First Community Bank Bundle

Unveiling the Past: What's the Story Behind First Community Bank?

Explore the First Community Bank SWOT Analysis and uncover a fascinating journey through the annals of American finance. From its earliest beginnings, First Community Bank's story reflects the evolution of banking, community development, and the enduring power of local financial institutions. Discover how these banks have adapted and thrived, shaping the financial landscape for over a century.

The brief history of First Community Bank company reveals a tapestry of resilience and adaptation. Examining the FCB history, from its bank company origins to its key milestones, provides insights into the challenges and triumphs of community banking. Learn about the significant events that shaped these institutions and their lasting impact on the communities they serve, offering a valuable perspective on financial institution evolution.

What is the First Community Bank Founding Story?

The FCB history is marked by diverse origins, reflecting the decentralized nature of community banking. Several institutions operate under this name, each with a unique founding story and trajectory. These banks share a common goal: to serve their local communities and support their financial needs.

The story of First Community Bank is not a singular narrative but a collection of beginnings, each shaped by local needs and entrepreneurial visions. From the early 20th century to the late 20th century, these banks have evolved, adapting to changing economic landscapes and community demands. The bank company origins are rooted in a commitment to providing financial services.

Understanding the financial institution evolution of these banks offers insights into the broader trends in American banking. The early banking history of these institutions reveals the values and strategies that have guided their growth. The FCB history is a testament to the enduring role of community banks in fostering economic development and providing personalized financial services.

Founding Story

The Farmers State Bank of Beecher, Illinois, chartered on November 20, 1916, is one example of First Community Bank's origins. It started with fourteen businessmen and 26 shareholders, who invested $25,000. The bank's initial focus was on providing essential financial services to the local farming community.

- Fred Wehrmann was the first president.

- The bank acquired loans from The First National Bank of Beecher.

- By December 6, 1916, they had purchased 82 loans totaling $24,972.50.

Emmet County State Bank

Another First Community Bank, located in Harbor Springs, Michigan, began as Emmet County State Bank on November 1, 1905. William J. Clarke, an Irish immigrant, founded the bank. Clarke's vision was to establish a local bank to serve the financial needs of the lumber town and surrounding Emmet County.

- The bank became a member of the Federal Deposit Insurance Corporation in 1933.

- It joined the Federal Reserve System in 1937.

First Community Bank in South Carolina

In 1995, Jim Leventis and Mike Crapps founded First Community Bank in South Carolina. They believed local business owners needed a responsive financial partner. Their original offices were in Lexington and Forest Acres, South Carolina. Their business model centered on building strong relationships and providing essential services to local businesses. You can learn more about their core values in this article: Mission, Vision & Core Values of First Community Bank.

- The bank has grown to over 20 locations.

- It currently employs more than 250 people.

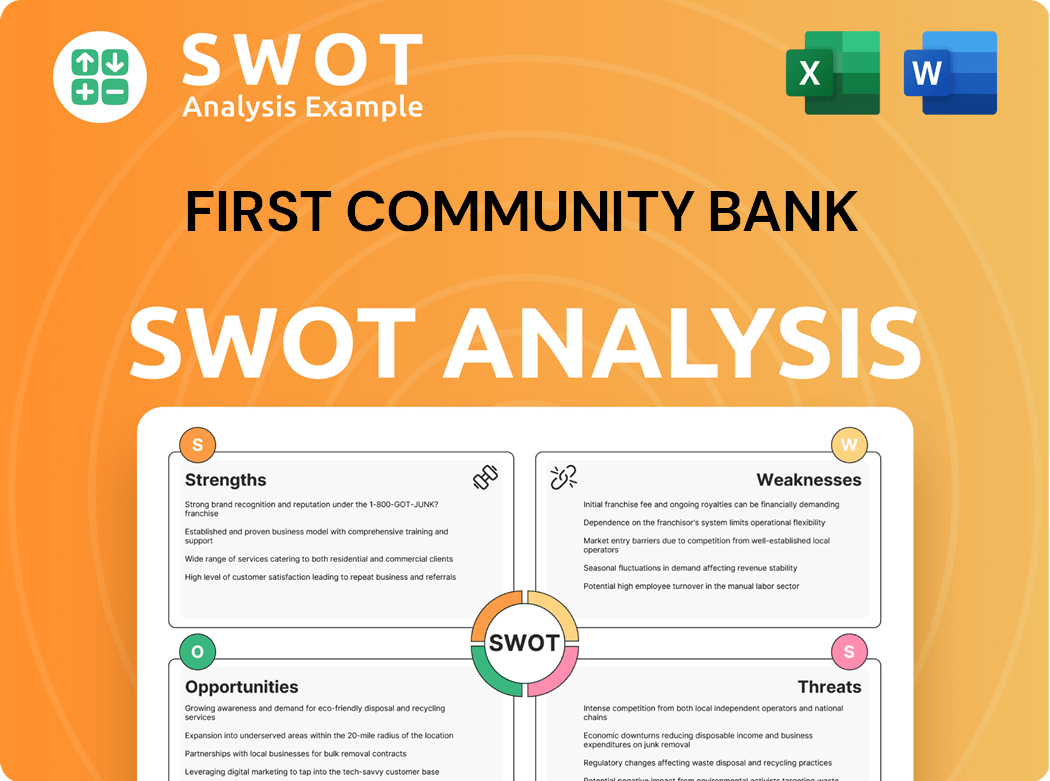

First Community Bank SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of First Community Bank?

The early growth and expansion of various First Community Bank entities showcase their dedication to meeting the evolving needs of their communities. This expansion is marked by strategic investments, asset growth, and geographical diversification. These banks have consistently broadened their services and market presence through mergers, acquisitions, and the opening of new branches.

Farmers State Bank of Beecher, Illinois, later known as First Community Bank, saw significant early growth. By the end of 1919, total assets reached $554,466, demonstrating a solid financial foundation. In 1945, the bank's assets exceeded $1,000,000, and by July 1946, it had made its 25,000th loan, highlighting its increasing community impact. This First Community Bank's history also included leadership transitions and the introduction of new financial products.

The evolution of First Community Bank in Harbor Springs, Michigan, from Emmet County State Bank to its current name in 1993, marked an expansion beyond Harbor Springs into Petoskey. This bank consistently expanded its geographical footprint, establishing branches in Cheboygan in 2000, Traverse City in 2006, Grand Rapids in 2012, and Birmingham in 2020. This expansion strategy demonstrates a commitment to serving a wider customer base within Michigan.

Founded in 1995, the South Carolina-based First Community Bank rapidly expanded its footprint through strategic mergers and acquisitions. Key milestones included merging with Bank of Camden in 2006 and Cornerstone National Bank in Upstate South Carolina in 2017. The bank expanded into Aiken and Augusta, Georgia, through a merger with Savannah River Banking Company in 2014. The bank's growth strategy led to the opening of its 20th location in 2018.

By 1984, the bank in Beecher, Illinois, had surpassed $25,000,000 in total assets, showcasing its financial growth. The South Carolina bank's expansion included further growth in downtown Greenville, S.C., and Evans, Ga., in 2019. These expansions highlight a focus on increasing market presence while maintaining a community-centric approach. The bank continues to adapt and grow to serve its customers better.

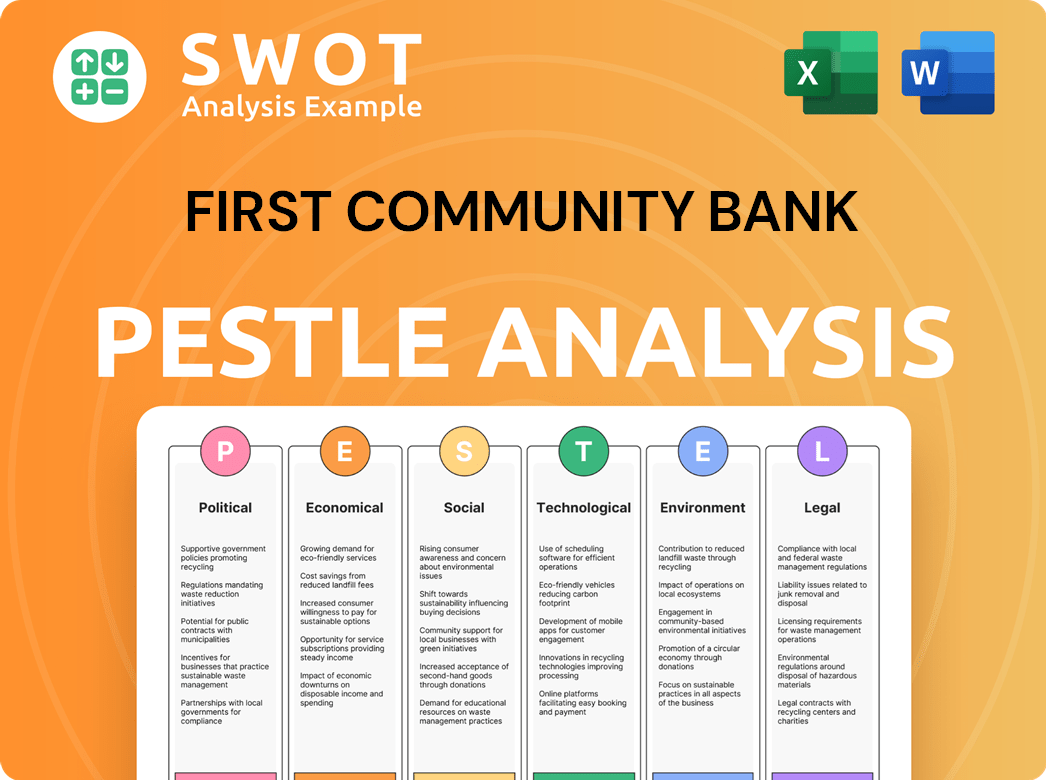

First Community Bank PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in First Community Bank history?

The FCB history is marked by several key milestones, reflecting its growth and adaptation within the financial landscape. From its origins as Farmers State Bank of Beecher, Illinois, to its expansion through acquisitions and technological advancements, the institution has continuously evolved to meet the needs of its customers and the challenges of the banking industry. The community bank timeline demonstrates a commitment to innovation and community service.

| Year | Milestone |

|---|---|

| August 7, 1942 | Farmers State Bank of Beecher applied for deposit insurance under the Federal Deposit Insurance Corporation (FDIC), ensuring greater security for depositors. |

| February 1975 | Bruce W. Bockelmann joined as cashier. |

| May 20, 1976 | The bank relocated to a new facility at 660 Penfield Street, introducing drive-up service. |

| Early 1990s | Introduction of Visa Debit Cards, a first for the area, allowing global card usage. |

| 1996 | The bank's name was changed to First Community Bank and Trust to reflect its multi-community presence, and it surpassed $50,000,000 in total assets. |

| 1997 | Full-featured electronic account access began with the introduction of TeleBanc. |

| June 2012 | Reopened Whiteville, North Carolina-based Waccamaw Bank as First Community Bank. |

| 2014 | Acquired Bank of America branches with $440 million in deposits in Virginia and North Carolina. |

| 2019 | Acquired Highlands Union Bank, rebranding all fifteen locations as First Community Bank, adding approximately $612 million in assets. |

| April 2023 | Completed a $113.2 million deal to acquire Surrey Bancorp, increasing its North Carolina locations to 11 and its total assets by $482 million. |

The bank has consistently embraced innovation to enhance customer experience and operational efficiency. A key innovation was the introduction of Visa Debit Cards in the early 1990s, a pioneering move that allowed customers to use their cards globally. Another example of innovation is the migration to a new online and mobile banking system in May 2024, which included features like mobile check deposit and bill pay.

Early Adoption of Technology

The introduction of Visa Debit Cards in the early 1990s marked an early adoption of technology, providing customers with greater convenience and global access to their funds. This initiative set the stage for future technological advancements.

Expansion of Services

The launch of TeleBanc in 1997 provided customers with full-featured electronic account access, enabling them to manage their finances remotely. This service expanded the bank's reach and convenience.

Mobile Banking Platform

The migration to a new online and mobile banking system in May 2024, featuring mobile check deposit and bill pay, demonstrates a commitment to providing modern, user-friendly banking solutions. This platform enhances accessibility.

Strategic Acquisitions

Acquiring other banks, such as Bank of America branches and Highlands Union Bank, allowed for an expansion of services and customer base. Strategic acquisitions have been key to the company's growth.

Branch Network Expansion

The addition of Surrey Bancorp in April 2023 increased the number of locations in North Carolina to 11, providing more convenient access for customers. Expansion of the branch network has been a focus.

Customer Service Enhancements

Focusing on customer service enhancements, such as the introduction of mobile check deposit and bill pay, shows the company is always looking for ways to improve customer satisfaction. The bank is dedicated to improving customer experience.

The banking industry faces several challenges, including intense competition, evolving customer expectations, and the rapid pace of technological change. These factors have driven First Community Bank to continually adapt its offerings and strategies. For more details on the bank's approach, you can explore the Marketing Strategy of First Community Bank.

Competitive Pressures

Stiff competition from larger financial institutions and other community banks requires continuous innovation and differentiation. The bank must maintain a competitive edge in the market.

Changing Customer Expectations

Customers now expect seamless digital experiences, which necessitates ongoing investment in technology and user-friendly platforms. Meeting these expectations is crucial.

Technological Advancements

The rapid pace of technological change requires continuous upgrades and adaptation to stay relevant and secure. The bank must keep up with the latest technology.

Regulatory Changes

Compliance with evolving government policies and regulations adds complexity and requires significant resources. Navigating these changes is essential.

Economic Fluctuations

Economic downturns and fluctuations can impact loan portfolios and overall financial performance. The bank must be prepared for economic changes.

Cybersecurity Threats

The increasing sophistication of cyber threats requires robust security measures to protect customer data and maintain trust. Cybersecurity is a major concern.

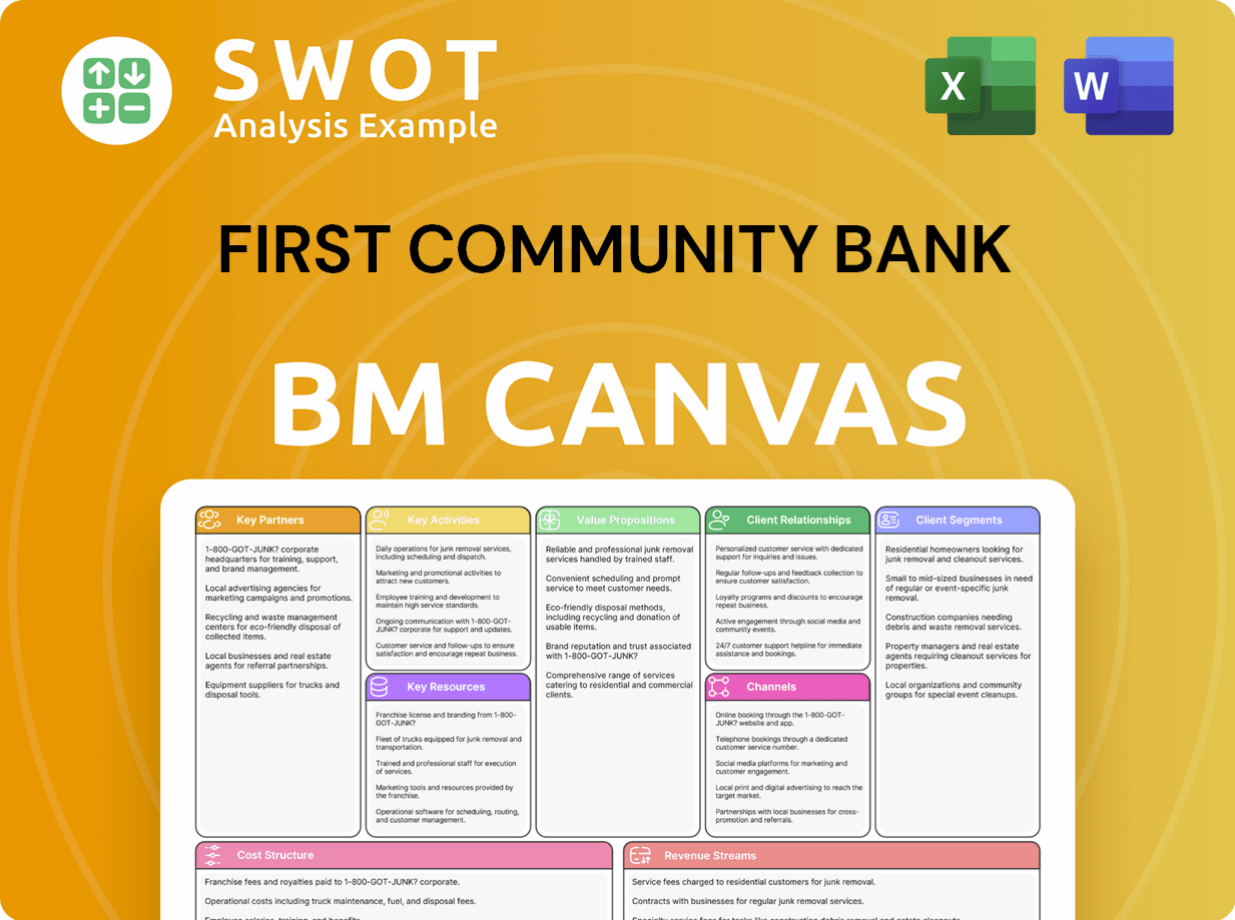

First Community Bank Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for First Community Bank?

The brief history of First Community Bank (FCB) showcases a journey of growth and adaptation. From its roots in the late 19th and early 20th centuries, FCB has expanded through strategic mergers and acquisitions, evolving to meet the changing needs of its customers and communities. Key milestones highlight its commitment to innovation and financial stability, positioning it for continued success in the financial landscape.

| Year | Key Event |

|---|---|

| 1874 | Roots of First Community Bankshares, Inc. established in Bluefield, Virginia. |

| 1905 | Emmet County State Bank, later to become a First Community Bank, opens in Harbor Springs, Michigan. |

| 1916 | Farmers State Bank of Beecher, Illinois, another precursor to a First Community Bank, opens for business. |

| 1933 | Emmet County State Bank becomes a member of the FDIC. |

| 1945 | Farmers State Bank of Beecher surpasses $1,000,000 in total assets. |

| 1976 | Farmers State Bank of Beecher moves to a new facility, introducing drive-up service. |

| 1989 | Farmers Bank changes its name to First Community Bank. |

| 1993 | Emmet County State Bank rebrands as First Community Bank due to expansion. First Community Bank of East Tennessee is founded. |

| 1995 | First Community Bank in South Carolina is founded by Jim Leventis and Mike Crapps. |

| 1996 | First Community Bank and Trust in Beecher, Illinois, surpasses $50,000,000 in total assets. |

| 1997 | First Community Bank introduces TeleBanc for electronic account access. |

| 2012 | First Community Bank (Bluefield, VA) reopens Waccamaw Bank branches. |

| 2014 | First Community Bank (Bluefield, VA) acquires Bank of America branches. First Community Bank (South Carolina) expands into Aiken and Augusta, GA. |

| 2019 | First Community Bank (Bluefield, VA) acquires Highlands Union Bank. |

| 2020 | First Community Bank (Harbor Springs, MI) opens a branch in Birmingham. |

| 2023 | First Community Bank (Bluefield, VA) completes acquisition of Surrey Bancorp, increasing assets by $482 million. |

| 2024 | First Community Bankshares, Inc. reports net income of $51.60 million and consolidated assets of $3.26 billion as of December 31. First Community Corporation (SC) reports net income of $14.0 million for 2024. |

| 2025 | First Community Bankshares, Inc. reports consolidated assets of $3.23 billion as of March 31, 2025. First Community Corporation (SC) reports total deposits increased to $1.726 billion at March 31, 2025, an annualized growth rate of 12.1%. |

Community banks are increasingly focused on digital banking and mobile applications. Partnerships with fintech companies are expanding the range of services offered. This focus on technology enhances customer experience and operational efficiency.

Emphasis is placed on financial literacy programs to empower customers. These programs help individuals and businesses make informed financial decisions. This commitment builds stronger customer relationships and community trust.

Strategic mergers and acquisitions, like the announced merger of First Community Bank of East Tennessee with TruPoint Bank in April 2025, are aimed at strengthening market position. These moves support sustainable growth and broader service offerings.

FCB companies remain committed to supporting local economies. This commitment includes supporting small businesses, as highlighted during National Small Business Week in May 2025. The focus on community service is a core value.

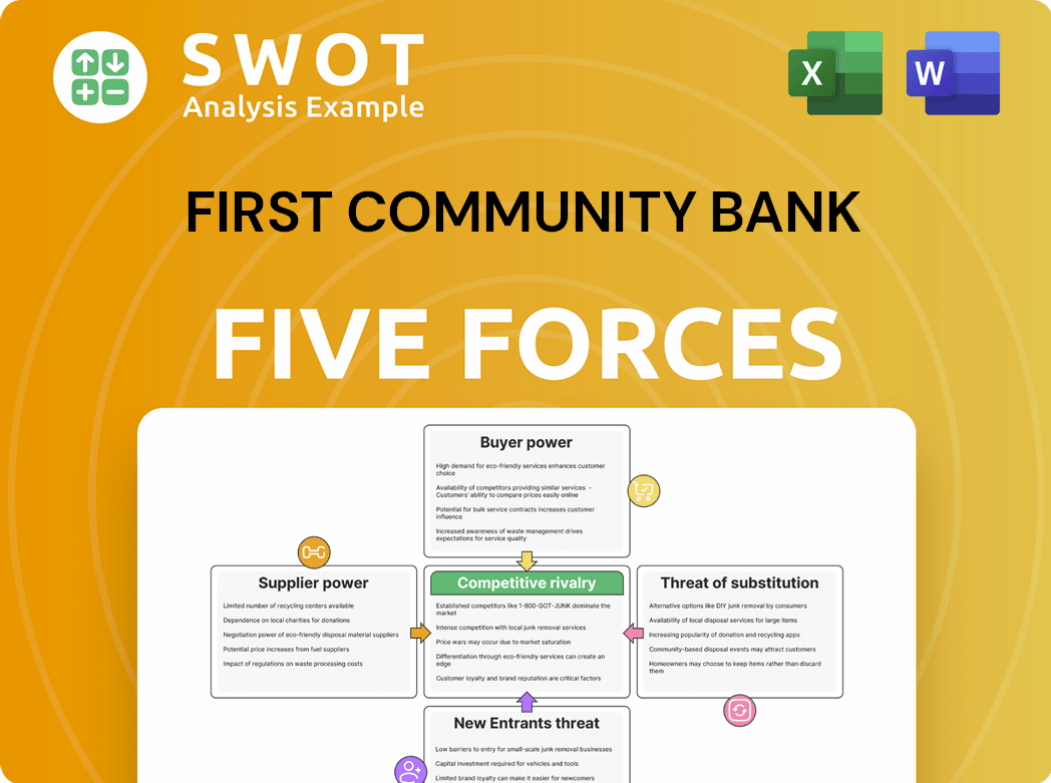

First Community Bank Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of First Community Bank Company?

- What is Growth Strategy and Future Prospects of First Community Bank Company?

- How Does First Community Bank Company Work?

- What is Sales and Marketing Strategy of First Community Bank Company?

- What is Brief History of First Community Bank Company?

- Who Owns First Community Bank Company?

- What is Customer Demographics and Target Market of First Community Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.