First Business Bundle

How Did First Business Company Emerge?

Embark on a journey through time to uncover the First Business SWOT Analysis, a financial institution with a rich early business history. From its humble beginnings, this oldest company has evolved, leaving an indelible mark on the financial landscape. Discover the pivotal moments that shaped its destiny and the visionary leadership that propelled it forward.

Delving into the company origins reveals a fascinating narrative of resilience and adaptation. Understanding the business establishment of First Business Financial Services, Inc. provides invaluable insights into its enduring success. Explore the historical business context that influenced its strategic decisions and market positioning.

What is the First Business Founding Story?

The story of the first business company, specifically First Business Financial Services, Inc., began in 1990. This marked a significant shift from its origins as Kingston State Bank, which was established much earlier in 1909. The transformation was driven by Jerry Smith, who saw an opportunity to create a bank focused on the unique needs of business owners.

Smith's vision was to establish a business-centric bank, a departure from traditional banking models. This involved hiring bankers and entrepreneurs who understood the intricacies of their clients' businesses. This approach set the stage for what would become a specialized financial institution.

The early business history of First Business centered on identifying a gap in the market. The initial business model was designed to provide high-quality commercial banking services. These included commercial loans, commercial real estate loans, equipment loans and leases, and treasury management services. These services were tailored for business owners, executives, professionals, and high-net-worth individuals.

Key Aspects of First Business's Founding

The founding of First Business was marked by a strategic shift from its roots as Kingston State Bank.

- Jerry Smith's leadership was critical in reshaping the bank to focus on business clients.

- The business model prioritized specialized services like commercial loans and treasury management.

- The early 1990s provided a favorable economic context for specialized financial services.

- The focus on deep client relationships and specialized expertise was fundamental to its establishment.

The bank's focus on building strong client relationships and providing specialized expertise was crucial. The economic climate of the early 1990s, with growing demand for specialized financial services, likely influenced the company's targeted approach. This allowed First Business to establish a distinct niche in the financial sector. For more details on its current operations, you can explore the Revenue Streams & Business Model of First Business.

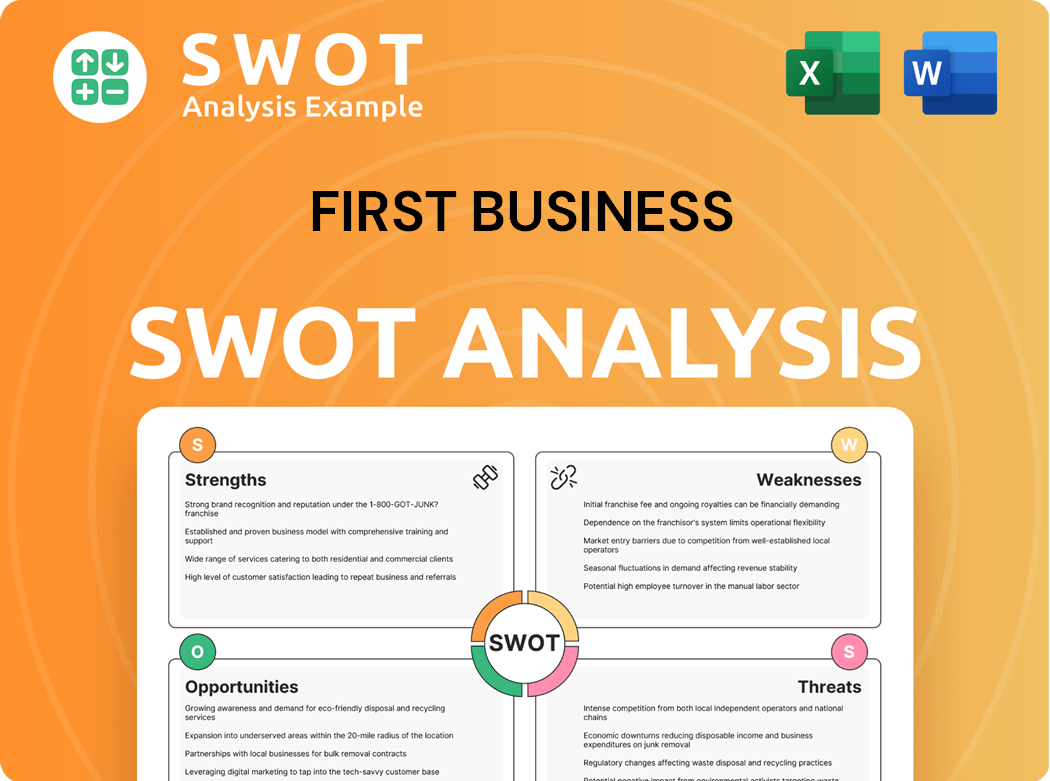

First Business SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of First Business?

The early growth and expansion of the first business company, following its refocus in 1990, centered on building strong client relationships and broadening its service offerings. Initially serving Madison, Wisconsin, with basic commercial banking, the company diversified as client needs evolved. This strategic move proved successful, leading to significant growth in assets under management. The company's expansion also included specialized financing options and geographic growth beyond its initial location.

In 2000, the company introduced 401(k) plans, followed by investment management services in 2001. This diversification into private wealth management was a key strategy. By expanding its services, the company aimed to meet the evolving needs of its clients and attract new business. This approach helped to establish a strong foundation for future growth.

The company progressively implemented offerings such as asset-based lending, accounts receivable financing, equipment finance, floorplan financing, and Small Business Administration (SBA) lending. These specialized financial products catered to a wider range of business needs. This expansion of services was a key factor in attracting and retaining clients.

Geographically, the company expanded beyond Madison, chartering First Business Bank-Milwaukee in 2000. In 2017, the company consolidated its subsidiary banks into a single bank operating subsidiary to streamline operations. This consolidation was aimed at improving efficiency while maintaining a local presence in key markets. The company's strategic approach included both organic growth and strategic consolidation.

As of March 31, 2025, the company's total assets reached $3.9 billion. Loans grew by 9.4% and deposits by 17.7% year-over-year. The company's operating model targets a 10% annual growth in loans, deposits, and revenue. You can learn more about their values in Mission, Vision & Core Values of First Business.

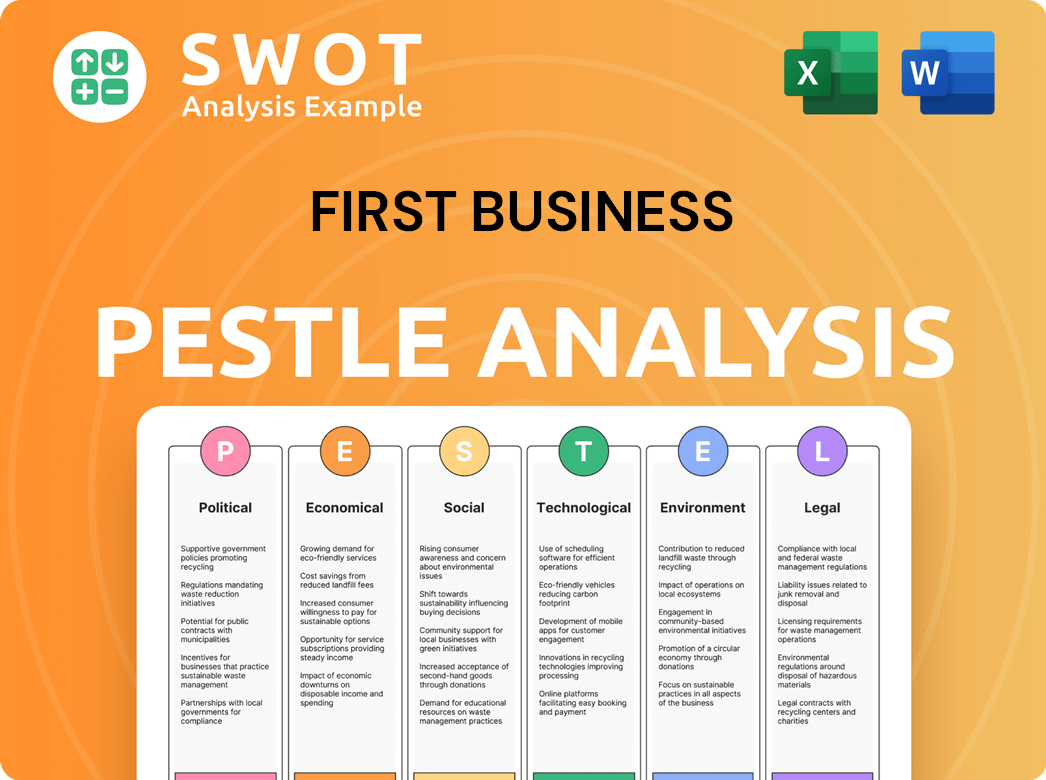

First Business PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in First Business history?

The Growth Strategy of First Business reflects a journey marked by significant milestones. The company's early business history is characterized by its focus on business-oriented banking, a strategy that has shaped its evolution and success.

| Year | Milestone |

|---|---|

| Founded (Over 35 years ago) | Jerry Smith pioneered the concept of a business-focused bank. |

| Q1 2025 | Private Wealth assets under management and administration reached a record $3.425 billion. |

| Early 2024 | Strategic plan finalized to foster innovative team members, grow core deposits, achieve operational excellence, and optimize business line performance. |

The company's innovations include its specialized approach to business banking, differentiating it from traditional banks. Furthermore, the implementation of robotic process automation (RPA) and automated financial statement spreading software showcases its commitment to technological advancements.

Business-Focused Banking Model

The company's foundational decision to operate as a business-focused bank, a concept pioneered by founder Jerry Smith, set it apart from traditional banks. This model catered specifically to the needs of business owners, leading to the development of comprehensive services.

Comprehensive Service Suite

The company developed a comprehensive suite of commercial banking, private wealth management, and bank consulting services. This diversification allowed the company to meet a wide range of financial needs for its clients.

Robotic Process Automation (RPA)

The implementation of robotic process automation (RPA) was a key innovation. This technology helped to streamline operations and improve efficiency across various departments.

Automated Financial Statement Spreading Software

The company utilized automated financial statement spreading software to improve credit analysis efficiency. This software helped to speed up the loan approval process and reduce errors.

Strategic Planning

The finalized strategic plan in early 2024 focused on fostering innovative team members, growing core deposits, achieving operational excellence, and optimizing business line performance. This plan helped to ensure sustainable profitability and growth.

Focus on Core Deposits

The company's core deposit growth strategy focused on attracting sticky deposits through deep business and private wealth relationships. This strategy helped to build a stable and reliable source of funding.

The company has faced challenges, including market downturns and competition from various financial institutions. They have also had to navigate regulatory changes and the variability of revenue streams from certain investments.

Market Downturns

The financial industry is subject to market downturns, which can impact profitability and growth. These downturns can lead to decreased demand for financial services and increased risk.

Competitive Threats

The company faces competition from a diverse range of institutions, including larger commercial banks, credit unions, and FinTech companies. This competition can put pressure on pricing and market share.

Regulatory Changes

Recent regulatory guidance has highlighted the importance of cybersecurity and operational risk management. The company must continuously monitor and adapt to these changes to ensure compliance.

Cybersecurity and Operational Risk

The company must manage cybersecurity and operational risks, which are crucial for maintaining customer trust and financial stability. Continuous monitoring and improvement are essential for mitigating these risks.

Revenue Stream Variability

The variability in swap fees and returns on SBIC funds has presented fluctuating revenue streams. This volatility can make financial planning and forecasting more challenging.

Core Deposit Growth

The company's core deposit growth strategy focuses on attracting sticky deposits through deep business and private wealth relationships. This strategy helps to build a stable and reliable source of funding.

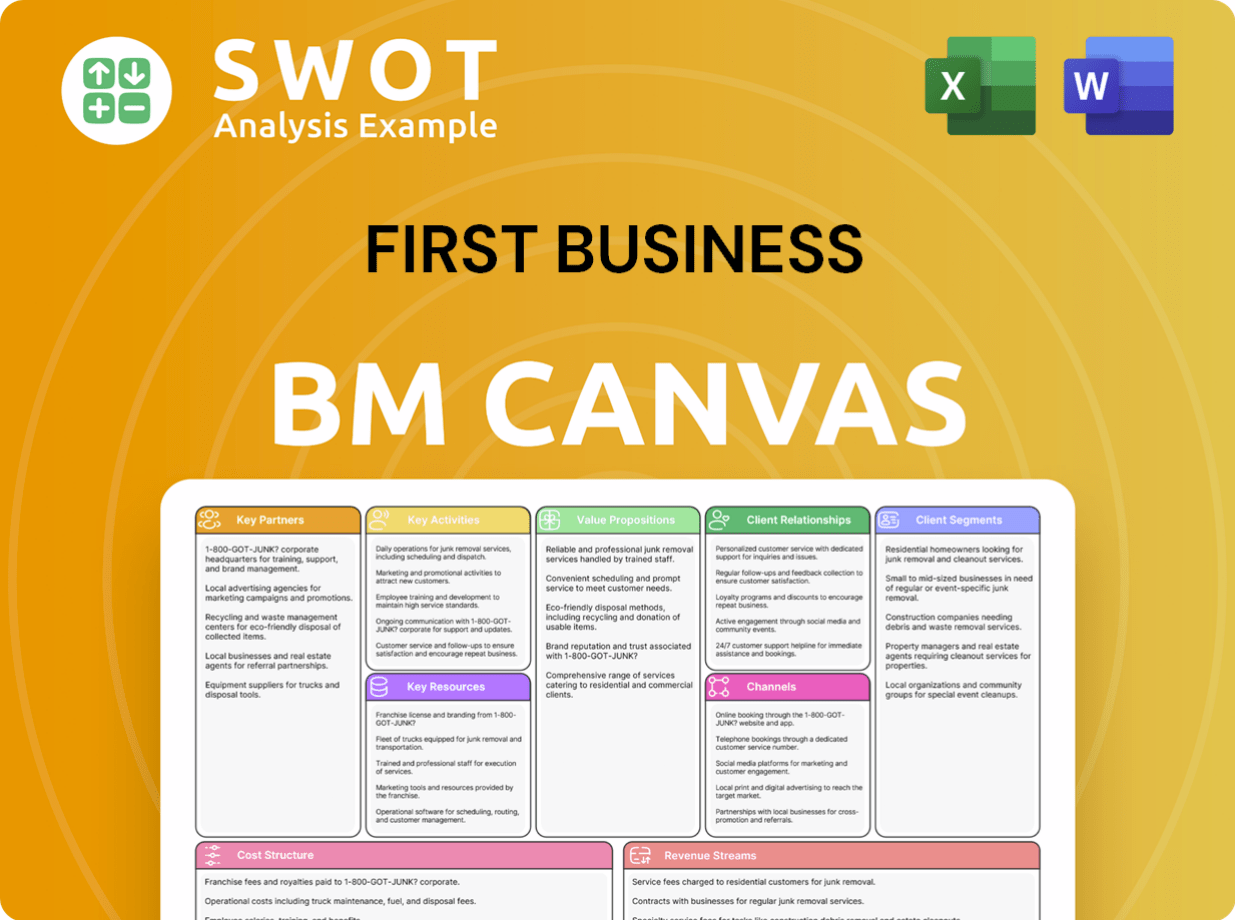

First Business Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for First Business?

The early business history of the first business company, now known as First Business Financial Services, Inc., showcases a journey of growth and adaptation. The company's company origins date back to 1909, evolving through name changes and strategic expansions to become a prominent financial institution. The following table outlines key milestones in its history.

| Year | Key Event |

|---|---|

| 1909 | Chartered as Kingston State Bank, marking the business establishment. |

| 1986 | Incorporated as a registered bank holding company under Wisconsin laws. |

| 1989 | Name changed to KD Bancshares, Inc. |

| 1990 | Relocated home office to Madison, Wisconsin, and refocused on small- to medium-sized businesses. |

| 1995 | First Business Capital Corp. was established, specializing in asset-based commercial lending. |

| 2000 | First Business Bank-Milwaukee was chartered and expanded into 401(k) plans. |

| 2001 | Began offering investment management services. |

| 2005 | Listed on Nasdaq under the symbol 'FBIZ.' |

| 2006 | Corey Chambas became Chief Executive Officer. |

| 2017 | Consolidated its subsidiary bank charters into a single bank operating subsidiary, First Business Bank. |

| Early 2024 | Finalized a new five-year strategic plan (2024-2028). |

| Q4 2024 | Reported total revenue growth of 6.6% for the full year, with net interest income growing by 10.3%. |

| March 31, 2025 | Total assets reached $3.9 billion, with loans up 9.4% and deposits up 17.7% year-over-year. |

| May 2, 2026 | Corey Chambas intends to retire as CEO, with David R. Seiler named as successor. |

First Business Financial Services is focused on its 2024-2028 strategic plan, aiming for continued organic growth. The company aims to achieve a 10% annual revenue growth, emphasizing engaged team members and operational excellence.

The company expects its net interest margin to remain between 3.60% and 3.65% in 2025. They anticipate an effective tax rate between 16% and 18% in 2025.

First Business plans to balance asset growth with potential share buyback programs to optimize long-term shareholder return. They aim to maintain CET1 above 9% at year-end 2024.

The financial services sector will continue to be shaped by digital transformation and AI integration. The company is leveraging technology to enhance customer experiences and operational efficiencies, staying true to its oldest company values.

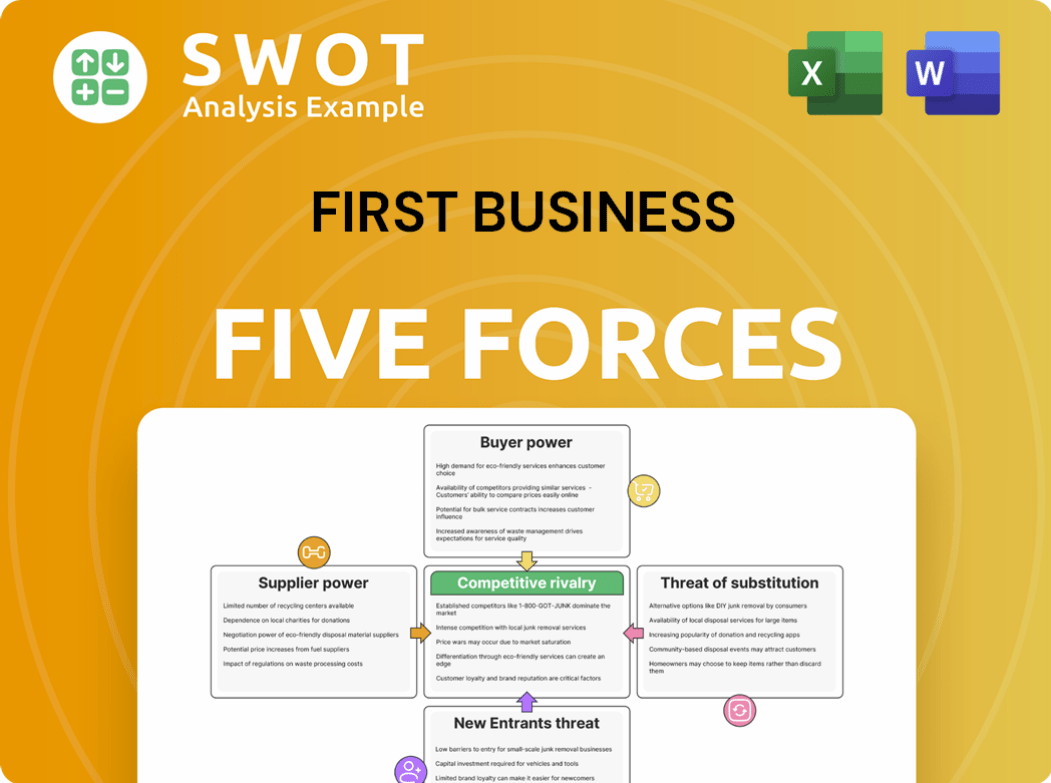

First Business Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of First Business Company?

- What is Growth Strategy and Future Prospects of First Business Company?

- How Does First Business Company Work?

- What is Sales and Marketing Strategy of First Business Company?

- What is Brief History of First Business Company?

- Who Owns First Business Company?

- What is Customer Demographics and Target Market of First Business Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.