Columbia Banking System Bundle

How did Columbia Bank Evolve from a One-Room Schoolhouse?

Journey back in time to discover the fascinating Columbia Bank SWOT Analysis, a financial institution that began in 1927 in Fair Lawn, New Jersey. From its roots in community banking, where loans were auctioned to local farmers, Columbia Bank has transformed into a significant player in the banking industry. Explore the remarkable

This

What is the Columbia Bank Founding Story?

The story of Columbia Bank, a prominent player in the banking industry, began in 1927. This financial institution took root as a building and loan association, setting the stage for its future growth. Understanding the brief history of Columbia Bank Washington provides valuable insight into its evolution.

The exact founding date and the names of all founders are not readily available in public records. However, its origins in a single room at the Bergen School House in Fair Lawn, New Jersey, highlight its community-focused beginnings. The initial goal was likely to provide accessible financial services for the local community, especially for farmers and business owners needing loans. This early focus shaped the bank's commitment to its customers.

In its early years, the bank used a unique business model: loans were auctioned off on the third Tuesday evening of each month. This approach offered a direct and transparent way for the community to access financing. This method catered to the specific needs of the community, providing a direct and transparent method for securing financing. This approach allowed the bank to build trust and support local economic activities.

Early Days and Community Focus

The bank's commitment to community banking is evident in anecdotes from its early days. While details about the company name selection or initial funding sources are not widely publicized, the context suggests a reliance on local deposits and community participation.

- The challenges during establishment included building trust, managing limited resources, and adapting to the economic climate of the late 1920s.

- The cultural and economic context of the time emphasized localized financial support and community development.

- The bank's early success was built on its ability to meet the financial needs of its local customers.

- Understanding Columbia Bank's marketing strategy can offer additional insights into its approach.

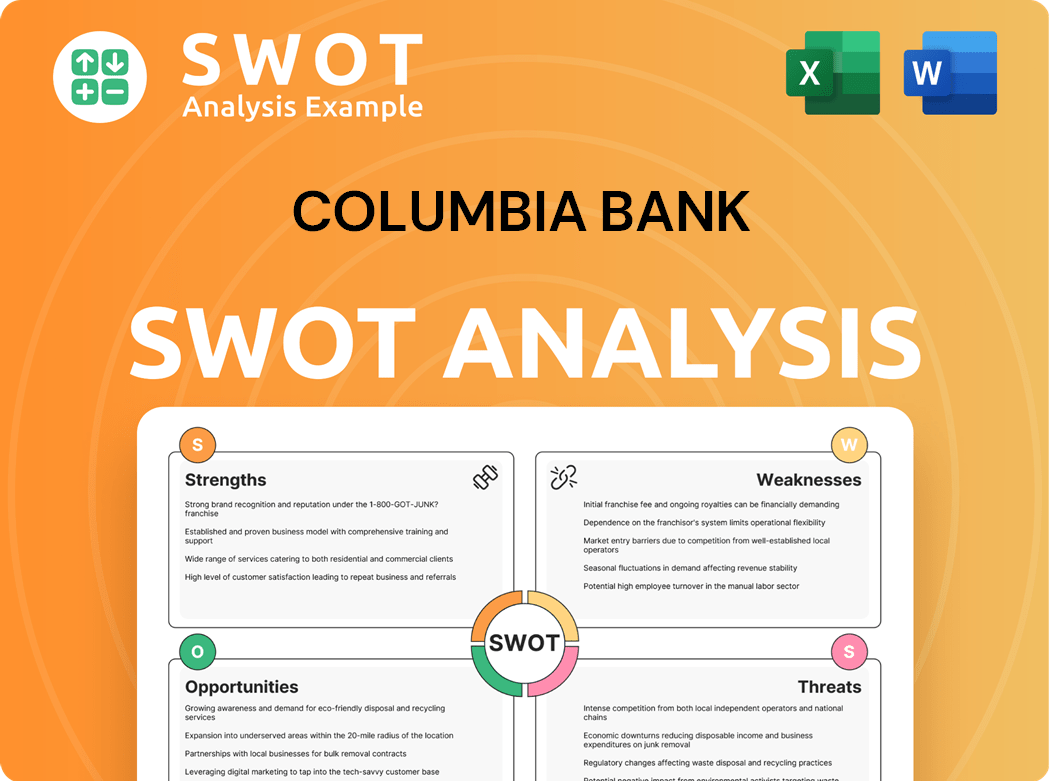

Columbia Banking System SWOT Analysis

- Complete SWOT Breakdown

- Fully Customizable

- Editable in Excel & Word

- Professional Formatting

- Investor-Ready Format

What Drove the Early Growth of Columbia Bank?

The early growth of Columbia Bank was marked by a steady expansion of its services and geographical reach, always maintaining its community banking focus. The bank pioneered innovations like drive-up and walk-up service windows, and school savings programs, demonstrating an early commitment to customer convenience. As customer numbers, deposits, and locations increased, Columbia Bank expanded its physical presence. By 2017, it served 10 New Jersey counties with a network of 46 full-service branches and three lending offices.

Columbia Banking System, Inc., the holding company, was established in 1993 to address a gap in local community banking caused by industry consolidation. The initial public offering (IPO) in 1993 fueled rapid growth in its initial years. This strategic move was crucial for the Revenue Streams & Business Model of Columbia Bank, enabling further expansion and investment in customer-focused services.

In the early 2000s, Columbia Bank expanded from the Puget Sound region into the Oregon coast, including the acquisition of Bank of Astoria. The bank further expanded its footprint through strategic acquisitions, partnering with the FDIC on five acquisitions of failed banks during the Great Recession. This growth continued throughout Washington, most of Oregon, Idaho, and northern California.

The acquisition of Freehold Bank in October 2024 further supported its regional presence and helped reduce expenses. This strategic growth, including its focus on relationship-driven lending and deposit growth strategies, has positively impacted its loan portfolio and deposit base, leading to more stable, recurring revenue streams. As of March 31, 2025, Columbia Bank (Columbia Financial, Inc.) had approximately $10.6 billion in assets, 69 full-service branch offices, and four regional lending centers.

In the first quarter of 2025, customer deposits increased notably by $440 million, highlighting the success of small business campaigns and the ability to win new relationships. This growth reflects the ongoing success of Columbia Bank's strategies and its ability to attract and retain customers within the competitive banking industry.

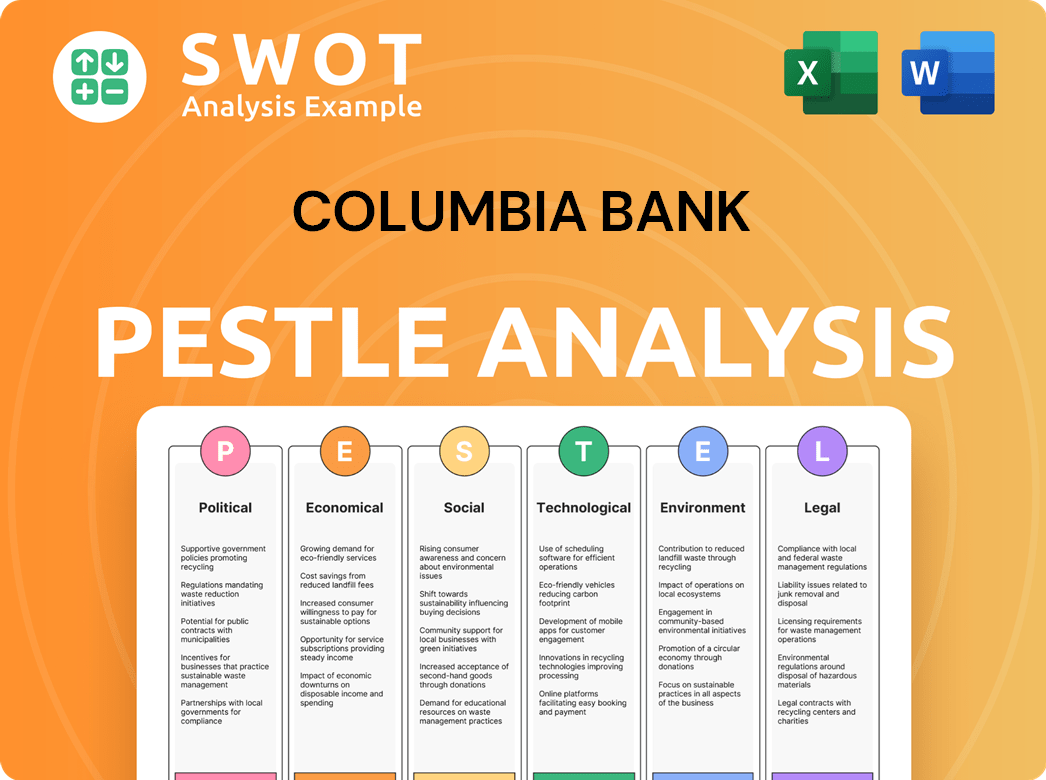

Columbia Banking System PESTLE Analysis

- Covers All 6 PESTLE Categories

- No Research Needed – Save Hours of Work

- Built by Experts, Trusted by Consultants

- Instant Download, Ready to Use

- 100% Editable, Fully Customizable

What are the key Milestones in Columbia Bank history?

The Columbia Bank history is marked by significant milestones, particularly its consistent focus on community banking since its establishment in 1927. This commitment has allowed it to build a strong presence in the banking industry, adapting to changing market dynamics while maintaining a customer-centric approach. The financial institution's journey reflects a blend of tradition and innovation, positioning it for continued growth and relevance.

| Year | Milestone |

|---|---|

| 1927 | Founded, marking the beginning of Columbia Bank's journey as a community bank. |

| Early Years | Introduced innovative services like drive-up windows and school savings programs, showcasing a forward-thinking approach. |

| 2024 | Reported operating earnings per share (EPS) of $0.72 in Q4, exceeding estimates, and achieved a net income of $143 million for the full year. |

| January 2025 | Maintained a 28-year streak of consecutive dividend payments, offering a 5.1% yield. |

| April 2025 | Announced the acquisition of Pacific Premier Bancorp, enhancing market leadership and expansion in Southern California. |

Columbia Bank has consistently embraced innovation to enhance customer service and operational efficiency. Early innovations included drive-up and walk-up service windows, and school savings programs, setting a precedent for customer-focused solutions.

Drive-Up and Walk-Up Service

Early adoption of drive-up and walk-up service windows provided convenient access to banking services. This approach demonstrated a commitment to customer convenience and efficiency from the start.

School Savings Programs

Initiatives like school savings programs promoted financial literacy and engagement with the community. These programs helped build long-term customer relationships.

24/7 Mobile and Online Banking

Investment in 24/7 mobile and online banking provides customers with continuous access to their accounts. This enhances convenience and accessibility.

Remote Deposits

Remote deposit capture allows customers to deposit checks electronically, saving time and improving efficiency. This service streamlines banking processes.

Intelligent ATMs

The use of 'Intelligent ATMs' offers advanced functionalities, enhancing the banking experience. These ATMs provide improved transaction capabilities.

Universal Banker Program

The 'Universal Banker' program utilizes specialists for consumer and business banking, enhancing customer service. This approach provides comprehensive support.

Despite its successes, Columbia Banking System faces several challenges, including intense competition and economic uncertainties. The bank overview reveals that it must navigate these challenges while continuing to innovate and adapt to maintain its market position.

Competition

Intense competition for deposits and loans from larger national banks and fintech disruptors poses a significant challenge. Maintaining a competitive edge requires strategic initiatives.

Declining Net Interest Income

Declining net interest income impacts profitability, requiring the bank to manage its assets and liabilities effectively. This includes optimizing interest rate spreads.

Legal and Restructuring Costs

Substantial legal settlements and restructuring expenses, such as a $55 million legal settlement and $14.4 million in merger and restructuring costs, affect financial performance. These costs require careful financial planning.

Economic and Regulatory Uncertainties

Economic and regulatory uncertainties add complexity to the business environment, necessitating proactive risk management. Adapting to regulatory changes is crucial.

Strategic Responses

The bank's strategic responses include optimizing its branch network and investing in digital banking capabilities. These moves aim to improve efficiency and customer service.

Acquisitions

Targeted acquisitions, such as the Pacific Premier Bancorp deal, are part of the expansion strategy. This enhances market leadership and accelerates growth.

For more insights into the ownership structure and shareholder details, you can explore Owners & Shareholders of Columbia Bank.

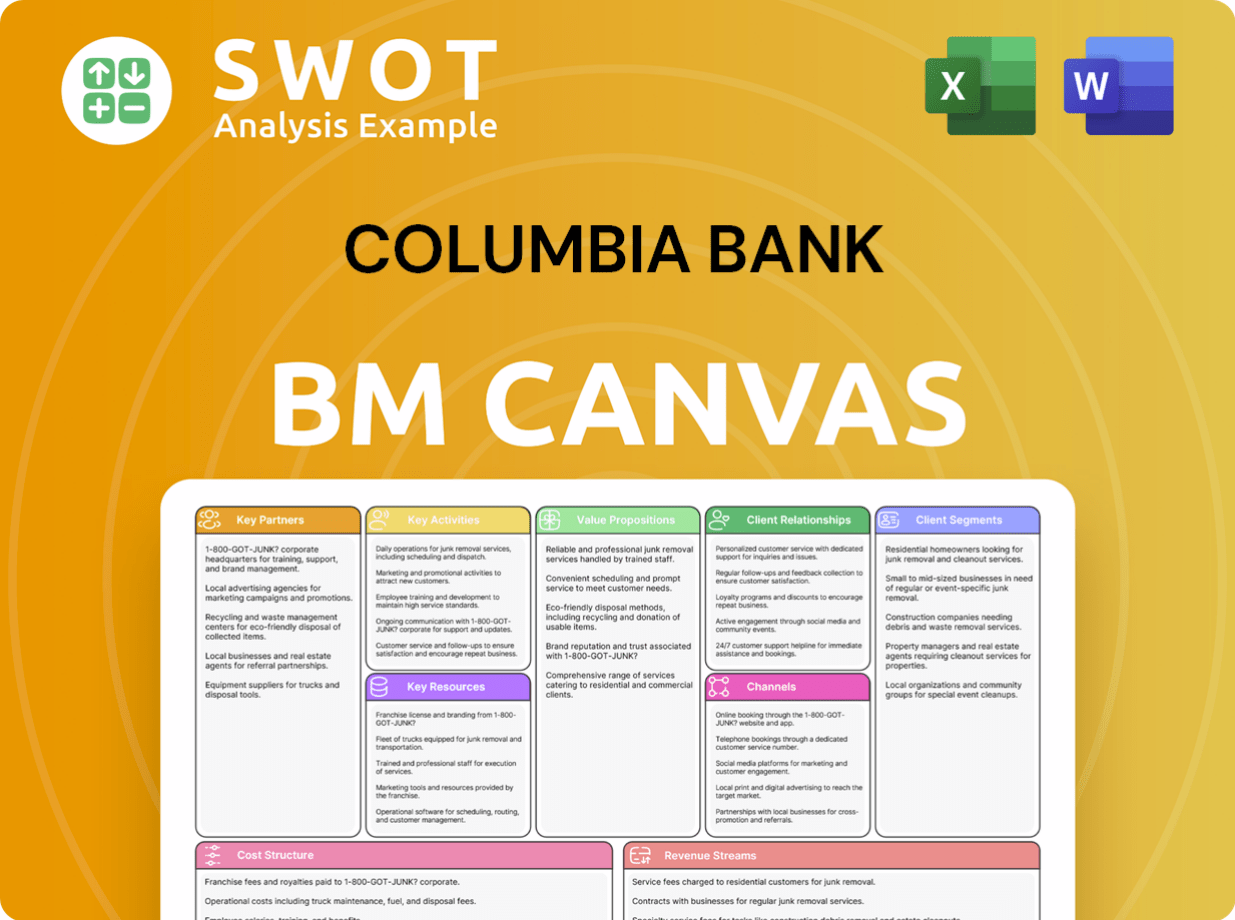

Columbia Banking System Business Model Canvas

- Complete 9-Block Business Model Canvas

- Effortlessly Communicate Your Business Strategy

- Investor-Ready BMC Format

- 100% Editable and Customizable

- Clear and Structured Layout

What is the Timeline of Key Events for Columbia Bank?

The Columbia Bank history is marked by strategic growth and adaptation within the banking industry, evolving from its roots in Fair Lawn, New Jersey, to a significant presence in the Pacific Northwest and beyond. Over the years, Columbia Banking System has navigated economic cycles, expanded through acquisitions, and strategically positioned itself for future success. The financial institution has consistently adapted to market changes, demonstrating a commitment to both organic growth and strategic acquisitions.

| Year | Key Event |

|---|---|

| 1927 | Columbia Bank is founded in Fair Lawn, New Jersey, starting as a building and loan association. |

| 1993 | Columbia Banking System is established to fill a void in the local community bank sector. |

| Early 2000s | Columbia expands into the Oregon coast, acquiring Bank of Astoria. |

| Great Recession | Columbia partners with the FDIC on five acquisitions of failed banks. |

| October 2021 | Columbia Bank is acquired by Umpqua Bank. |

| February 2023 | Columbia completes its merger with Umpqua Bank. |

| October 2024 | Columbia Financial, Inc. consolidates and integrates Freehold Bank. |

| Q4 2024 | Columbia Banking System reports full-year 2024 net income of $143 million and operating net income of $150 million, with a net interest margin of 3.64%. |

| Q1 2025 | Columbia Banking System reports operating earnings per share of $0.72 and Columbia Bank (Columbia Financial, Inc.) reports net income of $8.9 million. |

| March 2025 | Umpqua Bank expands into Colorado with its first retail branch and commercial office in Denver. |

| April 2025 | Columbia Banking System announces its definitive merger agreement to acquire Pacific Premier Bancorp in an all-stock transaction. |

Columbia Banking System anticipates continued growth, projecting low to mid-single-digit loan growth. The company is focused on optimizing its branch network and investing in digital banking capabilities. Management is also pursuing targeted acquisitions to expand its market presence.

The acquisition of Pacific Premier Bancorp is expected to close in the second half of 2025. The combined company is expected to have approximately $70 billion in assets. The strategic acquisition of Pacific Premier accelerates Columbia's expansion in Southern California.

The acquisition of Pacific Premier is expected to deliver mid-teens EPS accretion, with tangible book value dilution earned back in three years. Columbia projects EPS accretion of 14% in 2026 and 15% in 2027. The company expects operating expenses for 2025 to range between $1.0 billion and $1.01 billion.

Columbia plans to expand its branch network in 2025, using savings from 2024 branch consolidations. The combined organization will operate under the unified brand of Columbia Bank, with Umpqua Bank changing its name to Columbia Bank. The goal is to achieve a top-10 deposit market share position in Southern California.

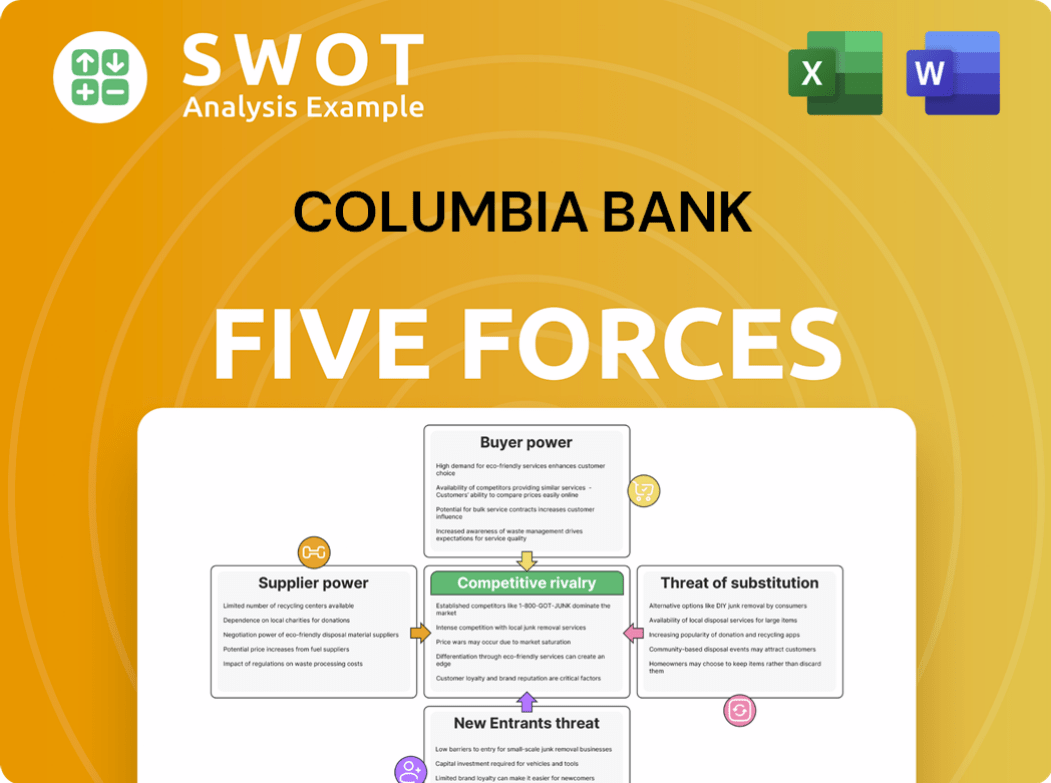

Columbia Banking System Porter's Five Forces Analysis

- Covers All 5 Competitive Forces in Detail

- Structured for Consultants, Students, and Founders

- 100% Editable in Microsoft Word & Excel

- Instant Digital Download – Use Immediately

- Compatible with Mac & PC – Fully Unlocked

Related Blogs

- What is Competitive Landscape of Columbia Bank Company?

- What is Growth Strategy and Future Prospects of Columbia Bank Company?

- How Does Columbia Bank Company Work?

- What is Sales and Marketing Strategy of Columbia Bank Company?

- What is Brief History of Columbia Bank Company?

- Who Owns Columbia Bank Company?

- What is Customer Demographics and Target Market of Columbia Bank Company?

Disclaimer

All information, articles, and product details provided on this website are for general informational and educational purposes only. We do not claim any ownership over, nor do we intend to infringe upon, any trademarks, copyrights, logos, brand names, or other intellectual property mentioned or depicted on this site. Such intellectual property remains the property of its respective owners, and any references here are made solely for identification or informational purposes, without implying any affiliation, endorsement, or partnership.

We make no representations or warranties, express or implied, regarding the accuracy, completeness, or suitability of any content or products presented. Nothing on this website should be construed as legal, tax, investment, financial, medical, or other professional advice. In addition, no part of this site—including articles or product references—constitutes a solicitation, recommendation, endorsement, advertisement, or offer to buy or sell any securities, franchises, or other financial instruments, particularly in jurisdictions where such activity would be unlawful.

All content is of a general nature and may not address the specific circumstances of any individual or entity. It is not a substitute for professional advice or services. Any actions you take based on the information provided here are strictly at your own risk. You accept full responsibility for any decisions or outcomes arising from your use of this website and agree to release us from any liability in connection with your use of, or reliance upon, the content or products found herein.