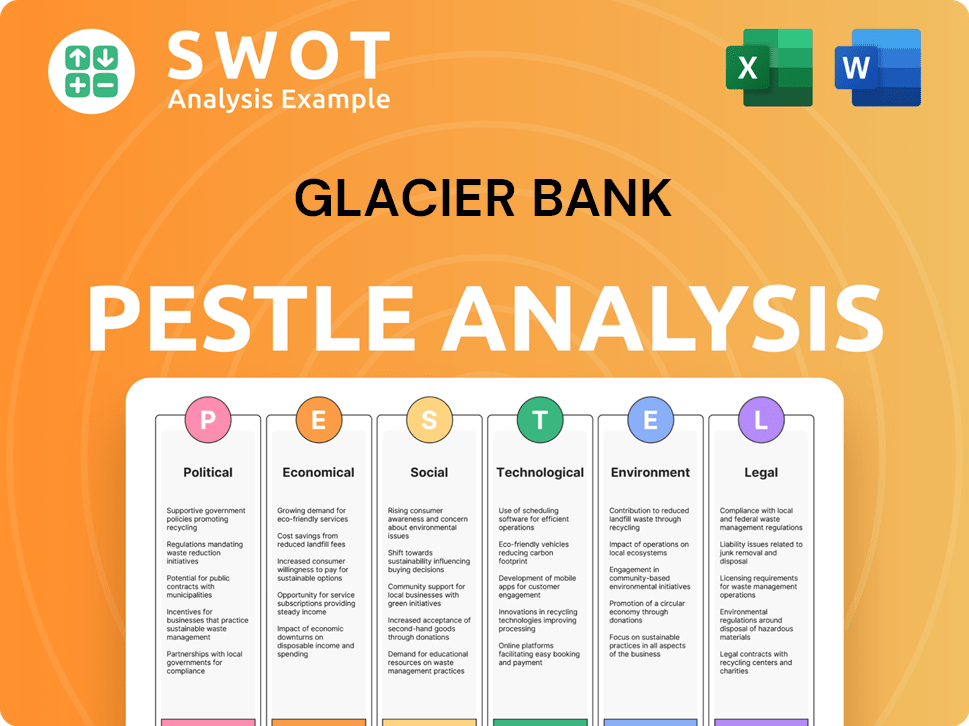

Glacier Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Glacier Bank history?

The Glacier Bank history is marked by significant growth and strategic decisions within the banking industry. The company has consistently expanded its footprint through bank acquisitions and maintained a strong commitment to its community banking model. This approach has allowed it to navigate market changes and maintain a strong financial position.

| Year | Milestone |

|---|---|

| 2000 | Glacier Bancorp began a series of strategic acquisitions to expand its presence across the Western United States. |

| 2012 | Consolidated its eleven commercial banks into a single, larger bank to streamline operations. |

| 2014 | Partnered with EVERFI to provide online financial literacy programs to K-12 schools, small businesses, and adults. |

| 2025 | Completed its 26th bank acquisition since 2000 with the Bank of Idaho Holding Co. deal closing on April 30, 2025. |

| Q1 2025 | Declared its 160th consecutive quarterly dividend. |

A key innovation for Glacier Bank has been its 'super community banking' model, which allows individual bank divisions to maintain local brand names and management teams. This approach fosters local market knowledge and community engagement while leveraging the resources of the larger Glacier Bancorp. This strategy has supported the company's growth and its ability to adapt to local market needs.

'Super Community Banking' Model

This model allows individual bank divisions to maintain local brand names and management teams, fostering community engagement. It also benefits from the resources of the larger Glacier Bancorp, supporting growth and adaptability.

Strategic Acquisitions

Glacier Bank has a consistent track record of strategic acquisitions, expanding its footprint across the Western United States. These acquisitions have been a key driver of its growth and market presence.

Financial Literacy Programs

Partnerships with organizations like EVERFI to provide online financial literacy programs to K-12 schools, small businesses, and adults. This demonstrates a commitment to community development beyond traditional banking services.

Despite its growth, Glacier Bank has faced challenges, including integrating acquired entities and maintaining consistent service quality across its expanding regions. Some customer feedback has highlighted issues with mobile app functionality and call center efficiency. The company has also had to navigate economic uncertainties and interest rate changes. For more details on the Glacier Bank history, you can explore Revenue Streams & Business Model of Glacier Bank.

Integration Challenges

Integrating acquired entities and maintaining consistent service quality across expanding regions has presented challenges. Addressing these issues is crucial for ensuring customer satisfaction and operational efficiency.

Economic Uncertainties

Navigating economic uncertainties, including interest rate changes and inflationary pressures, has been a constant challenge. Glacier Bancorp focuses on operational efficiencies, such as managing costs and improving its net interest margin, which increased to 3.04% in Q1 2025.

Customer Service Issues

Customer feedback has highlighted issues with mobile app functionality and call center efficiency. Addressing these concerns is important for maintaining customer loyalty and improving the overall banking experience.

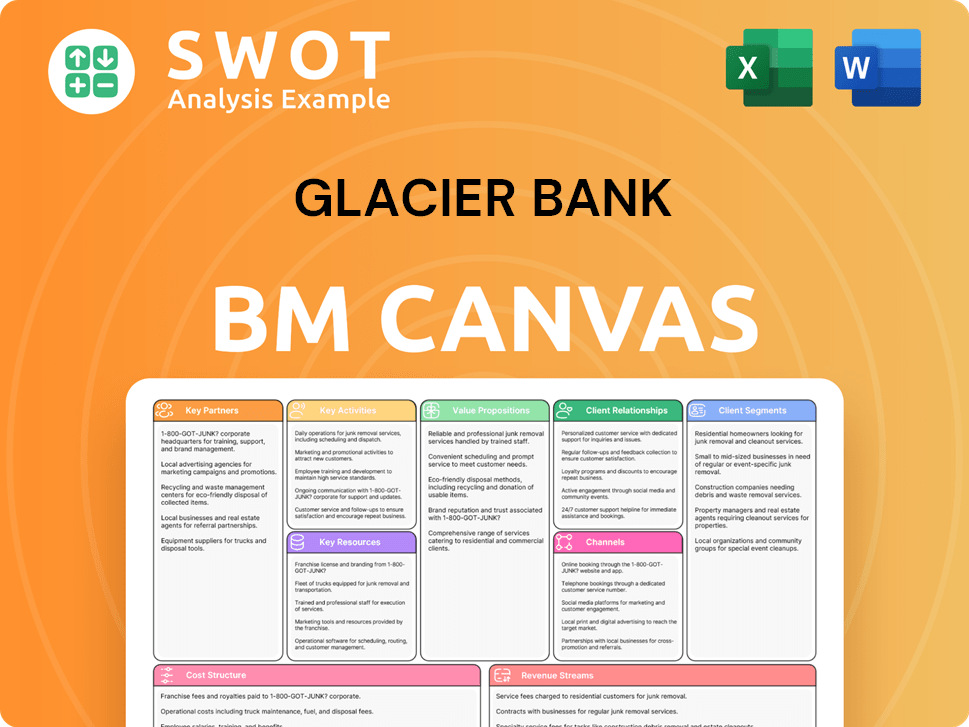

Glacier Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Glacier Bank?

The story of Glacier Bank, a prominent player among Montana banks, began in 1955 as First Federal Savings and Loan in Kalispell. Over the years, it has grown significantly through strategic acquisitions and adaptations. The company's journey includes a transition to public ownership, expansion beyond Montana, and a focus on community banking. The timeline illustrates the key moments that shaped the bank into the institution it is today.

| Year | Key Event |

|---|---|

| 1955 | Founded as First Federal Savings and Loan in Kalispell, Montana. |

| 1984 | Became a publicly held company as First Federal Savings Bank of Montana. |

| 1989 | Acquired Glacier National Bank, broadening its reach. |

| 1990 | Glacier Bancorp Inc. was established as the parent company. |

| 1992 | First Federal was renamed Glacier Bank. |

| 1999 | Ventured outside Montana with the acquisition of Mountain West Bank of Idaho. |

| 2012 | Consolidated its eleven commercial banks into a single, larger bank. |

| 2014 | Partnered with EVERFI to launch financial literacy programs. |

| 2023 | Reported total assets of $28.5 billion as of December 31. |

| 2024 (February 1) | Completed acquisition of Community Financial Group, Inc. (Wheatland Bank). |

| 2024 (July 19) | Completed acquisition of six Montana branch locations from HTLF Bank. |

| 2025 (January 13) | Announced acquisition of Bank of Idaho Holding Co. for $245.4 million. |

| 2025 (April 24) | Reported Q1 2025 net income of $54.6 million and diluted EPS of $0.48. |

| 2025 (April 30) | Completed the acquisition of Bank of Idaho Holding Co., integrating its operations into three existing Glacier Bank divisions. |

Glacier Bancorp is focused on expanding its presence through strategic acquisitions. The recent purchase of Bank of Idaho Holding Co. is a prime example, aiming to strengthen its footprint in key growth states like Idaho and Washington. These moves are central to its growth strategy within the banking industry.

The company is projecting further margin expansion in 2025, driven by asset repricing and securities portfolio runoff. In Q1 2025, the bank reported a net income of $54.6 million and diluted EPS of $0.48, showcasing its solid financial health. Decreasing deposit costs and increasing loan yields are expected to enhance profitability.

Analysts maintain a consensus 'Hold' rating for GBCI stock, with a target price of $51.50, despite a 22% year-to-date share price decline as of April 2025. Glacier Bancorp’s commitment to its 'super community banking' model and its strategic expansion efforts position it well in the evolving banking landscape.

Randy Chesler, President and CEO, expresses optimism about the company's ability to adapt and grow. The focus on operational efficiencies and a commitment to serving communities remain central to Glacier Bank's mission. This approach supports its long-term success and stability among Montana banks.

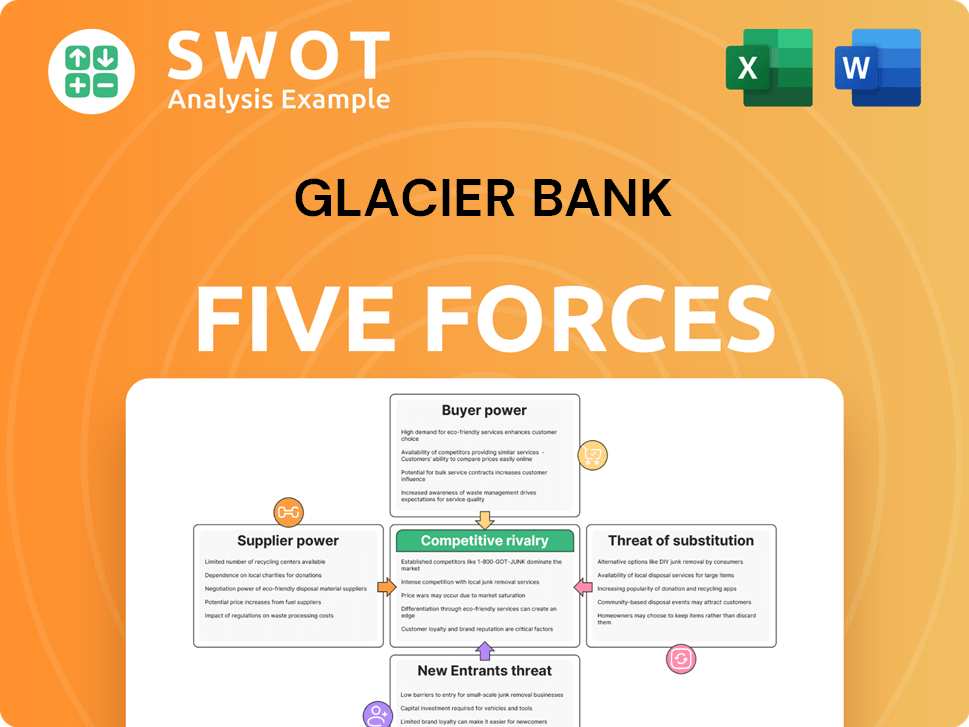

Glacier Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Glacier Bank Company?

- What is Growth Strategy and Future Prospects of Glacier Bank Company?

- How Does Glacier Bank Company Work?

- What is Sales and Marketing Strategy of Glacier Bank Company?

- What is Brief History of Glacier Bank Company?

- Who Owns Glacier Bank Company?

- What is Customer Demographics and Target Market of Glacier Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.